The Artificial Intelligence in Epidemiology Market Size is valued at 475.63 Million in 2024 and is predicted to reach 5271.80 Million by the year 2034 at an 27.4% CAGR during the forecast period for 2025-2034.

Key Industry Insights & Findings from the Report:

Artificial intelligence (AI) is an intelligent system that performs various human intelligence-based operations in domains such as biology, computer science, mathematics, linguistics, psychology, and engineering. These talents include reasoning, learning, and problem-solving. In the healthcare industry, artificial intelligence is used to analyze complex medical data using algorithms and software. Rising public awareness of the significance of technology in chronic disease diagnosis and monitoring will be a significant driving force in the progress of AI applications in epidemiology. As healthcare research and development efforts expand, so will the demand for artificial intelligence in epidemiology labs.

The extensive usage and use of AI in drug research and discovery activities is a critical motivator. Pharmaceutical and biotech companies have also increased their R&D investments. This investment interest is driving the adoption of AI systems to follow the progression of syndromic diseases. The growing burden of chronic diseases has increased the need for effective control measures and the development of feasible treatment solutions. Government-backed programs, more significant investment from private investors and venture capitalists, and the creation of AI-focused start-ups worldwide are driving market expansion. Despite the prevalence of the diseases, the high cost of these techniques may impede the growth of the worldwide AI-based critical care market.

Artificial intelligence in the epidemiology market is segmented on the deployment, applications and end users. Based on deployment, the market is segmented into web-based and cloud-based. Based on application, artificial intelligence in the epidemiology market is segmented into infection prediction & forecasting and disease & syndromic surveillance. Based on the end user, artificial intelligence in the epidemiology market is segmented into government & state agencies, research labs, pharmaceutical & biotechnology companies, and healthcare providers.

The market's leading segment is healthcare providers. As a result of recent increases in awareness and correction of some common misconceptions about the intake of certain veggies, consumer acceptance and widespread application for equestrian and cow feeding are expected to drive demand for GMO veggies, strengthening segmental development.

Web-based grabbed the highest revenue share, and it is anticipated that they will continue to hold that position during the expected time. Adopting web-based software in epidemiology provides various advantages, including the possibility of integrating with other interoperable platforms. Web-based resources are also being developed to give health information and aid decision-making quickly. Such advancements will accelerate the use of AI in web-based epidemiological data analysis.

The North American artificial intelligence in epidemiology market is expected to register the highest market share in revenue shortly. Because of developments in healthcare IT infrastructure, rising healthcare expenditures, widespread technology use, favourable government efforts, and the presence of numerous key market competitors, The region has seen an increase in the use of AI technologies by federal authorities. The presence of key technology players will also facilitate the efficient integration of AI in epidemiology. Countries such as the United States and Canada are home to big pharmaceutical and biotechnology corporations that invest heavily in research, indicating a promising future for North American AI solution suppliers. Besides, Asia-Pacific is predicted to increase due to significant breakthroughs and development in IT infrastructure and entrepreneurial initiatives specialized in AI-based technologies. Artificial intelligence (AI) is an intelligent system that performs various functions.

| Report Attribute | Specifications |

| Market size value in 2024 | USD 475.63 Million |

| Revenue forecast in 2034 | USD 5271.80 Million |

| Growth rate CAGR | CAGR of 27.4% from 2025 to 2034 |

| Quantitative units | Representation of revenue in US$ Million and CAGR from 2025 to 2034 |

| Historic Year | 2021 to 2024 |

| Forecast Year | 2025-2034 |

| Report coverage | The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

| Segments covered | Deployment, Application, End-Use |

| Regional scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope | U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico ;France; Italy; Spain; Japan; South Korea; South East Asia |

| Competitive Landscape | Cognizant Technology Solutions Corporation, Cerner Corporation (Oracle), Epic Systems Corporation, eClinicalWorks LLC, Alphabet Inc., Komodo Health, Microsoft Corporation, Meditech, Predixion Software, Siemens Healthineers AG, Intel Corporation, Bayer Healthcare, Artificial Intelligence for Medical Epidemiology (AIME), Cardiolyse, and SAS Institute, Inc |

| Customization scope | Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

| Pricing and available payment methods | Explore pricing alternatives that are customized to your particular study requirements. |

By Deployment

By Application

By End-use

By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

This study employed a multi-step, mixed-method research approach that integrates:

This approach ensures a balanced and validated understanding of both macro- and micro-level market factors influencing the market.

Secondary research for this study involved the collection, review, and analysis of publicly available and paid data sources to build the initial fact base, understand historical market behaviour, identify data gaps, and refine the hypotheses for primary research.

Secondary data for the market study was gathered from multiple credible sources, including:

These sources were used to compile historical data, market volumes/prices, industry trends, technological developments, and competitive insights.

Primary research was conducted to validate secondary data, understand real-time market dynamics, capture price points and adoption trends, and verify the assumptions used in the market modelling.

Primary interviews for this study involved:

Interviews were conducted via:

Primary insights were incorporated into demand modelling, pricing analysis, technology evaluation, and market share estimation.

All collected data were processed and normalized to ensure consistency and comparability across regions and time frames.

The data validation process included:

This ensured that the dataset used for modelling was clean, robust, and reliable.

