Deep Venous Disease Treatment Devices Market Size, Share & Trends Analysis Report By Products (Thrombectomy and Thrombolysis Devices, Inferior Vena Cava (IVC) Filters, Peripheral Vascular Stents, PTA Balloon Catheters, Accessory Devices, and Compression Devices/Stockings) and End-user And Segment Forecasts, 2024-2031

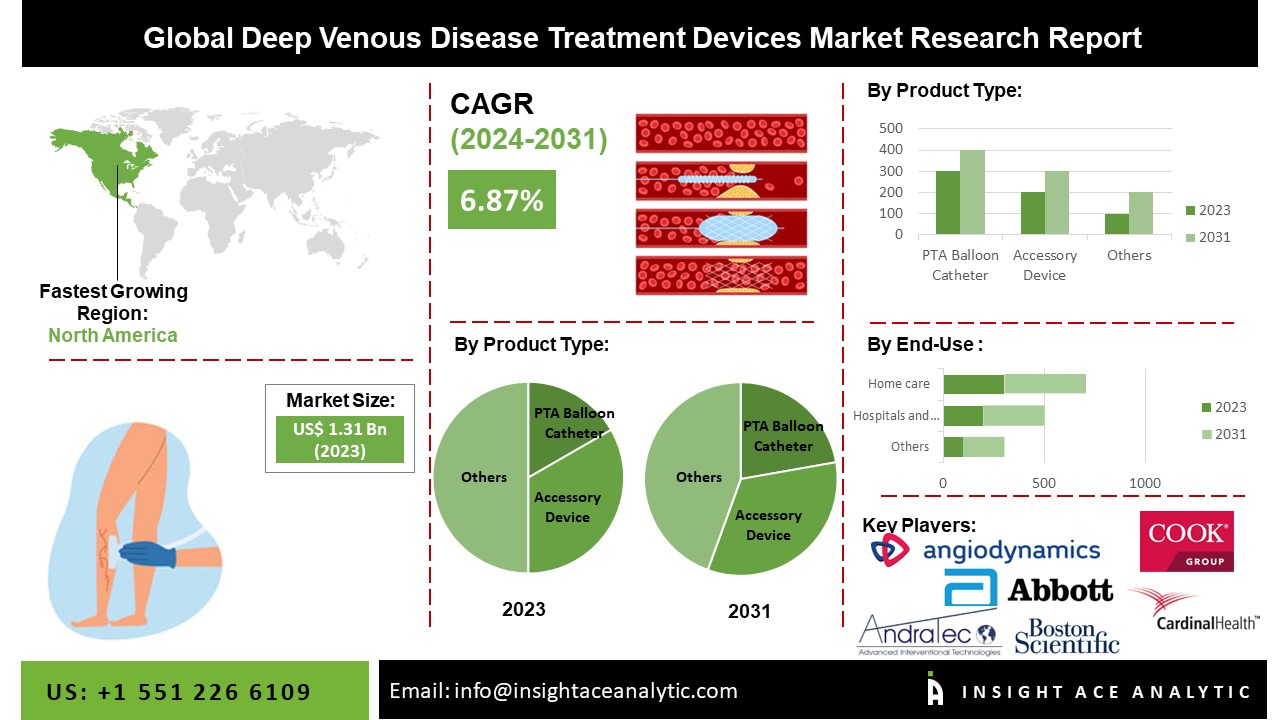

The Global Deep Venous Disease Treatment Devices Market Size is valued at 1.31 billion in 2023 and is predicted to reach 2.22 billion by the year 2031 at a 6.87% CAGR during the forecast period for 2024-2031.

Key Industry Insights & Findings from the Report:

- The rising prevalence of deep vein diseases acts as a primary driver for the demand for treatment devices. Factors such as lifestyle changes, an ageing population, and predisposing factors like obesity contribute to the rising incidence of these conditions, increasing the need for effective medical interventions and driving the market for treatment devices.

- Continuous advancements in vascular stent technologies are a significant driver of deep venous disease treatment device market growth.

- North America dominated the market and accounted for a global revenue share in 2023.

- Device for the Treatment of Deep Venous Disease The market encounters obstacles such as fierce rivalry, swiftly advancing technology, and the necessity to adjust to shifting market demands.

Vein-related illnesses are conditions that damage the body's veins. One of the most prevalent disorders brought on by harmed vessel walls and valves is varicose veins. According to an article in the Journal of the American Heart Association, around 23% of adults in the United States have varicose veins. Venous reflux disease is treated using a variety of techniques, including ablation, sclerotherapy injection, ligation or stripping, and supportive care.

