_Market.JPG)

Healthcare Management Service Organization (MSO) Market Size is predicted to grow at an 10.9% CAGR during the forecast period for 2024-2031.

Market info")

Management services organizations (MSOs) are administrative and management entities that provide a range of services to healthcare providers. They offer different types of governance, structure, and function tailored to the needs of individual practice associations (IPAs) or medical groups. Healthcare providers can outsource to an MSO for specific functions or a suite of services, depending on their requirements. By maintaining strong relationships with regulators and third-party contractors, MSOs help providers focus on improving medical outcomes and controlling practice expenses. MSOs operate under strict guidelines to ensure a clear separation between financial incentives and patient care decisions.

They can only receive fair market value (FMV) compensation directly from the physician, clinician, or their professional corporation, reinforcing this division. Additionally, the MSO is prohibited from directly hiring or firing clinical staff such as nurses, physician assistants, and medical assistants, as these roles require supervision by qualified medical personnel. This delineation ensures that medical decisions remain in the hands of healthcare professionals, preventing any overreach by the MSO. While the MSO can manage the patient experience and serve as the face of the practice, it cannot influence or dictate a patient's treatment plan, maintaining the integrity of medical decisions and prioritizing patient well-being above all else.

Management Services Organizations (MSOs) play a crucial role in optimizing healthcare systems. By standardizing care management across the network, MSOs ensure consistent delivery of high-quality healthcare while streamlining administrative burdens. This not only improves patient outcomes but also reduces overall costs. Additionally, MSOs are a boon for healthcare systems seeking to expand their network. By taking care of administrative tasks, MSOs free up doctors' time to focus on patient care, making the practice a more attractive option for potential partners. This creates a win-win situation for both patients and healthcare providers

Based on the by-services segment, The market is divided into Operations Management, Network Management, Quality Management, Care Management, and Other Services. Among these, the care management segment is expected to have the highest growth during the forecast period. Care Management involves coordinating and managing the care of patients, ensuring they receive the appropriate services and resources to meet their healthcare needs. Care Management strategies are integral to population health management initiatives, which aim to improve the health outcomes of entire patient populations by addressing preventive care, chronic disease management, and care coordination. By standardizing care delivery, improving population health management, and reducing costs, care management services contribute significantly to the overall value proposition of MSOs.

Based on the by ownership, the market is categorized into hospitals, physician groups, investors, and others. The hospital segment dominates the market. Hospitals are increasingly looking to MSOs as a way to expand their networks and improve operational efficiency. They may either acquire existing MSOs or create their own. Hospitals often partner with MSOs to outsource certain administrative functions, such as revenue cycle management, billing, and coding. By collaborating with MSOs, hospitals can streamline operations, reduce administrative burden, and focus more on delivering quality patient care.

The regulatory environment in North America, while complex, provides a framework that incentivizes the adoption of MSO services. Healthcare providers are increasingly under pressure to comply with regulations such as HIPAA (Health Insurance Portability and Accountability Act) and MACRA (Medicare Access and CHIP Reauthorization Act), driving the demand for MSO services to ensure compliance and mitigate regulatory risks.

|

Report Attribute |

Specifications |

|

Growth Rate CAGR |

CAGR of 10.9% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Services, By Ownership |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; South Korea; Southeast Asia |

|

Competitive Landscape |

MedVanta, Envolve Health, OneOncology, Vanguard Health Solutions, Neolytix, Argusmso, AmerisourceBergen Corporation, Other Player. |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing and Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Healthcare Management Service Organization (MSO) Market Snapshot

Chapter 4. Global Healthcare Management Service Organization (MSO) Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Industry Analysis – Porter’s Five Forces Analysis

4.7. Competitive Landscape & Market Share Analysis

4.8. Impact of Covid-19 Analysis

Chapter 5. Market Segmentation 1: By Services Estimates & Trend Analysis

5.1. By Services & Market Share, 2024 & 2034

5.2. Market Size (Value (US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following By Services:

5.2.1. Operations Management

5.2.2. Network Management

5.2.3. Quality Management

5.2.4. Care Management

5.2.5. Other Services

Chapter 6. Market Segmentation 2: By Ownership Estimates & Trend Analysis

6.1. By Ownership & Market Share, 2024 & 2034

6.2. Market Size (Value (US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following By Ownership:

6.2.1. Hospitals

6.2.2. Physician Groups

6.2.3. Investors

6.2.4. Others

Chapter 7. Healthcare Management Service Organization (MSO) Market Segmentation 3: Regional Estimates & Trend Analysis

