Global Drug Infusion Systems Market

Share With :

Drug infusion systems are used across pharmacological therapies to administer various drugs including antibiotics, insulin, chemotherapy drugs, painkillers, intravenously or through non-oral routes, like epidural routes and intramuscular injections in a controlled manner.

The Global drug infusion system market is expected to offer lucrative growth in the coming years owing to the increasing prevalence of chronic diseases and rising geriatric population across the globe.

The rise in chronic diseases has led to high demand for better medicines and facilities. For instance, as per the latest estimates by the IDF Diabetes Atlas Ninth edition 2019, around 463 million people aged between 20-79 years were living with diabetes in 2019; the number is estimated to reach 700 million by 2045. Moreover, the prevalence of genetic diseases and cancer has witnessed an upsurge in recent years. For the advanced and continued care of the patients, the drug infusion systems are being extensively used in hospitals and critical care centers.

On the other side, the high cost of the drug infusion system and stringent government regulations are expected to restrain the market's growth during the forecast period.

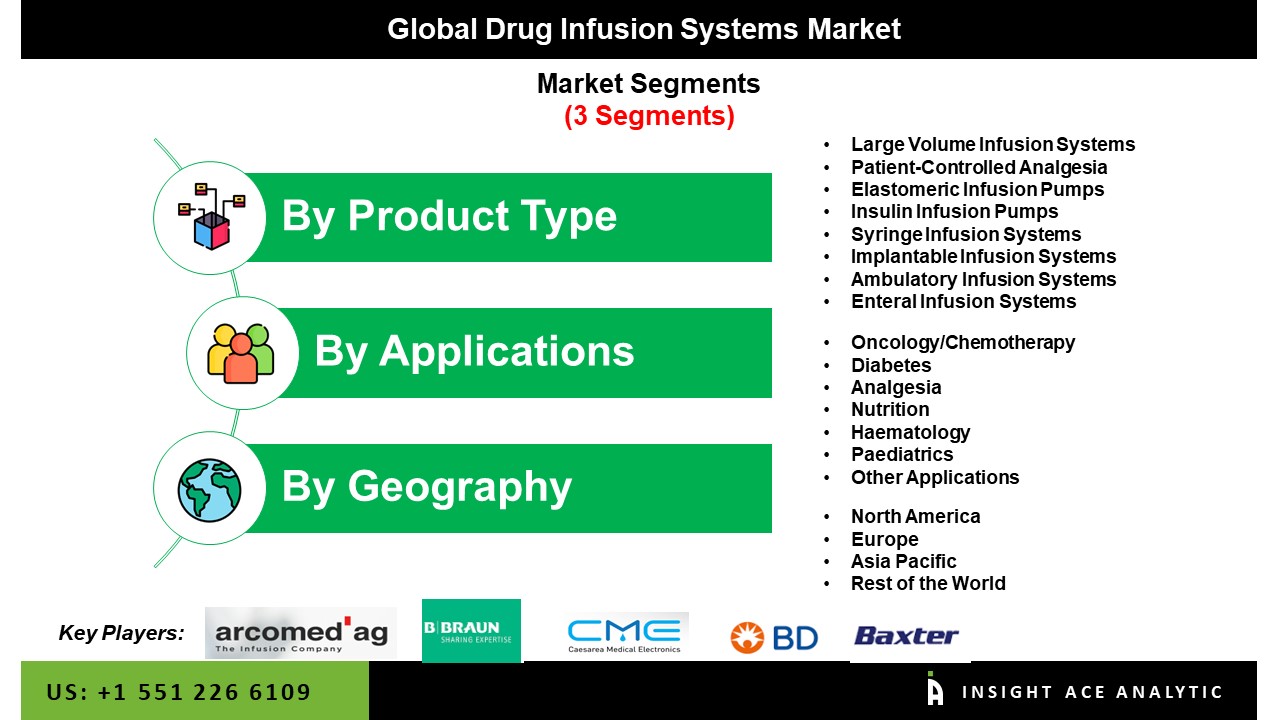

The Global Drug infusion systems market is segmented on the basis of product type, application, and region. Based on the product type, the market is divided into large volume infusion systems, patient-controlled analgesia, elastomeric infusion pumps, insulin infusion pumps, syringe infusion systems, implantable infusion systems, ambulatory infusion systems, and enteral infusion systems. On the basis of application, the market is divided into oncology/chemotherapy, diabetes, analgesia, nutrition, haematology, pediatrics, and other applications.

Based on the region, the market is studied across North America, Asia-Pacific, Europe, and LAMEA. North America held the largest share of the market in 2019, followed by Europe and Asia Pacific. However, the Asia Pacific is projected to have the highest growth rate during the forecast period.

The key players operating in the market include Acromed AG, B. Braun Melsungen AG, Baxter International Inc., Becton, Dickinson and Company, Caesarea Medical Electronics Ltd., Debiotech S.A., Flowonix Medical Inc., Fresenius SE & Co. KGaA, Halyard Health, Inc., ICU Medical Inc., IRADIMED CORPORATION, Insulet Corporation, Medtronic, MOOG, Inc., Smiths Group plc, Tandem Diabetes Care, Inc., Terumo Corporation and Zyno Medical, LLC among others.

Global Drug Infusion Systems Market Segmentation:

Global Drug Infusion Systems Market Revenue (US$ Mn), by Product Type, 2019–2030

Global Drug Infusion Systems Market Revenue(US$ Mn), by Applications, 2019–2030

Global Drug Infusion Systems Market Revenue(US$ Mn), by Region, 2019–2030

North America Drug Infusion Systems Market Revenue (US$ Mn) by Country, 2019–2030

Europe Drug Infusion Systems Market Revenue (US$ Mn), by Country, 2019–2030

Asia Pacific Drug Infusion Systems Market Revenue (US$ Mn), by Country, 2019–2030

Latin America Drug Infusion Systems Market Revenue (US$ Mn), by Country, 2019–2030

Middle East & Africa Drug Infusion Systems Market Revenue (US$ Mn), by Country, 2019–2030

This study employed a multi-step, mixed-method research approach that integrates:

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Secondary data for the market study was gathered from multiple credible sources, including:

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Primary interviews for this study involved:

Interviews were conducted via:

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

This ensured that the dataset used for modelling was clean, robust, and reliable.

The bottom-up approach involved aggregating segment-level data, such as:

This method was primarily used when detailed micro-level market data were available.

The top-down approach used macro-level indicators:

This approach was used for segments where granular data were limited or inconsistent.

To ensure accuracy, a triangulated hybrid model was used. This included:

This multi-angle validation yielded the final market size.

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Given inherent uncertainties, three scenarios were constructed:

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.