The Lead-Acid Battery Scrap Market Size is valued at USD 12.8 billion in 2023 and is predicted to reach USD 25.7 billion by the year 2031 at a 9.3% CAGR during the forecast period for 2024-2031.

Lead-acid battery scrap refers to batteries that have been used or discarded and yet contain precious lead, which can be able to be repurposed. The recycling process entails the segregation and purification of the lead, the neutralization of the acid, and the reuse of the plastic casing. Efficient recycling is crucial for minimizing environmental contamination and preserving resources, while also yielding economic benefits by reclaiming lead.

In automobiles, industrial settings, and electrical backup networks, lead-acid batteries are widely utilized. Both private and public sectors are investing in these systems to recycle lead-acid batteries more effectively. Facilities for recycling spent batteries remove important lead, guaranteeing appropriate disposal and reducing the ecological impact. Utilized in a variety of sectors, recycled lead promotes an economy with circularity that is environmentally friendly. Growing industry and consumer recognition of a demand for sustainable methods is driving the industry significantly.

However, the global lead-acid battery scrap industry is confronted with enormous challenges in terms of regulation and compatibility. The recycling technologies and procedures. Thus, it might be difficult to achieve integrated and defined norms. The absence of global standards frequently leads to incompatibilities, which impedes recycling facilities' ability to exchange information and interact efficiently. The absence of connectivity hampers the sector's capacity to achieve effective substance recoveries and improved efficiency. Irregular standards may result in errors, higher operating expenses, and less-than-ideal cleaning products. In the wake of the COVID-19 epidemic and subsequent lockdown, there was a decline in consumer demand for lead-acid batteries. Many different businesses were impacted by this, including those who make and recycle batteries.

The lead-acid battery scrap market is segmented based on battery, product, and source. As per the battery, the market is segmented into flooded and sealed. By product, the market is segmented into lead and sulfuric acid. According to sources, the market is segmented into motor vehicles and U.P.S.

The sealed lead-acid battery scrap is expected to hold a major global market share in 2023. Because these batteries are sealed, the electrolytes cannot leak or spill out, increasing their dependability and suitability for uses where comfort and security are crucial. Sealed lead-acid batteries are the most common type of battery in the scrap industry since they are used in many industries, including automobile connectivity, energy efficiency systems, and electrical power supplies.

Motor vehicles make up the bulk of lead-acid battery usage due to elements like the flourishing motoring sector, rising vehicle ownership rates, and the increasing need for battery-powered cars (E.V.s) with lithium-ion batteries in supporting technologies. Lead-acid battery recycling has increased proportionately as a result of the growth of electronic commerce and the logistics sector, as well as a surge in the number of automobiles on motorways, especially in countries like the US, Germany, the U.K., China, and India.

The North American lead-acid battery scrap market is expected to register the very big market share in revenue in the near future. This can be attributed to the fact that its people tend to be well-off and educated. Increasing lead-acid battery use in the region meets the rising need for batteries across various industries, including smart cards, packaging, and electric vehicles. In addition, Asia Pacific is estimated to grow rapidly in the global lead-acid battery market due to advancements in the renewable energy sector, an ever-increasing need for battery energy storage devices, and a massive consumer user base for consumer and portable electronics.

| Report Attribute | Specifications |

| Market Size Value In 2023 | USD 12.8 Bn |

| Revenue Forecast In 2031 | USD 25.7 Bn |

| Growth Rate CAGR | CAGR of 9.3% from 2024 to 2031 |

| Quantitative Units | Representation of revenue in US$ Bn and CAGR from 2024 to 2031 |

| Historic Year | 2019 to 2023 |

| Forecast Year | 2024-2031 |

| Report Coverage | The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

| Segments Covered | By Battery, Product, And Source. |

| Regional Scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country Scope | U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South East Asia; South Korea |

| Competitive Landscape | Johnson Controls International PLC, Exide Technologies S.A.S., East Penn Manufacturing Co., Inc., GS Yuasa International Ltd., Battery Solutions LLC, Whitelake Organics Pvt Ltd., Gravita India Ltd., Aqua Metals Inc., Madenat Al Nokhba Recycling Services LLC, Beeah Group. And other market players |

| Customization Scope | Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

| Pricing And Available Payment Methods | Explore pricing alternatives that are customized to your particular study requirements. |

Lead-Acid Battery Scrap Market By Battery

Lead-Acid Battery Scrap Market By Product

Lead-Acid Battery Scrap Market By Source

Lead-Acid Battery Scrap Market By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

This study employed a multi-step, mixed-method research approach that integrates:

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Secondary data for the market study was gathered from multiple credible sources, including:

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

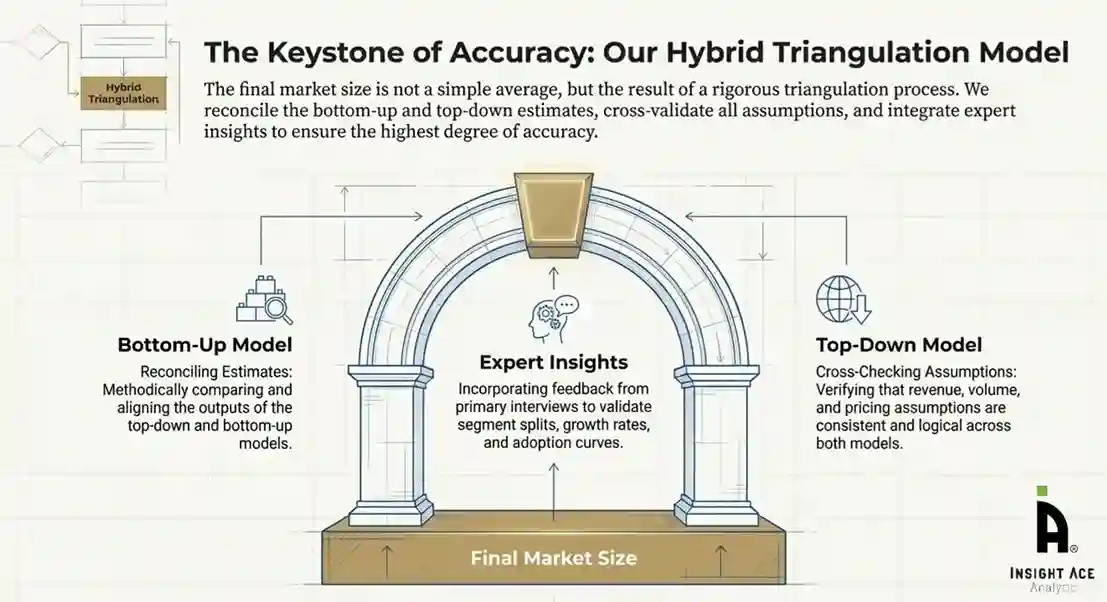

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Primary interviews for this study involved:

Interviews were conducted via:

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

This ensured that the dataset used for modelling was clean, robust, and reliable.

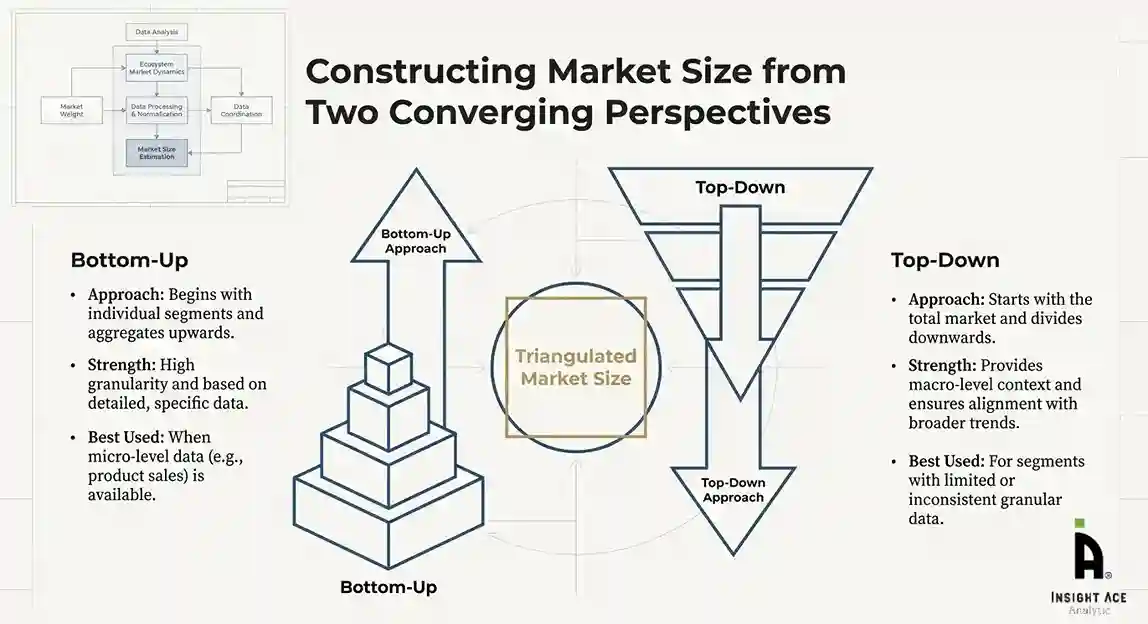

The bottom-up approach involved aggregating segment-level data, such as:

This method was primarily used when detailed micro-level market data were available.

The top-down approach used macro-level indicators:

This approach was used for segments where granular data were limited or inconsistent.

To ensure accuracy, a triangulated hybrid model was used. This included:

This multi-angle validation yielded the final market size.

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Given inherent uncertainties, three scenarios were constructed:

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.