Rare Disease Clinical Trials Market Size, Share & Trends Analysis Report By Therapeutic Area (Oncology, Cardiovascular Disorders, Neurological Disorders, Infectious Disease, Genetic Disorders, Autoimmune and Inflammation, Hematologic Disorders, Musculoskeletal Disorders), Phase (Phase I, II, III, and IV), And Sponsor, By Region, And Segment Forecasts, 2024-2031

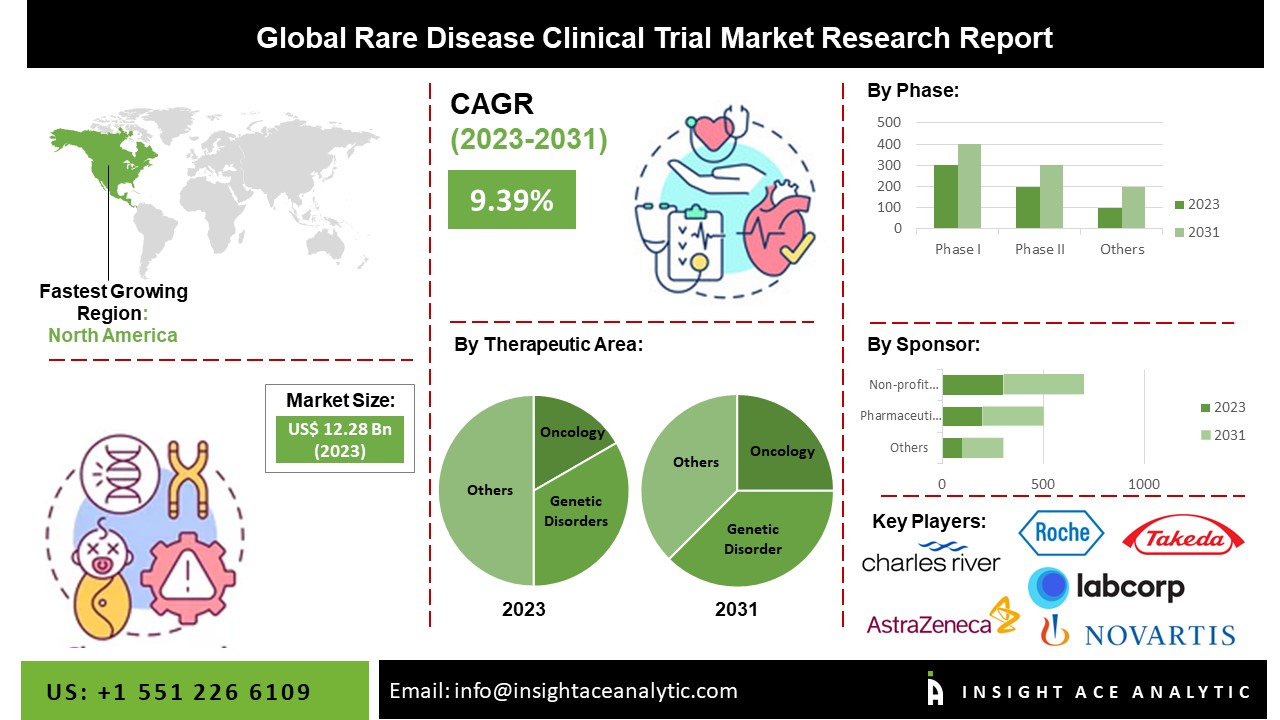

The Global Rare Disease Clinical Trials Market Size is valued at 12.28 billion in 2023 and is predicted to reach 25.05 billion by the year 2031 at a 9.39% CAGR during the forecast period for 2024-2031.

The lack of medications available to treat rare diseases, advancements in personalized medicine, and cell and gene therapies, which are opening up new pathways for new treatments for rare diseases, are a few of the causes contributing to this expansion. Also, a rise in financing for clinical trials for rare diseases from pharmaceutical, biotech, and non-profit groups is driving market expansion.

