Global Digital Agriculture Market Size is valued at USD 21.9 Bn in 2024 and is predicted to reach USD 64.5 Bn by the year 2034 at a 11.6% CAGR during the forecast period for 2025-2034.

Digital agriculture refers to plans created to enhance and control the management of agricultural operations and production tasks. Automation of record keeping, data storage, monitoring, and production processes are only a few of the many uses for this software on farms. Utilizing data-driven insights, digital farming software optimizes agricultural output and revenue, among other indicators. Individuals involved in farming and the agricultural value chain can all enhance food production through digital agriculture, which consists of utilizing new and advanced technology integrated into a unified system. As a result of the digital platform's assistance, farmers and ranchers can better link up with resources, including capital, marketing, sales, and machinery.

The agricultural sector could be entirely transformed by forming a global digital agriculture market. By using digital technology in agriculture, suppliers can increase their chances of reaching a worldwide audience, and countries can better accommodate the increasing need for food. Furthermore, the growing interest in digital agriculture and its potential to improve crop yield optimization aided in the growth of the farming industry.

However, the market growth is hampered by the high-cost criteria for the safety and health of the digital agriculture market and the product's inability to prevent fog in environments with dramatic temperature fluctuations or high digital agriculture. Due to the high maintenance costs of modern vehicles, small farmers need to use smart digital farming solutions widely. The ongoing costs of these cars' sensors, software, hardware, and cameras threaten their market growth.

For small-scale farmers, the high cost of devices and software systems is a major obstacle to adoption in the digital agriculture market. There was a significant impact on the agricultural sector from the COVID-19 epidemic because of the travel restrictions, nationwide lockdowns, and suspension of import and export activity caused by the limited mobility of migrants and rural laborers. The global agricultural sector was hit hard by the severe scarcity of workers caused by this circumstance. The outbreak also caused a drop in agricultural equipment sales because of the unfavourable economic climate and limited shipments.

The digital agriculture market is categorized based on offering, technology, operation, and type. Offering segment includes advisory services, precision agriculture & farm management, quality management & traceability, digital procurement, Agri e-commerce, and financial services. By technology, the market is segmented into peripheral technology and core technology. The market is segmented by operation into farming & feeding, monitoring & scouting, and marketing & demand generation. The market is segmented by type into hardware, software, and services.

The precision agriculture & farm management digital agriculture market is expected to hold a major global market share in 2022. With precision agriculture and efficient farm management, farmers can decrease the quantity of inputs they utilize, effectively lowering the likelihood of environmental damage. Precision agriculture allows farmers to keep a closer eye on their crops and make better management decisions, which in turn helps keep soil healthy and decreases the likelihood of pests and diseases.

The hardware industry makes up the bulk of acrylic acid ester usage because the subcategories include access points, sensing devices, antennas, and automation and control systems. Farming is greatly enhanced by using hardware components, including sensing devices, drones, and automation and control systems, especially in countries like the US, Germany, the UK, China, and India.

The North American digital agriculture market is expected to deliver the highest market share in revenue shortly. It can be attributed to the government's actively encouraging modern agricultural technologies and constructed infrastructure. In addition, Asia Pacific is projected to expand in the global digital agriculture market because the governments of developing nations have taken various steps to promote the use of contemporary agricultural techniques.

|

Report Attribute |

Specifications |

|

Market size value in 2024 |

USD 21.9 Bn |

|

Revenue forecast in 2034 |

USD 64.5 Bn |

|

Growth Rate CAGR |

CAGR of 11.6% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn,and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Offering, Technology, Operation, And Type |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; Southeast Asia; South Korea |

|

Competitive Landscape |

Cisco Systems, Inc. (US), IBM Corporation (US), Accenture (Ireland), Trimble Inc. (US), Deere & Company (US), Epicor Software Corporation (US), Hexagon AB (Sweden), Bayer AG (Germany), AGCO Corporation (US), and Vodafone Group PLC (UK). |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Digital Agriculture Market Snapshot

Chapter 4. Global Digital Agriculture Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Industry Analysis – Porter’s Five Forces Analysis