The market is driven by elements such as the rise in deep vein disease incidence, which increases the demand for treatment devices. The rise in deep venous disease diagnoses in hospitals, which increases the need for preventative devices, and the rise in deep venous disease awareness drives the development of deep venous disease devices in the market.

However, producers and consumers have suffered due to the pandemic. The number of treatments substantially decreased since varicose vein surgeries are not urgent. A decrease also influenced the revenue streams of the manufacturers in varicose vein surgeries or procedures due to limitations on travel. Manufacturers are taking several strategic actions to recover from COVID-19. To enhance the technology and test findings associated with the pet food flavors and ingredients market, the players are engaging in several R&D activities, product launches, and strategic collaborations.

Competitive Landscape:

Some of the Deep Venous Disease Treatment Devices market players are:

- Abbott Laboratories

- AndraTec GmbH

- AngioDynamics, Inc.

- Boston Scientific Corporation

- Cardinal Health

- Cook Group

- Innova Vascular, Inc.

- Koninklijke Philips N.V.

- Medtronic plc

- Nipro Corporation

- Penumbra, Inc.

- Stryker Corporation

- Surmodics, Inc. (Vetex Medical Ltd.)

- Teleflex Incorporated

- Terumo Corporation

Market Segmentation:

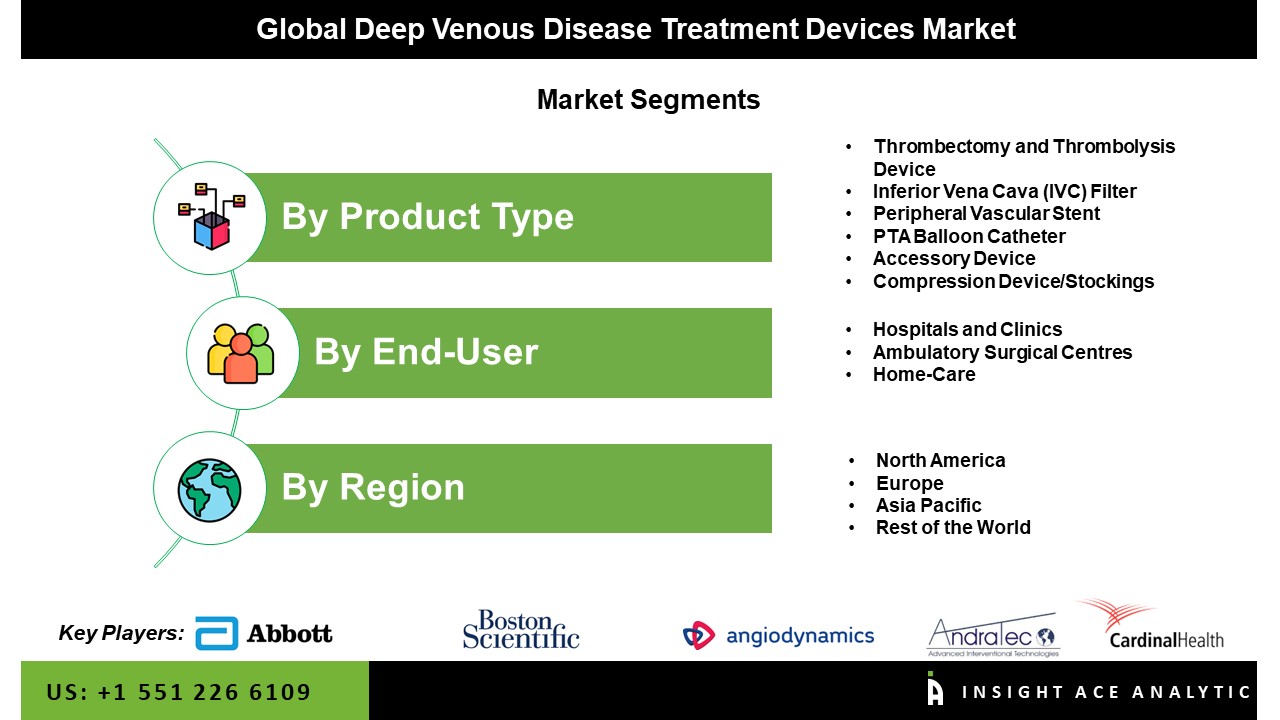

The Deep Venous, Disease Treatment Devices market, is segmented based on products and End-user. Product segment includes Thrombectomy and Thrombolysis Devices, Inferior Vena Cava (IVC) Filters, Peripheral Vascular Stents, PTA Balloon Catheters, Accessory Devices, and Compression Devices/Stockings. By End-User, the market is segmented into Hospitals and Clinics, Ambulatory Surgical Centers, and Homecare.

