Food Texture Market Size is valued at USD 14.16 Bn in 2023 and is predicted to reach USD 22.67 Bn by the year 2031 at a 6.25% CAGR during the forecast period for 2024-2031.

Food texture refers to the qualities of a dish that can be felt when eating it, both in the mouth and on the hands. Soft, firm, mushy, crunchy, smooth, and lumpy are just a few of the terms we use to describe the texture of food. Foods are more likely to be liked and eaten when they have a certain texture. Food texturization compounds enhance the food in some way, whether by increased viscosity, thickness, creaminess, clarity, or some other attribute. Although consumers universally acknowledge the significance of flavor, texture can sometimes be disregarded. Many available texturizing additives can give food new flavours and textures. The combination or combination of usage establishes the final feel of the product. They strengthen food, which lengthens the time it may be stored. In addition to the functional potential of texturizing agents in new product lines and applications, rising consumer demand for convenience or ready-to-eat products instead of fresh items also contributes to the market's rapid expansion.

However, the market growth is hampered by the strict regulatory criteria for the safety and health of the food texture market, and the complexity of regulations is a major barrier to growth in the food texture industry. Due to the wide variety of food additive rules and standards, it can be difficult for manufacturers to compete in global markets. There is a high cost associated with testing and complying with these rules. Changes in supply and demand have altered market dynamics due to shifts in consumer behaviour, restrictions on the food service industry, and international lockdowns. With fewer restaurants and cafes, there was less need for convenience and speciality foods. In turn, this affected demand for items and materials designed to enhance surface texture in the locations.

The food texture market segmentation is based on type, form, and application. Based on type, the market is segmented into cellulose derivatives, gums, pectin, gelatin, starch, inulin, and dextrin. As per the form, the market is segmented into dry and liquid. The application segment is segmented into bakery & confectionery products and dairy & frozen foods.

The liquid food texture market is expected to hold a significant global market share in 2024. liquid or beverage-based items that offer convenience and functionality. Changes to these liquid products' mouthfeel, viscosity, and overall sensory appeal are typically necessary. The increased interest in dairy and meat substitutes has also stimulated new developments in the liquid food texture industry.

Dairy & frozen foods is used in large amount due to the loss of vitamins and minerals from fresh meals over time. Frozen alternatives may be more nutrient-dense than their fresh counterparts, especially in countries like the US, Germany, the UK, China, and India.

The Asia Pacific food texture market is expected to register the maximum market share in revenue in the near future. It can be attributed to the fact that more and more creative methods of feeding the public have emerged, and so has the demand for ingredients that lend texture to dishes. The rising demand for processed foods in the bakery, confectionary, convenience food, and dairy industries will affect the worldwide food texture industry. In addition, Europe is estimated to grow rapidly in the global food texture market because of consumer interest in packaged goods and the retail industry's response.

|

Report Attribute |

Specifications |

|

Market Size Value In 2023 |

USD 14.16 Bn |

|

Revenue Forecast In 2031 |

USD 22.67 Bn |

|

Growth Rate CAGR |

CAGR of 6.25 % from 2024 to 2031 |

|

Quantitative Units |

Representation of revenue in US$ Million and CAGR from 2024 to 2031 |

|

Historic Year |

2019 to 2023 |

|

Forecast Year |

2024-2031 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Type, Form, Application |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South East Asia; South Korea |

|

Competitive Landscape |

Ajinomoto Co Inc. (Japan), ADM (US), Ashland (US), IFF (US), Cargill (US), Tate & Lyle (UK), Avebe (Netherlands), CP Kelco (US), Kerry Group plc (Ireland), DSM (Netherlands), Ingredion (US), Estelle Chemicals Pvt. Ltd (India), Fiberstar, Inc. (US), Riken Vitamin Co., Ltd. (Japan), and Levapan S.A. (Colombia), Nexira, Palsgaard, Puratos, Naturex, Roquette Frères, Bhansali International, B & V Srl, Altrafine Gums, Agarmex, Agar Del Pacifico S.A. and Others |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Food Texture Market Snapshot

Chapter 4. Global Food Texture Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Form Analysis – Porter’s Five Forces Analysis

