Global Smart Fleet Management Market Size is valued at USD 461.5 Bn in 2024 and is predicted to reach USD 1388.9 Bn by the year 2034 at a 11.8% CAGR during the forecast period for 2025-2034. .

Smart fleet management is a collection of fleet management technologies used to manage, support, and acquire the fleet's primary, systematic activities. The supporting digital technology applications for sustenance and fuel management, driver safety, tracking, telematics, and smart surveillance drive the fast-expanding demand for the smart fleet management market.

The need to increase operational productivity and improve vehicular safety is the primary driver driving market expansion. Furthermore, the incorporation of restricted car technologies within vehicles has necessitated a plethora of solutions that can aid in improving fleet operations. Artificial Intelligence (AI), the Internet of Things (IoT), and data analytics have the potential to drive industry growth.

However, due to the commute limits, COVID-19 had a detrimental influence on the worldwide smart fleet management business. Regulatory and legislative changes, working capital management, supply chain execution, and labor dependency were all issues for the market.

On the other hand, organizations established strategic cost-cutting plans to deal with the pandemic's impact. The demand for smart fleet management hardware and managing software has skyrocketed to manage and cater to the continuing supply of basics in the post-pandemic scenario.

Competitive Landscape:

Some of the smart fleet management market players are:

- Calamp Corp.

- Cisco Systems, Inc.

- Continental Ag

- Denso Corporation

- Globecomm Systems Inc. (Speedcast International Limited)

- Globecomm Systems, Inc.

- Harman International Industries Inc.

- IBM Corporation

- International Business Machines Corporation (IBM)

- Jutha Maritime Public Company Limited

- Orbcomm, Inc.

- Otto Marine Limited

- Precious Shipping Co. Ltd.

- Robert Bosch GmbH.

- Samsung Electronics Co. Ltd. (Harman International Industries, Inc.)

- Siemens AG

- Sierra Wireless, Inc.

- Tech Mahindra Limited

Market Segmentation:

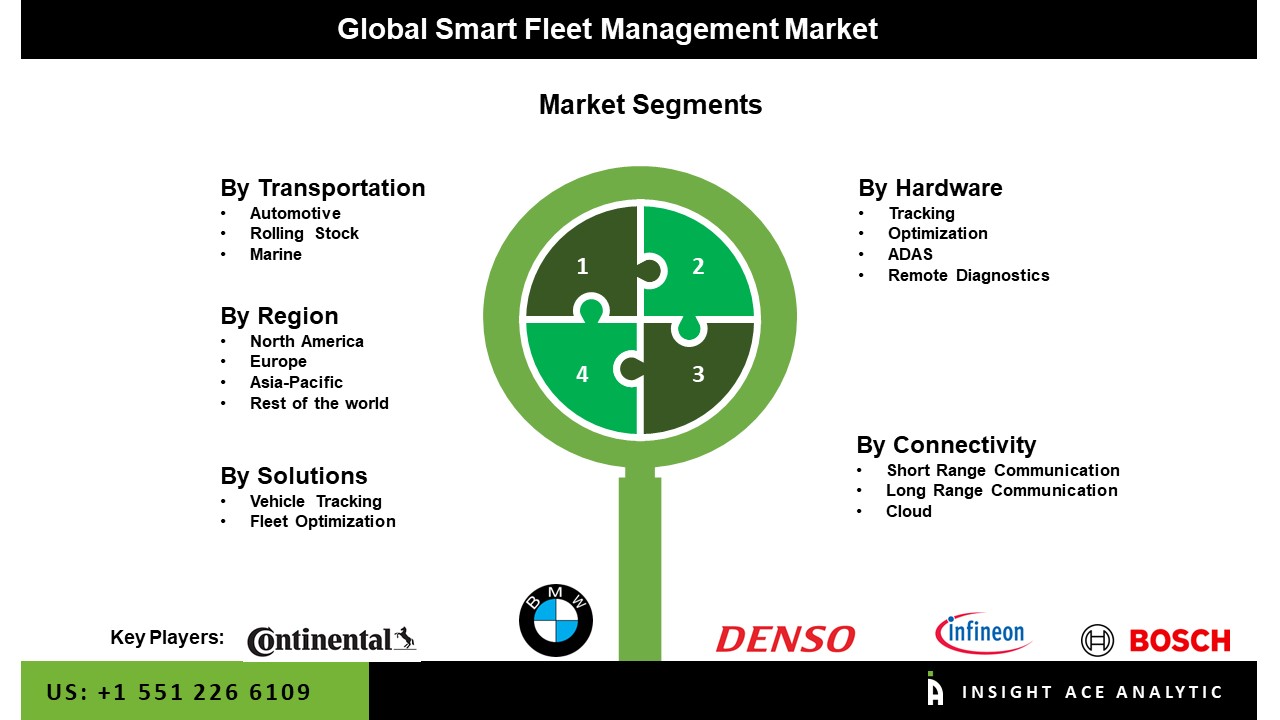

The smart fleet management market is segmented on the basis of mode of transport, hardware, connectivity, and solutions. Based on the mode of transport, the market is segmented as automotive, rolling stock, and marine. The hardware segment includes tracking, optimization, ADAS, and diagnostics. By connectivity, the market is segmented into cloud, short-range communication, and long-range communication. The solutions segment includes tracking and optimization.

Based On The Mode Of Transport, The Automotive Segment Is Valued As A Major Contributor To The Smart Fleet Management Market

The automotive category is expected to hold a major share of the global smart fleet management market in 2024. Cloud-based solutions, such as AI, IoT, and big data, are utilized to acquire primary data for fleet management. Techwave Consulting Inc., for example, employs sensors that may be implanted in cars to monitor high-value products while connecting to the cloud and transmitting data in real time. Moreover, critical operations in smart fleet management include vehicle and driver tracking, asset management, two-way communication, driver safety and time management, rescheduling delivery tasks, and others.

The Cloud Segment Witnessed Growth At A Rapid Rate

The cloud segment is projected to grow at a rapid rate in the global smart fleet management market. With a surge in demand for connectivity and fleet management solutions, smart devices and software have become the go-to tools for fleet operators. Cloud management systems handle asset tracking, driver monitoring, fleet optimization, and other associated challenges. Additionally, the cloud enables the backup and recovery of data and software on additional infrastructure or storage.

Furthermore, many firms are using various cloud models to address the shortcomings of traditional fleet management technologies.

The Asia Pacific Smart Fleet Management Market Holds A Significant Revenue Share In The Region

Asia Pacific's smart fleet management market is expected to register the highest market share in terms of revenue in the near future. The initiatives by governments to minimize carbon emissions and traffic congestion on the road have prompted fleet management firms to opt for smart fleet management solutions. This system provides real-time information to the operator/management, allowing them to make quick decisions that increase operational efficiency and help save money. Moreover, North America ranks second in the market, thanks to the region's rising fleet management services. Europe is expected to grow strongly in the market. Small fleet firms are implementing smart fleet management to keep track of cars and inventory levels.

Smart Fleet Management Market Report Scope:

|

Report Attribute

|

Specifications

|

|

Market size value in 2024

|

USD 461.5 Bn

|

|

Revenue forecast in 2034

|

USD 1388.9 Bn

|

|

Growth rate CAGR

|

CAGR of 11.8% from 2025 to 2034

|

|

Quantitative units

|

Representation of revenue in US$ Bn, and CAGR from 2025 to 2034

|

|

Historic Year

|

2021 to 2024

|

|

Forecast Year

|

2025-2034

|

|

Report coverage

|

The forecast of revenue, the position of the company, the competitive market statistics, growth prospects, and trends

|

|

Segments covered

|

Type, Application, And Distribution

|

|

Regional scope

|

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

|

|

Country scope

|

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia; South Korea; Southeast Asia

|

|

Competitive Landscape

|

Robert Bosch GmbH, Continental Ag, Denso Corporation, Harman International Industries Inc., Siemens AG, IBM Corporation, Sierra Wireless, Inc., Cisco Systems, Inc., Calamp Corp., Precious Shipping Public Company Ltd., Otto Marine Limited, Orbcomm, Inc., Jutha Maritime Public Company Limited, Globecomm Systems, Inc.

|

|

Customization scope

|

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape.

|

|

Pricing and available payment methods

|

Explore pricing alternatives that are customized to your particular study requirements.

|

Segmentation of Smart Fleet Management Market-

Smart Fleet Management Market By Mode of Transport-

- Automotive

- Rolling Stock

- Marine

Smart Fleet Management Market By Hardware-

- Tracking

- Optimization

- ADAS

- Diagnostics

Smart Fleet Management Market By Connectivity-

- Cloud

- Short Range Communication

- Large Range Communication

Smart Fleet Management Market By Solutions-

Smart Fleet Management Market By Region-

North America-

Europe-

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

Asia-Pacific-

- China

- Japan

- India

- South Korea

- South East Asia

- Rest of Asia Pacific

Latin America-

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Middle East & Africa-

- GCC Countries

- South Africa

- Rest of the Middle East and Africa