Transplant Diagnostics Market Size, Share & Trends Analysis Report By Technology (PCR, NGS, Sanger Sequencing), Product (Instrument, Reagent, Software), Application (HLA, Blood Profile, Pathogen Detection), Type (Heart, Kidney, Liver, Bone Marrow), End User, By Region, And Segment Forecasts, 2025-2034

Global Transplant Diagnostics Market Size is valued at USD 4.9 Bn in 2024 and is predicted to reach USD 10.4 Bn by the year 2034 at a 7.9% CAGR during the forecast period for 2025-2034.

The rise in organ transplants is a significant aspect driving demand for diagnostics utilized before surgery. There has always been a greater need for transplants than available organs. Nonetheless, the market will likely profit from in-depth field study and analysis to close this gap. The European Commission's initiatives for organ harvesting have made donated organs available.

The availability of the European donor card and rising public awareness have further increased the region's organ donation rate. Similar to other countries, the U.S. has seen significant organ donation increases due to increased awareness. Also, the demand for organ transplant surgeries is increasing due to the rising number of patients with chronic illnesses that frequently cause organ failure. Personalized medicine and stem cell therapy are also becoming more widely used. Pre-procedure diagnostics are in high demand as a result. Improved and sophisticated diagnostic methods are required due to the risks and complexity of organ transplantation.

Recent Developments:

- In March 2022, Immucor, Inc., a business specialising in transfusion and transplantation diagnostics, introduced two new products to its transplant diagnostics line, proving its dedication to recent developments in the histocompatibility industry.

Competitive Landscape:

Some of the primary Transplant Diagnostics Market players are:

- Abbott Laboratories, Inc.

- Adaptive Biotechnologies

- Affymetrix, Inc.

- altona Diagnostics GmbH

- Arquer Diagnostics Ltd

- BAG Diagnostics GmbH

- Becton, Dickinson and Company,

- Biofortuna Limited

- BioMerieux SA,

- Bio-rad Laboratories, Inc.

- Biotype GmbH

- Bruker,

- CareDx Inc.

- CLONIT srl

- Diagnóstica Longwood SL

- DiaSorin S.p.A.

- ELITechGroup

- EUROFINS VIRACOR

- Hoffmann La-Roche AG.

- Hologic, Inc.

- Horiba Ltd

- Illumina, Inc.

- Immucor Transplant Diagnostics, Inc.

- Laboratory Corporation of America Holdings.

- Linkage Biosciences

- Luminex Corporation

- Merck KGaA

- NanoString

- Olerup SSP AB

- Omixon Ltd.

- PathoNostics

- Preservation Solutions, Inc.

- Qiagen N.V.

- Randox Laboratories Ltd.

- Stryker

- Takara Bio Inc.