Based On Product, The Accessory Segment Is Accounted As A Major Contributor In The Deep Venous Disease Treatment Devices Market

During the projected period, the growing elderly population and the rising prevalence of cardiovascular disorders are anticipated to be the key drivers of the accessory device segment's growth. Cardiovascular illnesses are more prone to strike the elderly population. Over 20.8% of the European population was 65 years or older, according to Ageing Europe Statistics, 2021. Between 2021 and 2100, it is predicted that the proportion of Europeans 80 years of age or older will rise from 6.0% to 14.6%, a two-and-a-half-fold increase. Additionally, the growing desire for minimally invasive procedures will probably fuel market expansion. For instance, a minimally invasive procedure called cardiac catheterization uses thin, elastic tubes called catheters to direct them via blood vessels to the problematic areas to identify and treat several heart and vascular disorders, including May-Thurner syndrome.

Hospital And Clinic Segment Witness Growth At A Rapid Rate

Due to a growth in hospitals and surgery centers, which was the largest contributor depending on end-user in 2023, is anticipated to keep up its dominance during the projected period. However, because ambulatory surgery centers are more affordable than traditional hospitals, this market segment is predicted to develop significantly during the forecast period.

In The Region, The North America Deep Venous Disease Treatment Devices Market Holds A Significant Revenue Share

North America held a share of revenue of approximately 45.0%, dominating the market in 2023. This is mostly caused by a sizable patient population that values appearance. Due to the obvious results and safety, many are eager to undergo cosmetic operations. The proof of the safety and effectiveness of laser therapy has contributed to lowering the stigma associated with cosmetic procedures and fostering societal acceptance of laser treatments, particularly among males. The region with the quickest growth is anticipated to be Asia Pacific. Due to its huge aging population, growing disposable money, and growing knowledge of these procedures, the Asia Pacific region is anticipated to have significant growth in the years to come. Because of the various legislative considerations that affect product availability between nations, the market is extremely diversified.

Recent Developments:

- In January 2024, Penumbra, Inc., a thrombectomy company, obtained CE Mark for its Indigo System CAT RX, designed to overcome limitations of traditional strategies in acute coronary syndrome treatment. Unlike syringe aspiration, which loses vacuum when fluid enters the system, CAT RX, now available in Europe, navigates tortuous coronary anatomy while sustaining mechanical aspiration with the Penumbra ENGINE.

- In April 2023, Abbott purchased Cardiovascular Systems, Inc. (CSI), a medical devices company that possessed cutting-edge solutions for addressing intricate artery problems, which affected a significant number of individuals. CSI's primary emphasis was on developing systems that targeted the treatment of coronary and peripheral artery disease, conditions that impacted approximately 20 million and 8 million individuals in the United States, respectively.

Deep Venous Disease Treatment Devices Market Report Scope:

| Report Attribute | Specifications |

| Market size value in 2023 | USD 1.31 Bn |

| Revenue forecast in 2031 | USD 2.22Bn |

| Growth rate CAGR | CAGR of 6.87% from 2024 to 2031 |

| Quantitative units | Representation of revenue in US$ Billion and CAGR from 2024 to 2031 |

| Historic Year | 2019 to 2023 |

| Forecast Year | 2024-2031 |

| Report coverage | The forecast of revenue, the position of the company, the competitive market statistics, growth prospects, and trends |

| Segments covered | Products, End-user |

| Regional scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia; South Korea; Southeast Asia |

| Competitive Landscape | Abbott Laboratories, AndraTec GmbH, AngioDynamics, Inc., Boston Scientific Corporation, Cardinal Health, Cook Group, Innova Vascular, Inc., Koninklijke Philips N.V., Medtronic plc, Nipro Corporation, Penumbra, Inc., Stryker Corporation, Surmodics, Inc. (Vetex Medical Ltd.), Teleflex Incorporated, and Terumo Corporation. |

| Customization scope | Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

| Pricing and available payment methods | Explore pricing alternatives that are customized to your particular study requirements. |