The COVID-19 outbreak significantly impacted the capacity to perform clinical trials. The pandemic forced the suspension and postponement of numerous clinical trials for uncommon diseases and the delay of participant recruitment. Due to this, new medications and therapies created for the treatment of rare diseases took longer. However, by the second half of 2020, clinical studies of rare illnesses had resumed, and they have now begun. This is likely to sustain the industry throughout the post-pandemic phase.

Recent Developments:

- In January 2023, Genethon, an R&D company, began a crucial clinical trial for the use of gene therapy to treat Crigler-Najjar Syndrome. Crigler-Najjar syndrome is a rare genetic liver disease marked by abnormally elevated bilirubin levels in the blood. (hyperbilirubinemia).

- In November 2022, The Biologics License Application (BLA) for PRX-102 (pegunigalsidasealfa) for the treatment of adult patients with Fabry disease was re-submitted to the US Food and Drug Administration (FDA) by ProtalixBiotherapeutics Inc. and Chiesi Global Rare Diseases.

Competitive Landscape:

Some of the Rare Disease Clinical Trials market players are:

- Takeda Pharmaceutical Company;

- Hoffmann-La Roche Ltd.;

- Pfizer, Inc.;

- AstraZeneca;

- Novartis AG;

- LabCorp;

- IQVIA, Inc.;

- Charles River Laboratories;

- Icon PLC;

- Parexel International Corporation

Market Segmentation:

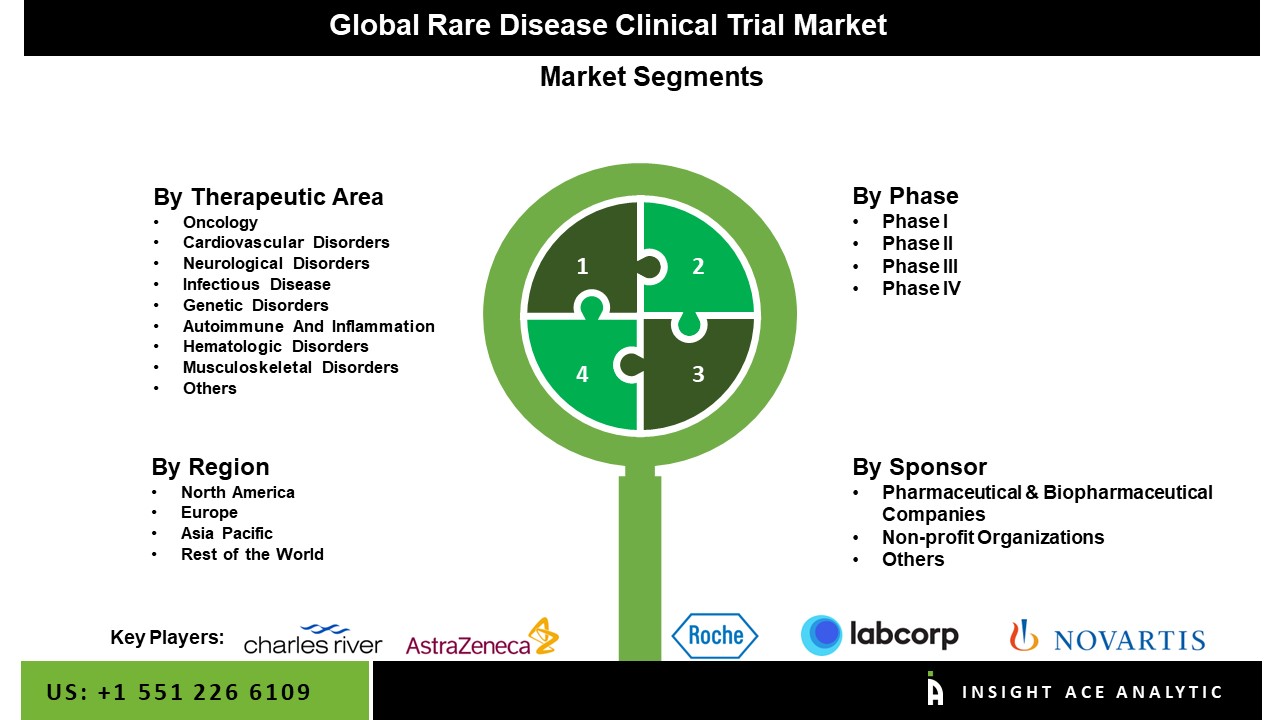

The Rare Disease Clinical Trials market is segmented by therapeutic area, phase, and sponsor. Based on the therapeutic site, the market is segmented as Oncology, Cardiovascular Disorders, Neurological Disorders, Infectious Disease, Genetic Disorders, Autoimmune and Inflammation, Hematologic Disorders, Musculoskeletal Disorders, and Others. By phase the market is segmented into Phase I, II, III, and IV. By drug, the market is segmented as OTC and Rx. By sponsor, the market is segmented as Pharmaceutical & Biopharmaceutical Companies, Non-profit Organizations, and Others.

Based On Phase, Phase II Is Accounted As A Significant Contributor In The Rare Disease Clinical Trials Market

The majority belonged to Phase II. Phase II studies are carried out in two stages; the first stage combines efficacy and dose range exploration; the second stage finalises the dose. Between 100 to 300 people are enrolled in Phase II clinical trials. The phase II category had the most registered clinical studies as of November 2022. On the ClinicalTrial.gov portal, 72,522 research had been registered as of November 2022. The large number of Phase II clinical studies is assisting in the segment's expansion.

Oncology Segment Witness Growth At A Rapid Rate

The largest share belonged to the oncology sector. Some of the main drivers of the segment's growth are the high number of cancer drug approvals for rare diseases, the rise in cancer clinical trials, and the increased interest among scientists in developing effective treatments for uncommon malignancies. As an illustration, the USFDA authorised the immunotherapy medication atezolizumab (Tecentriq) in January 2023 for use in patients with advanced alveolar soft part sarcoma (ASPS).

The North America Rare Disease Clinical Trials Market Holds Significant Revenue Share In The Region

Due to advantageous reimbursement rules, increased spending on orphan pharmaceuticals for the treatment of rare diseases, and the existence of prominent market participants who encouraged the creation of novel products, North America accounted for the most significant revenue share. Moreover, the U.S. FDA can approve medications used to treat critical disorders quickly. The FDA's drug approval procedure is streamlined by the Accelerated Approval Rules, which permit a treatment used to treat a critical ailment to be approved using a surrogate end-point. All of these elements are anticipated to boost the North American market.

Rare Disease Clinical Trials Market Report Scope:

| Report Attribute | Specifications |

| Market size value in 2023 | USD 12.28 Bn |

| Revenue forecast in 2031 | USD 25.50 Bn |

| Growth rate CAGR | CAGR of 9.39% from 2024 to 2031 |

| Quantitative units | Representation of revenue in US$ Billion, and CAGR from 2024 to 2031 |

| Historic Year | 2019 to 2023 |

| Forecast Year | 2023-2031 |

| Report coverage | The forecast of revenue, the position of the company, the competitive market statistics, growth prospects, and trends |

| Segments covered | Therapeutic Area, Phase, And Sponsor |

| Regional scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia; South Korea; Southeast Asia |

| Competitive Landscape | Takeda Pharmaceutical Company; F. Hoffmann-La Roche Ltd.; Pfizer, Inc.; AstraZeneca; Novartis AG; LabCorp; IQVIA, Inc.; Charles River Laboratories; Icon PLC; Parexel International Corporation. |

| Customization scope | Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

| Pricing and available payment methods | Explore pricing alternatives that are customized to your particular study requirements. |

Segmentation of Rare Disease Clinical Trials Market-

Rare Disease Clinical Trials Market By Therapeutic area-

- Oncology

- Cardiovascular Disorders

- Neurological Disorders

- Infectious Disease

- Genetic Disorders

- Autoimmune and Inflammation

- Hematologic Disorders

- Musculoskeletal Disorders

- Others

Rare Disease Clinical Trials Market By Phase-

- Phase I

- Phase II

- Phase III

- Phase IV

Rare Disease Clinical Trials Market By Sponsor-

- Pharmaceutical & Biopharmaceutical Companies

- Non-profit Organizations

- Others

Rare Disease Clinical Trials Market By Region-

North America-

- The US

- Canada

- Mexico

Europe-

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

Asia-Pacific-

- China

- Japan

- India

- South Korea

- South East Asia

- Rest of Asia Pacific

Latin America-

- Brazil

- Argentina

- Rest of Latin America

Middle East & Africa-

- GCC Countries

- South Africa

- Rest of Middle East and Africa

Research Design and Approach

This study employed a multi-step, mixed-method research approach that integrates:

- Secondary research

- Primary research

- Data triangulation

- Hybrid top-down and bottom-up modelling

- Forecasting and scenario analysis

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary Research

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Sources Consulted

Secondary data for the market study was gathered from multiple credible sources, including:

- Government databases, regulatory bodies, and public institutions

- International organizations (WHO, OECD, IMF, World Bank, etc.)

- Commercial and paid databases

- Industry associations, trade publications, and technical journals

- Company annual reports, investor presentations, press releases, and SEC filings

- Academic research papers, patents, and scientific literature

- Previous market research publications and syndicated reports

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

Primary Research

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Stakeholders Interviewed

Primary interviews for this study involved:

- Manufacturers and suppliers in the market value chain

- Distributors, channel partners, and integrators

- End-users / customers (e.g., hospitals, labs, enterprises, consumers, etc., depending on the market)

- Industry experts, technology specialists, consultants, and regulatory professionals

- Senior executives (CEOs, CTOs, VPs, Directors) and product managers

Interview Process

Interviews were conducted via:

- Structured and semi-structured questionnaires

- Telephonic and video interactions

- Email correspondences

- Expert consultation sessions

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

Data Processing, Normalization, and Validation

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

- Standardization of units (currency conversions, volume units, inflation adjustments)

- Cross-verification of data points across multiple secondary sources

- Normalization of inconsistent datasets

- Identification and resolution of data gaps

- Outlier detection and removal through algorithmic and manual checks

- Plausibility and coherence checks across segments and geographies

This ensured that the dataset used for modelling was clean, robust, and reliable.

Market Size Estimation and Data Triangulation

Bottom-Up Approach

The bottom-up approach involved aggregating segment-level data, such as:

- Company revenues

- Product-level sales

- Installed base/usage volumes

- Adoption and penetration rates

- Pricing analysis

This method was primarily used when detailed micro-level market data were available.

Top-Down Approach

The top-down approach used macro-level indicators:

- Parent market benchmarks

- Global/regional industry trends

- Economic indicators (GDP, demographics, spending patterns)

- Penetration and usage ratios

This approach was used for segments where granular data were limited or inconsistent.

Hybrid Triangulation Approach

To ensure accuracy, a triangulated hybrid model was used. This included:

- Reconciling top-down and bottom-up estimates

- Cross-checking revenues, volumes, and pricing assumptions

- Incorporating expert insights to validate segment splits and adoption rates

This multi-angle validation yielded the final market size.

Forecasting Framework and Scenario Modelling

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Forecasting Methods

- Time-series modelling

- S-curve and diffusion models (for emerging technologies)

- Driver-based forecasting (GDP, disposable income, adoption rates, regulatory changes)

- Price elasticity models

- Market maturity and lifecycle-based projections

Scenario Analysis

Given inherent uncertainties, three scenarios were constructed:

- Base-Case Scenario: Expected trajectory under current conditions

- Optimistic Scenario: High adoption, favourable regulation, strong economic tailwinds

- Conservative Scenario: Slow adoption, regulatory delays, economic constraints

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.

Request Customization

Add countries, segments, company profiles, or extend forecast — free 10% customization with purchase.

Customize This Report →Enquire Before Buying

Speak with our analyst team about scope, methodology, pricing, or deliverable formats.

Enquire Now →Frequently Asked Questions

The Global Rare Disease Clinical Trials Market Size is valued at 12.28 billion in 2023 and is predicted to reach 25.05 billion by the year 2031

Rare Disease Clinical Trials Market expected to grow at a 9.39% CAGR during the forecast period for 2024-2031

Takeda Pharmaceutical Company; F. Hoffmann-La Roche Ltd.; Pfizer, Inc.; AstraZeneca; Novartis AG; LabCorp; IQVIA, Inc