- Thermo Fisher Scientific,

- TransMedics

- Transonic

- Zimmer Biomet

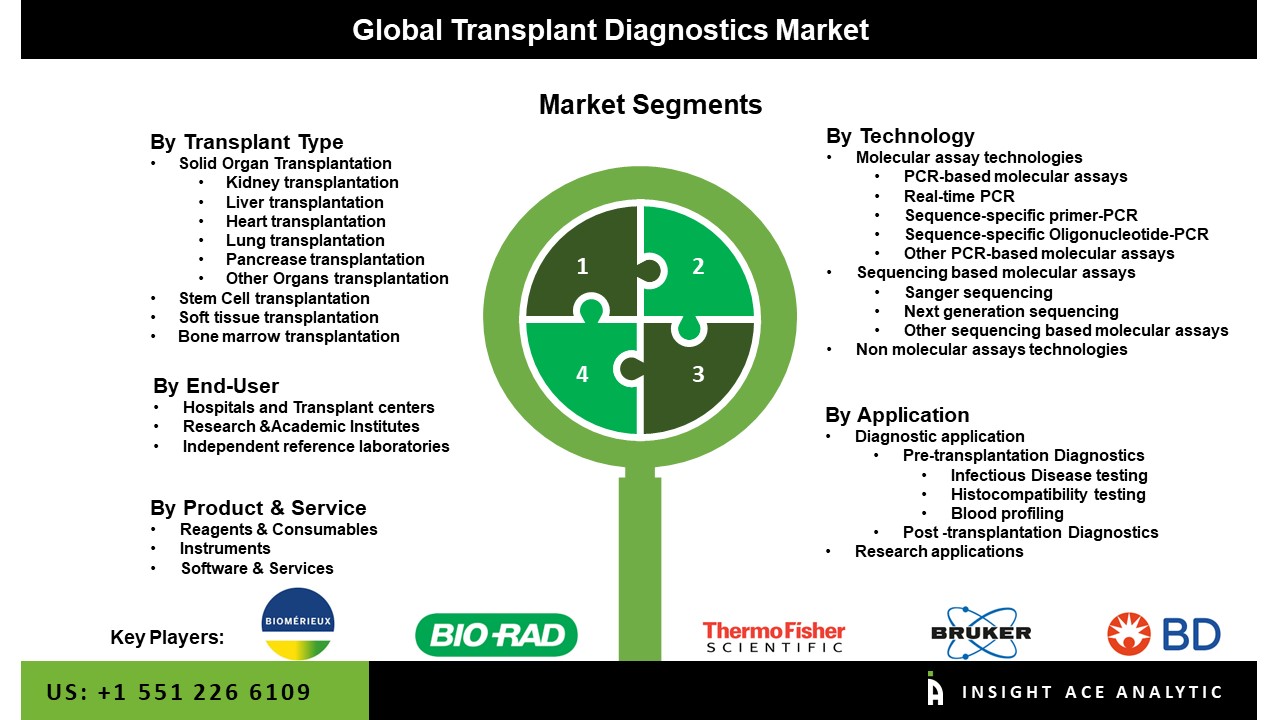

Market Segmentation:

The Transplant Diagnostics market is segmented on the basis of product & service, application, technology, transplant type, and end-user. Based on technology, the market is segmented into molecular assay technologies, sequencing-based molecular assays, and nonmolecular assay technologies. The product & service segment includes consumables, instruments, and software & services. By application, the market is segmented into diagnostic applications and research applications. By transplant type, the market is segmented as solid organ, stem cell, soft tissue, and bone marrow transplantation. End-use segment includes hospitals & Transplant services, research & academic institutes, and independent reference laboratories.

Based On Product & Services, The Software & Services Segment Is Accounted As A Major Contributor In The Transplant Diagnostics Market.

Reagents and consumables are anticipated to expand first, followed by the services and software category. The introduction of more complex instruments has raised the need for training sessions to instruct technical employees on handling and usage, which has contributed to the expansion of this market. Also, the industry growth is being fueled by elements like regular software upgrades and better services provided by market competitors to remain competitive.

Pre-Transplantation Diagnostics Segment Witnessed Growth At A Rapid Rate.

The producers of these diagnostic products are using tactics like purchasing agreements for reagents and consumables. Moreover, the frequent procurement of reagents and consumables is a crucial element in speeding adoption. As a result, the category had the highest revenue share in 2016 and is anticipated to continue to hold the top spot throughout the projected period.

In The Region, The North America Transplant Diagnostics Market Holds A Significant Revenue Share.

The majority of revenue came from North America. Key influences include the widespread use of cutting-edge methods and diagnostic technologies, rising healthcare costs, and the accessibility of qualified personnel. Due to factors including a highly established healthcare infrastructure and the availability of qualified specialists, the U.S. has the most significant market share. Also, the widespread use of stem cell therapies, tailored pharmaceuticals, and soft tissue transplants is promoting regional market expansion.

Transplant Diagnostics Market Report Scope:

| Report Attribute | Specifications |

| Market size value in 2024 | USD 4.9 Bn |

| Revenue forecast in 2034 | USD 10.4 Bn |

| Growth rate CAGR | CAGR of 7.9% from 2025 to 2034 |

| Quantitative units | Representation of revenue in US$ Bn, and CAGR from 2025 to 2034 |

| Historic Year | 2021 to 2024 |

| Forecast Year | 2025-2034 |

| Report coverage | The forecast of revenue, the position of the company, the competitive market statistics, growth prospects, and trends |

| Segments covered | Product & Service, Application, Technology, Transplant Type, And End-User. |

| Regional scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia; South Korea; Southeast Asia |

| Competitive Landscape | BioMerieux SA, Becton, Dickinson and Company, Thermo Fisher Scientific, Bio-Rad Laboratories, Bruker, and Merck KGaA. |

| Customization scope | Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

| Pricing and available payment methods | Explore pricing alternatives that are customized to your particular study requirements. |

