Precision Diagnostics & Medicine Market Size was valued at USD 138.4 Bn in 2024 and is predicted to reach USD 425.9 Bn by 2034 at a 12.3% CAGR during the forecast period for 2025-2034.

The rapidly developing discipline of precision diagnostics and medicine focuses on customising medical interventions and diagnostic processes to each patient's unique characteristics. It entails applying cutting-edge technologies, such as biomarkers, proteomics, and genomics, to deliver more precise and individualised healthcare treatments. By considering the environmental, genetic, and behavioural factors that influence a patient's health, this approach aims to enhance the effectiveness of treatments. The precision diagnostics and medicine market is expanding due to factors such as the continuous integration of cutting-edge technologies, including AI and machine learning, to improve precision diagnostics and medicine development. Additionally, the growing cooperation and investments made by significant pharmaceutical and diagnostics companies are creating better precision diagnostics and medicine solutions. Furthermore, the rising emphasis of these businesses on creating precision treatments and diagnostic tools for various illnesses, including autoimmune and neurodegenerative conditions, underscores the growing significance of precision diagnostics and medicine in healthcare.

In addition, wearable medical technology and direct-to-consumer precision diagnostic tests are gaining popularity due to patients' increasing health awareness, presenting potential opportunities for market participants. However, it is anticipated that the high expense of precision healthcare and the difficulties in integrating and managing large datasets in the healthcare industry will limit the expansion of the precision diagnostics and medicine market.

The precision diagnostics & medicine market is segmented based on type, product, indication, and end-user. Based on type, the market is segmented into genetic testing, DTC testing, and others. By product, the market is segmented into monoclonal antibodies, inhibitor drugs, cell & gene therapies, antiviral & anti- retroviral drugs, and others. By indication, the market is segmented into diagnostics (oncology, neurology, immunology, others) and medicine (oncology, rare diseases, infectious diseases, hematological disorders, others). By end-user, the market is segmented into clinical laboratories, hospitals, home care settings, and others.

The monoclonal antibodies segment is expected to hold a major global market share in 2024. The expansion of this market is attributed to factors such as the increasing number of partnerships to develop sophisticated monoclonal antibodies and advancements in antibody engineering technologies. The use of these drug modalities for the treatment of infectious, autoimmune, and cancerous diseases is also growing as a result of their many benefits over conventional medications, including high specificity, low toxicity, and longer-lasting effects.

During the projection period, the diagnostic laboratories segment grew at the fastest rate. Advancements in molecular diagnostic technologies, such as next-generation sequencing and biomarker analysis, enable more accurate and personalized testing, increasing demand for specialized lab services. The expansion of this market is also aided by the growing partnerships between pharmaceutical and diagnostic firms and hospitals to create customized treatments and diagnostic procedures.

The North American precision diagnostics & medicine market is expected to register the highest market share in revenue in the near future propelled by its robust biotechnology research areas and sophisticated healthcare infrastructure. Innovations that improve the effectiveness and dependability of individualized diagnostics technologies are the consequence of ongoing investments in these fields. The industry has grown as a result of government efforts to enhance healthcare accessibility and quality as well as significant investment in R&D. In addition, Asia Pacific is projected to grow rapidly in the global precision diagnostics & medicine market, especially in nations like China and India, where government funding for cutting-edge medical technology and upgrades to healthcare infrastructure are expanding market potential. The market has grown as a result of the growing incidence of chronic illnesses including diabetes and cancer, as well as growing knowledge of individualized therapies.

|

Report Attribute |

Specifications |

|

Market Size Value In 2024 |

USD 138.4 Bn |

|

Revenue Forecast In 2034 |

USD 425.9 Bn |

|

Growth Rate CAGR |

CAGR of 12.3% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Type, By Indication, By Product, By End-user |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South East Asia; South Korea |

|

Competitive Landscape |

F. Hoffmann-La Roche Ltd, Eli Lilly and Company, Pfizer Inc., GSK plc, Sanofi, Johnson & Johnson Services, Inc., Vertex Pharmaceuticals Incorporated, Agilent Technologies, Inc., Thermo Fisher Scientific Inc., Myriad Genetics, Inc., Guardant Health, Abbott, AstraZeneca, AbbVie Inc., Amgen Inc., Merck KgaA, Sarepta Therapeutics, Inc., Merck & Co., Inc., Natera, Inc., ARUP Laboratories, Devyser, Diasorin S.P.A., Tempus, Illumina, Inc., Danaher, Exact Sciences Corporation, Qiagen, 23andMe, Inc., Trinity Biotech Plc, Amoy Diagnostics Co., Ltd., Novartis AG, Bristol-Myers Squibb Company, Gilead Sciences, Inc., Pillar Biosciences Inc., Invivoscribe, Inc., NeuroCode, C2N Diagnostics, and other organizations. |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Precision Diagnostics & Medicine Market Snapshot