7.1. North America

7.1.1. North America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Services, 2021-2034

7.1.2. North America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Ownership, 2021-2034

7.1.3. North America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

7.2. Europe

7.2.1. Europe Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Services, 2021-2034

7.2.2. Europe Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Ownership, 2021-2034

7.2.3. Europe Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

7.3. Asia Pacific

7.3.1. Asia Pacific Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Services, 2021-2034

7.3.2. Asia Pacific Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Ownership, 2021-2034

7.3.3. Asia Pacific Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

7.4. Latin America

7.4.1. Latin America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Services, 2021-2034

7.4.2. Latin America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Ownership, 2021-2034

7.4.3. Latin America Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

7.5. Middle East & Africa

7.5.1. Middle East & Africa Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Services, 2021-2034

7.5.2. Middle East & Africa Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by Ownership, 2021-2034

7.5.3. Middle East & Africa Healthcare Management Service Organization (MSO) Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

Chapter 8. Competitive Landscape

8.1. Major Mergers and Acquisitions/Strategic Alliances

8.2. Company Profiles

8.2.1. Advanced Medical Management

8.2.2. AmerisourceBergen Corporation

8.2.3. Argusmso

8.2.4. Conifer Health Solutions, LLC.

8.2.5. Envolve Health

8.2.6. Healthsmart MSO Inc.

8.2.7. MedPOINT Management, Inc.

8.2.8. MedVanta

8.2.9. Neolytix

8.2.10. Network Medical Management

8.2.11. OneOncology

8.2.12. Pacific Partners Management Services, Inc.

8.2.13. Vanguard Health Solutions

8.2.14. Other Prominent Players

Global Healthcare Management Service Organization (MSO) Market – By Services

Market seg")

Global Healthcare Management Service Organization (MSO) Market – By Ownership

Global Healthcare Management Service Organization (MSO) Market – By Region

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

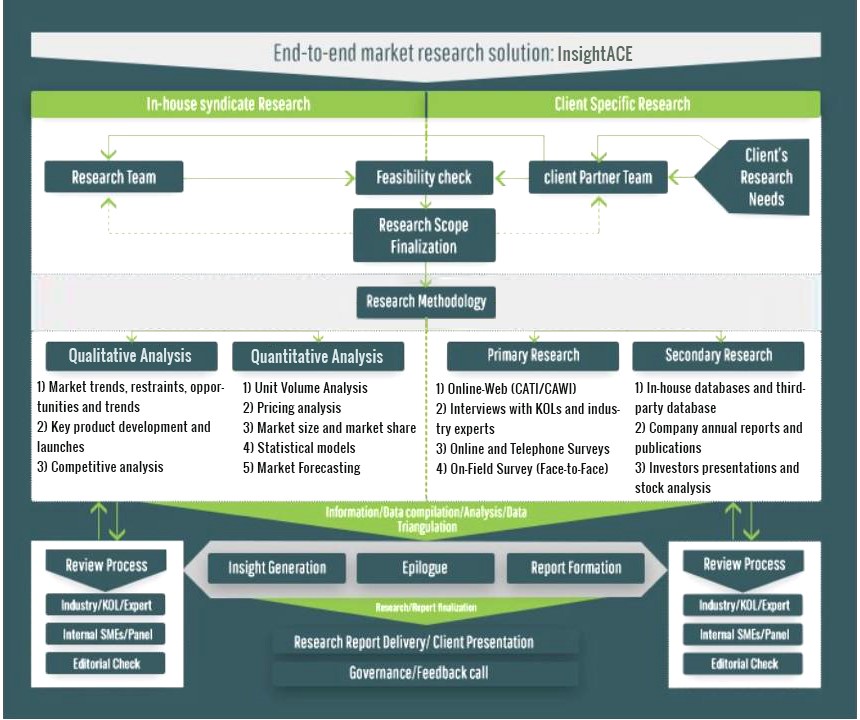

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.