Segmentation of Deep Venous Disease Treatment Devices Market-

Deep Venous Disease Treatment Devices Market By Product-

- Thrombectomy and Thrombolysis Device

- Inferior Vena Cava (IVC) Filter

- Peripheral Vascular Stent

- PTA Balloon Catheter

- Accessory Device

- Compression Device/Stockings

Deep Venous Disease Treatment Devices Market By End User-

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Homecare

Deep Venous Disease Treatment Devices Market By Region-

North America-

- The US

- Canada

- Mexico

Europe-

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

Asia-Pacific-

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

Latin America-

- Brazil

- Argentina

- Rest of Latin America

Middle East & Africa-

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Research Design and Approach

This study employed a multi-step, mixed-method research approach that integrates:

- Secondary research

- Primary research

- Data triangulation

- Hybrid top-down and bottom-up modelling

- Forecasting and scenario analysis

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary Research

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Sources Consulted

Secondary data for the market study was gathered from multiple credible sources, including:

- Government databases, regulatory bodies, and public institutions

- International organizations (WHO, OECD, IMF, World Bank, etc.)

- Commercial and paid databases

- Industry associations, trade publications, and technical journals

- Company annual reports, investor presentations, press releases, and SEC filings

- Academic research papers, patents, and scientific literature

- Previous market research publications and syndicated reports

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

Primary Research

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Stakeholders Interviewed

Primary interviews for this study involved:

- Manufacturers and suppliers in the market value chain

- Distributors, channel partners, and integrators

- End-users / customers (e.g., hospitals, labs, enterprises, consumers, etc., depending on the market)

- Industry experts, technology specialists, consultants, and regulatory professionals

- Senior executives (CEOs, CTOs, VPs, Directors) and product managers

Interview Process

Interviews were conducted via:

- Structured and semi-structured questionnaires

- Telephonic and video interactions

- Email correspondences

- Expert consultation sessions

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

Data Processing, Normalization, and Validation

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

- Standardization of units (currency conversions, volume units, inflation adjustments)

- Cross-verification of data points across multiple secondary sources

- Normalization of inconsistent datasets

- Identification and resolution of data gaps

- Outlier detection and removal through algorithmic and manual checks

- Plausibility and coherence checks across segments and geographies

This ensured that the dataset used for modelling was clean, robust, and reliable.

Market Size Estimation and Data Triangulation

Bottom-Up Approach

The bottom-up approach involved aggregating segment-level data, such as:

- Company revenues

- Product-level sales

- Installed base/usage volumes

- Adoption and penetration rates

- Pricing analysis

This method was primarily used when detailed micro-level market data were available.

Top-Down Approach

The top-down approach used macro-level indicators:

- Parent market benchmarks

- Global/regional industry trends

- Economic indicators (GDP, demographics, spending patterns)

- Penetration and usage ratios

This approach was used for segments where granular data were limited or inconsistent.

Hybrid Triangulation Approach

To ensure accuracy, a triangulated hybrid model was used. This included:

- Reconciling top-down and bottom-up estimates

- Cross-checking revenues, volumes, and pricing assumptions

- Incorporating expert insights to validate segment splits and adoption rates

This multi-angle validation yielded the final market size.

Forecasting Framework and Scenario Modelling

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Forecasting Methods

- Time-series modelling

- S-curve and diffusion models (for emerging technologies)

- Driver-based forecasting (GDP, disposable income, adoption rates, regulatory changes)

- Price elasticity models

- Market maturity and lifecycle-based projections

Scenario Analysis

Given inherent uncertainties, three scenarios were constructed:

- Base-Case Scenario: Expected trajectory under current conditions

- Optimistic Scenario: High adoption, favourable regulation, strong economic tailwinds

- Conservative Scenario: Slow adoption, regulatory delays, economic constraints

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.

Request Customization

Add countries, segments, company profiles, or extend forecast — free 10% customization with purchase.

Customize This Report →Enquire Before Buying

Speak with our analyst team about scope, methodology, pricing, or deliverable formats.

Enquire Now →Frequently Asked Questions

Deep Venous Disease Treatment Devices Market Size is valued at 1.31 billion in 2023 and is predicted to reach 2.22 billion by the year 2031

Deep Venous Disease Treatment Devices Market expected to grow at a 6.87% CAGR during the forecast period for 2024-2031

Abbott Laboratories, AndraTec GmbH, AngioDynamics, Inc., Boston Scientific Corporation, Cardinal Health, Cook Group, Innova Vascular, Inc., Koninklijk