Chapter 4. Global Precision Diagnostics & Medicine Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2024-2034

4.8. Competitive Landscape & Market Share Analysis, By Key Player (2023)

4.9. Use/impact of AI on Precision Diagnostics & Medicine Market Trends

4.10. Global Precision Diagnostics & Medicine Market Penetration & Growth Prospect Mapping (US$ Mn), 2021-2034

Chapter 5. Precision Diagnostics & Medicine Market Segmentation 1: By Type, Estimates & Trend Analysis

5.1. Market Share by Type, 2024 & 2034

5.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following Type:

5.2.1. Precision Diagnostics

5.2.1.1. Genetic Testing

5.2.1.2. DTC Testing

5.2.1.3. Other Types

5.2.2. Precision Medicine

5.2.2.1. Monoclonal Antibodies

5.2.2.2. Inhibitor Drugs

5.2.2.3. Cell & Gene Therapies

5.2.2.4. Antiviral & Anti-Retroviral Drugs

5.2.2.5. Other Products

Chapter 6. Precision Diagnostics & Medicine Market Segmentation 2: Indication, Estimates & Trend Analysis

6.1. Market Share by Indication, 2024 & 2034

6.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following Indication:

6.2.1. Precision Diagnostics

6.2.1.1. Oncology

6.2.1.2. Neurology

6.2.1.3. Immunology

6.2.1.4. Other Diagnostic Indications

6.2.2. Precision Medicine

6.2.2.1. Oncology

6.2.2.2. Rare Diseases

6.2.2.3. Infectious Diseases

6.2.2.4. Hematological Disorders

6.2.2.5. Other Medicine Indications

Chapter 7. Precision Diagnostics & Medicine Market Segmentation 3: By End User, Estimates & Trend Analysis

7.1. Market Share by End User, 2024 & 2034

7.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following End User:

7.2.1. Clinical Laboratories

7.2.2. Hospitals

7.2.3. Home Care Settings

Chapter 8. Precision Diagnostics & Medicine Market Segmentation 6: Regional Estimates & Trend Analysis

8.1. Global Precision Diagnostics & Medicine Market, Regional Snapshot 2024 & 2034

8.2. North America

8.2.1. North America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.2.1.1. US

8.2.1.2. Canada

8.2.2. North America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.2.3. North America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Indication, 2021-2034

8.2.4. North America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by End User, 2021-2034

8.3. Europe

8.3.1. Europe Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.3.1.1. Germany

8.3.1.2. U.K.

8.3.1.3. France

8.3.1.4. Italy

8.3.1.5. Spain

8.3.1.6. Rest of Europe

8.3.2. Europe Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.3.3. Europe Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Indication, 2021-2034

8.3.4. Europe Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by End User, 2021-2034

8.4. Asia Pacific

8.4.1. Asia Pacific Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.4.1.1. India

8.4.1.2. China

8.4.1.3. Japan

8.4.1.4. Australia

8.4.1.5. South Korea

8.4.1.6. Hong Kong

8.4.1.7. Southeast Asia

8.4.1.8. Rest of Asia Pacific

8.4.2. Asia Pacific Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.4.3. Asia Pacific Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Indication, 2021-2034

8.4.4. Asia Pacific Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by End User, 2021-2034

8.5. Latin America

8.5.1. Latin America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.5.1.1. Brazil

8.5.1.2. Mexico

8.5.1.3. Rest of Latin America

8.5.2. Latin America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.5.3. Latin America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Indication, 2021-2034

8.5.4. Latin America Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by End User, 2021-2034

8.6. Middle East & Africa

8.6.1. Middle East & Africa Wind Turbine Rotor Blade Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

8.6.1.1. GCC Countries

8.6.1.2. Israel

8.6.1.3. South Africa

8.6.1.4. Rest of Middle East and Africa

8.6.2. Middle East & Africa Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.6.3. Middle East & Africa Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by Indication, 2021-2034

8.6.4. Middle East & Africa Precision Diagnostics & Medicine Market Revenue (US$ Million) Estimates and Forecasts by End User, 2021-2034