4.7. Competitive Landscape & Market Share Analysis

4.8. Impact of Covid-19 Analysis

Chapter 5. Market Segmentation 1: by Type Estimates & Trend Analysis

5.1. by Type & Market Share, 2024 & 2034

5.2. Market Size (Value (US$ Mn)) & Forecasts and Trend Analyses, 2021 to 2034 for the following by Type:

5.2.1. Hardware

5.2.1.1. Automation & Control Systems

5.2.1.1.1. Drones/UAVs

5.2.1.1.2. Irrigation Controllers

5.2.1.1.3. GPS/GNSS

5.2.1.1.4. Flow & Application Control Devices

5.2.1.1.5. Guidance & Steering

5.2.1.1.6. Handheld Mobile Device/Handheld Computers

5.2.1.1.7. Displays

5.2.1.1.8. Harvesters & Forwarders

5.2.1.1.9. Variable Rate Controllers

5.2.1.1.10. Control Systems

5.2.1.1.11. Robotic Hardware

5.2.1.1.12. HVAC Systems

5.2.1.1.13. LED Grow Lights

5.2.1.1.14. Other Automation & Control Systems

5.2.1.2. Sensing & Monitoring Devices

5.2.1.2.1. Yield Monitors

5.2.1.2.2. Soil Sensors

5.2.1.2.3. Water Sensors

5.2.1.2.4. Climate Sensors

5.2.1.2.5. Camera Systems

5.2.1.2.6. RFID & Sensors for Precision Forestry

5.2.1.2.7. Temperature & Environment Monitoring Sensors

5.2.1.2.8. pH & Dissolved Oxygen Sensors

5.2.1.2.9. EC Sensors

5.2.1.2.10. RFID Tags & Readers for Livestock Monitoring

5.2.1.2.11. Sensors for Livestock Monitoring

5.2.1.2.12. Sensors for Smart Greenhouse

5.2.1.2.13. Other Sensing & Monitoring Devices

5.2.2. Software

5.2.2.1. On-cloud

5.2.2.2. On-premises

5.2.2.3. AI & Data Analytics

5.2.3. Services

5.2.3.1. System Integration & Consulting

5.2.3.2. Data Collection & Analytical Services

5.2.3.3. Connectivity Services

5.2.3.4. Assistant Professional Services

5.2.3.5. Maintenance & Support Services

Chapter 6. Market Segmentation 2: by Offering Estimates & Trend Analysis

6.1. by Offering & Market Share, 2024 & 2034

6.2. Market Size (Value (US$ Mn)) & Forecasts and Trend Analyses, 2021 to 2034 for the following by Offering:

6.2.1. Advisory Services

6.2.2. Precision Agriculture & Farm Management

6.2.3. Quality Management & Traceability

6.2.4. Digital Procurement

6.2.5. Agri e-Commerce

6.2.6. Financial Services

Chapter 7. Market Segmentation 3: by Operation Estimates & Trend Analysis

7.1. by Operation & Market Share, 2024 & 2034

7.2. Market Size (Value (US$ Mn)) & Forecasts and Trend Analyses, 2021 to 2034 for the following by Operation:

7.2.1. Farming & Feeding

7.2.1.1. Precision Agriculture

7.2.1.2. Precision Animal Rearing & Feeding

7.2.1.3. Precision Aquaculture

7.2.1.4. Precision Forestry

7.2.1.5. Smart Greenhouse

7.2.2. Monitoring & Scouting

7.2.3. Marketing & Demand Generation

Chapter 8. Market Segmentation 4: by Technology Estimates & Trend Analysis

8.1. by Technology & Market Share, 2024 & 2034

8.2. Market Size (Value (US$ Mn)) & Forecasts and Trend Analyses, 2021 to 2034 for the following by Technology:

8.2.1. Peripheral Technology

8.2.1.1. Platforms

8.2.1.2. Apps

8.2.2. Core Technology

8.2.2.1. Automation

8.2.2.2. Drones

8.2.2.3. Robotics

8.2.2.4. AI/ML

Chapter 9. Digital Agriculture Market Segmentation 5: Regional Estimates & Trend Analysis