4.7. Competitive Landscape & Market Share Analysis

4.8. Impact of Covid-19 Analysis

Chapter 5. Market Segmentation 1: By Type Estimates & Trend Analysis

5.1. By Type, & Market Share, 2019 & 2031

5.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following By Type:

5.2.1. Cellulose Derivatives

5.2.2. Gums

5.2.3. Pectin

5.2.4. Gelatin

5.2.5. Starch

5.2.6. Inulin

5.2.7. Dextrin

5.2.8. Other Types

Chapter 6. Market Segmentation 2: By Source Estimates & Trend Analysis

6.1. By Source & Market Share, 2019 & 2031

6.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following By Source:

6.2.1. Natural

6.2.2. Synthetic

Chapter 7. Market Segmentation 3: By Form Estimates & Trend Analysis

7.1. By Form & Market Share, 2019 & 2031

7.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following By Form:

7.2.1. Dry

7.2.2. Liquid

Chapter 8. Market Segmentation 4: By Application Estimates & Trend Analysis

8.1. By Application & Market Share, 2019 & 2031

8.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following By Application:

8.2.1. Bakery & Confectionery Products

8.2.2. Dairy & Frozen Foods

8.2.3. Meat & Poultry Products

8.2.4. Beverages

8.2.5. Snacks & Savory

8.2.6. Sauces & Dressings

8.2.7. Other Applications

Chapter 9. Market Segmentation 5: By Functionality Estimates & Trend Analysis

9.1. By Functionality & Market Share, 2019 & 2031

9.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following By Functionality:

9.2.1. Thickening

9.2.2. Gelling

9.2.3. Emulsifying

9.2.4. Stabilizing

9.2.5. Other Functionalities

Chapter 10. Food Texture Market Segmentation 6: Regional Estimates & Trend Analysis