Chapter 9. Competitive Landscape

9.1. Major Mergers and Acquisitions/Strategic Alliances

9.2. Company Profiles

9.2.1. F. Hoffmann-La Roche Ltd (Switzerland)

9.2.1.1. Business Overview

9.2.1.2. Key Offering/Service Overview

9.2.1.3. Financial Performance

9.2.1.4. Geographical Presence

9.2.1.5. Recent Developments with Business Strategy

9.2.2. Agilent Technologies, Inc. (US)

9.2.3. Thermo Fisher Scientific Inc. (US)

9.2.4. Myriad Genetics, Inc. (US)

9.2.5. Guardant Health (US)

9.2.6. Abbott (US)

9.2.7. Illumina, Inc. (US)

9.2.8. Danaher (US)

9.2.9. Exact Sciences Corporation (US)

9.2.10. Qiagen (Netherlands)

9.2.11. 23andME, INC. (US)

9.2.12. ARUP Laboratories. (US)

9.2.13. Devyser (Sweden)

9.2.14. Diasorin S.P.A. (Italy)

9.2.15. Tempus (US)

9.2.16. Pillar Biosciences Inc. (US)

9.2.17. Invivoscribe, Inc. (US)

9.2.18. NeuroCode (US)

9.2.19. C2N Diagnostics (US)

9.2.20. Trinity Biotech Plc. (Ireland)

9.2.21. Amoy Diagnostics Co., Ltd. (China)

9.2.22. Novartis AG (Switzerland)

9.2.23. Bristol-Myers Squibb Company (US)

9.2.24. Gilead Sciences, Inc (US)

9.2.25. AstraZeneca (UK)

9.2.26. AbbVie Inc. (US)

9.2.27. Eli Lilly and Company (US)

9.2.28. Pfizer Inc. (US)

9.2.29. GSK plc. (UK)

9.2.30. Sanofi (France)

9.2.31. Johnson & Johnson Services, Inc. (US)

9.2.32. Vertex Pharmaceuticals Incorporated (US)

9.2.33. Amgen Inc. (US)

9.2.34. Merck KGaA (Germany)

9.2.35. Sarepta Therapeutics, Inc. (US)

9.2.36. Merck & Co., Inc.

9.2.37. Natera, Inc.

Precision Diagnostics & Medicine Market-By Type

Precision Diagnostics & Medicine Market-By Product

Precision Diagnostics & Medicine Market-By Indication

Precision Diagnostics & Medicine Market-By End-User

Precision Diagnostics & Medicine Market-By Region

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

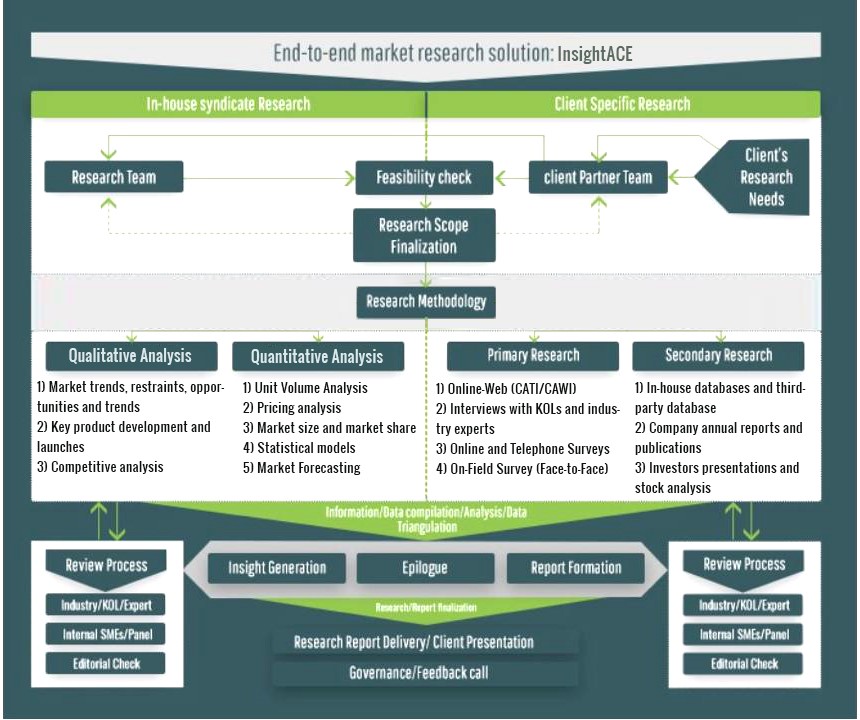

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.