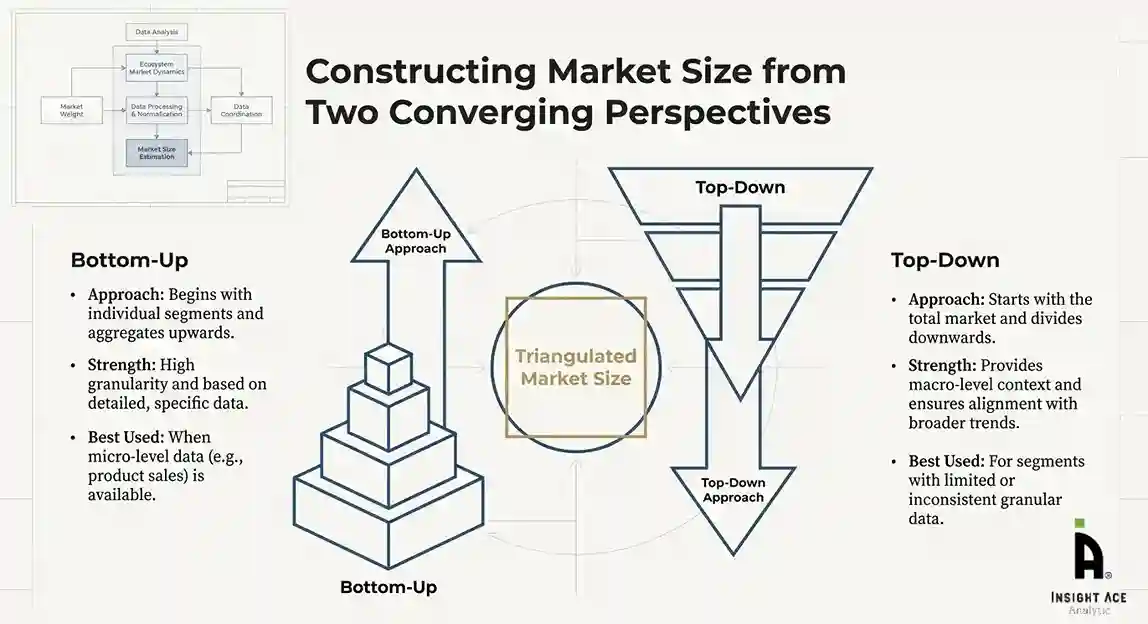

The bottom-up approach involved aggregating segment-level data, such as:

This method was primarily used when detailed micro-level market data were available.

The top-down approach used macro-level indicators:

This approach was used for segments where granular data were limited or inconsistent.

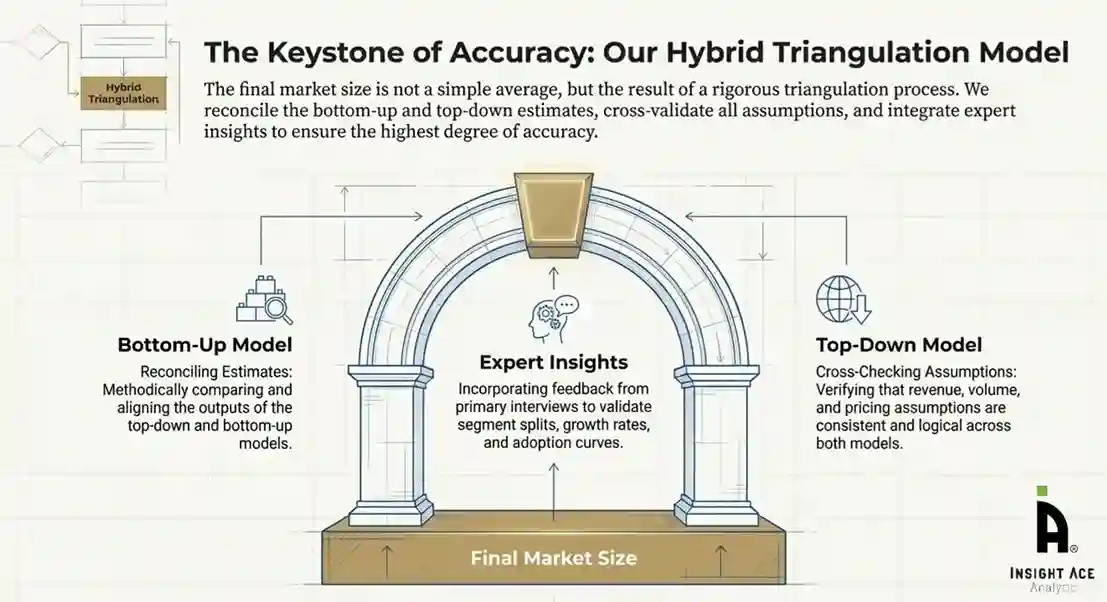

To ensure accuracy, a triangulated hybrid model was used. This included:

This multi-angle validation yielded the final market size.

Market forecasts were developed using a combination of time-series modelling, adoption curve analysis, and driver-based forecasting tools.

Given inherent uncertainties, three scenarios were constructed:

Sensitivity testing was conducted on key variables, including pricing, demand elasticity, and regional adoption.