9.1. North America

9.1.1. North America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

9.1.2. North America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Offering, 2021-2034

9.1.3. North America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Operation, 2021-2034

9.1.4. North America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Technology, 2021-2034

9.1.5. North America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

9.2. Europe

9.2.1. Europe Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

9.2.2. Europe Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Offering, 2021-2034

9.2.3. Europe Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Operation, 2021-2034

9.2.4. Europe Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Technology, 2021-2034

9.2.5. Europe Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

9.3. Asia Pacific

9.3.1. Asia Pacific Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

9.3.2. Asia Pacific Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Offering, 2021-2034

9.3.3. Asia-Pacific Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Operation, 2021-2034

9.3.4. Asia Pacific Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Technology, 2021-2034

9.3.5. Asia Pacific Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

9.4. Latin America

9.4.1. Latin America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

9.4.2. Latin America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Offering, 2021-2034

9.4.3. Latin America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Operation, 2021-2034

9.4.4. Latin America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Technology, 2021-2034

9.4.5. Latin America Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

9.5. Middle East & Africa

9.5.1. Middle East & Africa Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

9.5.2. Middle East & Africa Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Offering, 2021-2034

9.5.3. Middle East & Africa Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Operation, 2021-2034

9.5.4. Middle East & Africa Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by Technology, 2021-2034

9.5.5. Middle East & Africa Digital Agriculture Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

Chapter 10. Competitive Landscape

10.1. Major Mergers and Acquisitions/Strategic Alliances

10.2. Company Profiles

10.2.1. Cisco Systems, Inc. (US)

10.2.2. IBM Corporation (US)

10.2.3. Accenture (Ireland)

10.2.4. Trimble Inc. (US)

10.2.5. Deere & Company (US)

10.2.6. Epicor Software Corporation (US)

10.2.7. Hexagon AB (Sweden)

10.2.8. Bayer AG (Germany)

10.2.9. AGCO Corporation (US)

10.2.10. Vodafone Group PLC (UK)

10.2.11. Other Prominent Players

Digital Agriculture Market By Offering-

Digital Agriculture Market By Technology-

Digital Agriculture Market By Operation-

Digital Agriculture Market By Type-

By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

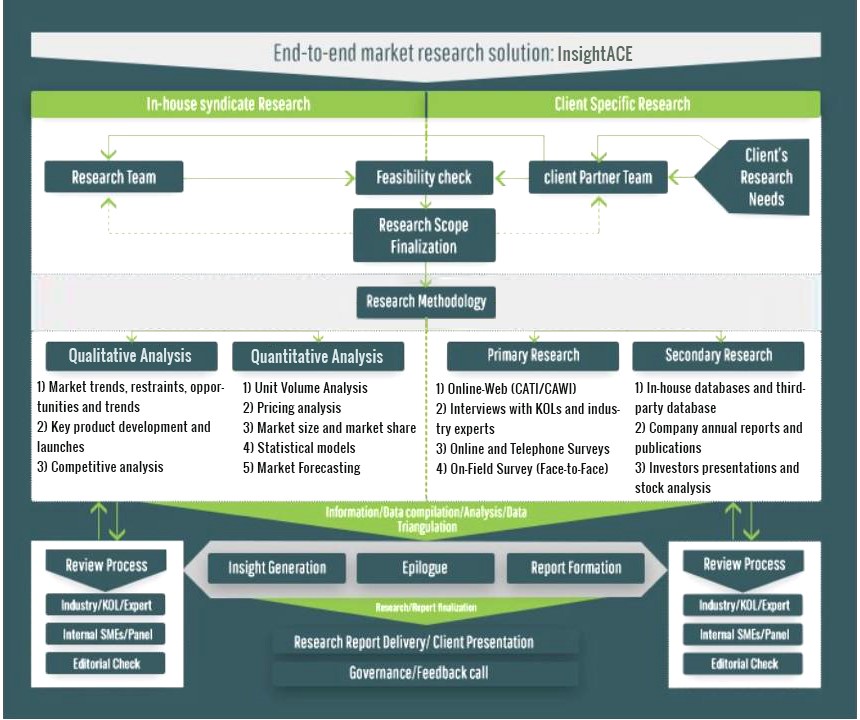

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.