10.1. North America

10.1.1. North America Food Texture Market revenue (US$ Million) estimates and forecasts By Type, 2024-2031

10.1.2. North America Food Texture Market revenue (US$ Million) estimates and forecasts By Source, 2024-2031

10.1.3. North America Food Texture Market revenue (US$ Million) estimates and forecasts By Form, 2024-2031

10.1.4. North America Food Texture Market revenue (US$ Million) estimates and forecasts By Application, 2024-2031

10.1.5. North America Food Texture Market revenue (US$ Million) estimates and forecasts By Functionality, 2024-2031

10.1.6. North America Food Texture Market revenue (US$ Million) estimates and forecasts by country, 2024-2031

10.2. Europe

10.2.1. Europe Food Texture Market revenue (US$ Million) By Type, 2024-2031

10.2.2. Europe Food Texture Market revenue (US$ Million) By Source, 2024-2031

10.2.3. Europe Food Texture Market revenue (US$ Million) By Form, 2024-2031

10.2.4. Europe Food Texture Market revenue (US$ Million) By Application, 2024-2031

10.2.5. Europe Food Texture Market revenue (US$ Million) By Functionality, 2024-2031

10.2.6. Europe Food Texture Market revenue (US$ Million) by country, 2024-2031

10.3. Asia Pacific

10.3.1. Asia Pacific Food Texture Market revenue (US$ Million) By Type, 2024-2031

10.3.2. Asia Pacific Food Texture Market revenue (US$ Million) By Source, 2024-2031

10.3.3. Asia Pacific Food Texture Market revenue (US$ Million) By Form, 2024-2031

10.3.4. Asia Pacific Food Texture Market revenue (US$ Million) By Application, 2024-2031

10.3.5. Asia Pacific Food Texture Market revenue (US$ Million) By Functionality, 2024-2031

10.3.6. Asia Pacific Food Texture Market revenue (US$ Million) by country, 2024-2031

10.4. Latin America

10.4.1. Latin America Food Texture Market revenue (US$ Million) By Type, (US$ Million) 2024-2031

10.4.2. Latin America Food Texture Market revenue (US$ Million) By Source, (US$ Million) 2024-2031

10.4.3. Latin America Food Texture Market revenue (US$ Million) By Form, (US$ Million) 2024-2031

10.4.4. Latin America Food Texture Market revenue (US$ Million) By Application, (US$ Million) 2024-2031

10.4.5. Latin America Food Texture Market revenue (US$ Million) By Functionality, (US$ Million) 2024-2031

10.4.6. Latin America Food Texture Market revenue (US$ Million) by country, 2024-2031

10.5. Middle East & Africa

10.5.1. Middle East & Africa Food Texture Market revenue (US$ Million) By Type, (US$ Million) 2024-2031

10.5.2. Middle East & Africa Food Texture Market revenue (US$ Million) By Source, (US$ Million) 2024-2031

10.5.3. Middle East & Africa Food Texture Market revenue (US$ Million) By Form, (US$ Million) 2024-2031

10.5.4. Middle East & Africa Food Texture Market revenue (US$ Million) By Application, (US$ Million) 2024-2031

10.5.5. Middle East & Africa Food Texture Market revenue (US$ Million) By Functionality, (US$ Million) 2024-2031

10.5.6. Middle East & Africa Food Texture Market revenue (US$ Million) by country, 2024-2031

Chapter 11. Competitive Landscape

11.1. Major Mergers and Acquisitions/Strategic Alliances

11.2. Company Profiles

11.2.1. Ajinomoto Co. Inc. (Japan)

11.2.2. ADM (US)

11.2.3. Ashland (US)

11.2.4. IFF (US)

11.2.5. Cargill (US)

11.2.6. Avebe (Netherlands)

11.2.7. CP kelco (US)

11.2.8. kerry group (Ireland)

11.2.9. DSM (Netherlands)

11.2.10. Ingredion (US)

11.2.11. Estelle Chemicals Pvt. Ltd. (India)

11.2.12. Fiberstar Inc. (US)

11.2.13. Tate & Lyle (UK)

11.2.14. Riken Vitamin Co Ltd. (Japan)

11.2.15. Nexira (France)

11.2.16. Palsgaard (Denmark)

11.2.17. Puratos (Belgium)

11.2.18. Naturex (Colombia)

11.2.19. Roquette Frères (France)

11.2.20. Bhansali international (India)

11.2.21. B & V SRL (Italy)

11.2.22. Altrafine Gums (India)

11.2.23. Agarmex (Mexico)

11.2.24. Agar del Pacifico S.A. (Chile)

Food Texture Market By Type-

Food Texture Market By Form-

Food Texture Market By Source-

Food Texture Market By Application-

Food Texture Market By Functionality-

Food Texture Market By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

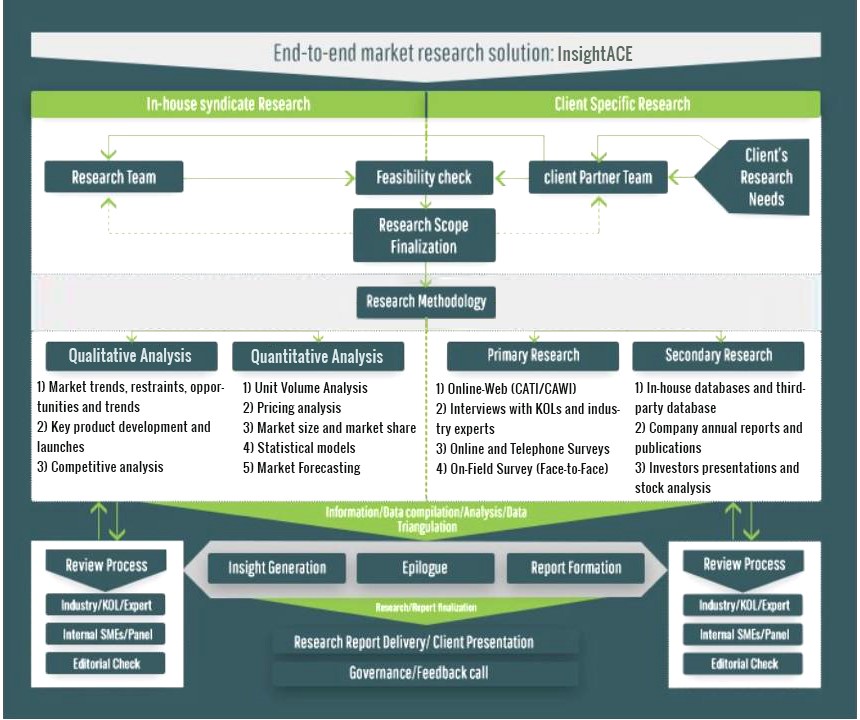

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.