Segmentation of Transplant Diagnostics Market-

Transplant Diagnostics Market By Technology-

- Molecular assay technologies

- PCR based molecular assays

- Real-time PCR

- Sequence-specific primer-PCR

- Sequence-specific Oligonucleotide-PCR

- Other PCR-based molecular assays

- Sequencing based molecular assays

- Sanger sequencing

- Next generation sequencing

- Others

- Non molecular assays technologies

Transplant Diagnostics Market By Product & Service-

- Reagents & Consumables

- Instruments

- Software & Services

Transplant Diagnostics Market By Application-

- Diagnostic application

- Pre-transplantation

- Infectious Disease testing

- Histocompatibility testing

- Blood profiling

- Post-transplantation diagnostics

- Pre-transplantation

- Research applications

Transplant Diagnostics Market By Transplant Type-

- Solid organ transplantation

- Kidney

- Liver

- Heart

- Lung

- Pancreases

- Others

- Stem Cell Transplantation

- Soft Tissue Transplantation

- Bone Marrow Transplantation

Transplant Diagnostics Market By End-User-

- Hospitals & Transplant Centers

- Research & Academic Institutes

- Independent Research Laboratories

Transplant Diagnostics Market By Region-

North America-

- The US

- Canada

Europe-

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

Asia-Pacific-

- China

- Japan

- India

- South Korea

- South East Asia

- Rest of Asia Pacific

Latin America-

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Middle East & Africa-

- GCC Countries

- South Africa

- Rest of Middle East and Africa

Research Design and Approach

This study employed a multi-step, mixed-method research approach that integrates:

- Secondary research

- Primary research

- Data triangulation

- Hybrid top-down and bottom-up modelling

- Forecasting and scenario analysis

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary Research

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Sources Consulted

Secondary data for the market study was gathered from multiple credible sources, including:

- Government databases, regulatory bodies, and public institutions

- International organizations (WHO, OECD, IMF, World Bank, etc.)

- Commercial and paid databases

- Industry associations, trade publications, and technical journals

- Company annual reports, investor presentations, press releases, and SEC filings

- Academic research papers, patents, and scientific literature

- Previous market research publications and syndicated reports

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

Primary Research

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Stakeholders Interviewed

Primary interviews for this study involved:

- Manufacturers and suppliers in the market value chain

- Distributors, channel partners, and integrators

- End-users / customers (e.g., hospitals, labs, enterprises, consumers, etc., depending on the market)

- Industry experts, technology specialists, consultants, and regulatory professionals

- Senior executives (CEOs, CTOs, VPs, Directors) and product managers

Interview Process

Interviews were conducted via:

- Structured and semi-structured questionnaires

- Telephonic and video interactions

- Email correspondences

- Expert consultation sessions

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

Data Processing, Normalization, and Validation

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

- Standardization of units (currency conversions, volume units, inflation adjustments)

- Cross-verification of data points across multiple secondary sources

- Normalization of inconsistent datasets

- Identification and resolution of data gaps

- Outlier detection and removal through algorithmic and manual checks

- Plausibility and coherence checks across segments and geographies

This ensured that the dataset used for modelling was clean, robust, and reliable.

Market Size Estimation and Data Triangulation

Bottom-Up Approach

The bottom-up approach involved aggregating segment-level data, such as:

- Company revenues

- Product-level sales

- Installed base/usage volumes

- Adoption and penetration rates

- Pricing analysis

This method was primarily used when detailed micro-level market data were available.

Top-Down Approach

The top-down approach used macro-level indicators:

- Parent market benchmarks

- Global/regional industry trends

- Economic indicators (GDP, demographics, spending patterns)

- Penetration and usage ratios

This approach was used for segments where granular data were limited or inconsistent.

Hybrid Triangulation Approach

To ensure accuracy, a triangulated hybrid model was used. This included:

- Reconciling top-down and bottom-up estimates

- Cross-checking revenues, volumes, and pricing assumptions

- Incorporating expert insights to validate segment splits and adoption rates

This multi-angle validation yielded the final market size.

Forecasting Framework and Scenario Modelling

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Forecasting Methods

- Time-series modelling

- S-curve and diffusion models (for emerging technologies)

- Driver-based forecasting (GDP, disposable income, adoption rates, regulatory changes)

- Price elasticity models

- Market maturity and lifecycle-based projections

Scenario Analysis

Given inherent uncertainties, three scenarios were constructed:

- Base-Case Scenario: Expected trajectory under current conditions

- Optimistic Scenario: High adoption, favourable regulation, strong economic tailwinds

- Conservative Scenario: Slow adoption, regulatory delays, economic constraints

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.

Request Customization

Add countries, segments, company profiles, or extend forecast — free 10% customization with purchase.

Customize This Report →Enquire Before Buying

Speak with our analyst team about scope, methodology, pricing, or deliverable formats.

Enquire Now →Frequently Asked Questions

Transplant Diagnostics Market Size is valued at USD 4.9 Bn in 2024 and is predicted to reach USD 10.4 Bn by the year 2034

Transplant Diagnostics Market expected to grow at a 7.9% CAGR during the forecast period for 2025-2034

BioMerieux SA, Becton, Dickinson and Company, Thermo Fisher Scientific, Bio-Rad Laboratories, Bruker, and Merck KGaA

Product & Service, Application, Technology, Transplant Type, and End-User are the key segments of the Transplant Diagnostics Market.

North America region is leading the Transplant Diagnostics Market