_Market.JPG)

Global UAV Satellite Communication (SATCOM) Market Size is valued at USD 9.3 Billion in 2024 and is predicted to reach USD 11.0 Billion by the year 2034 at a 1.7% CAGR during the forecast period for 2025-2034.

Market")

The UAV Satellite Communication (SATCOM) industry is growing due to the increasing need for mobile satellite services and small satellites for earth observation services in the energy, oil & gas, defense, and agricultural sectors. The current communication infrastructure includes an artificial satellite in a network known as satellite communication (Satcom).

The market is anticipated to develop as a result of this. There are several different orbits in which satellites are placed, including geostationary, elliptical, Molniya, and low Earth orbits. Typical satellite communications (Satcom) uses include broadcasting TV and radio shows as well as traditional point-to-point communications and mobile apps. In order to improve communication infrastructure, satellite communication has been used by rural and underdeveloped communities globally.

Additionally, the spread of intelligent transportation systems (ITS) has been foreshadowed by the adoption of next-generation technologies like AI and IoT. Real-time vehicle tracking made possible by ITS allows users and goods operators to share and receive information quickly. Satcom in transportation allows uninterrupted and seamless data transmission among the vehicle and transport hub, effectively replacing the requirement for terrestrial networks. Therefore, using satellites in the transport and logistics network offers subsequent growth opportunities for the satellite communication market.

The UAV Satellite Communication (SATCOM) market is segmented on the basis of application, drone type, frequency band, and component. Application segment includes Marine Surveillance, Disaster Management, Surveying and Mapping, Industrial Inspection and Monitoring, Military ISR, Agriculture and Forestry, Civil Surveillance, and Cinematography. The drone-type segment includes fixed wing and rotary wing. Frequency band segment includes Ku Band, Ka Band, X Band, C Band, S Band, L Band, Q Band, and V Band. The component segment includes Antennae, Amplifier, Upconverter, Downconverter, Analog-to-Digital Converter, Digital-to-Analog Converter, Modulator, Demodulator, Encoder, Decoder, Scrambler, Descrambler, Multiplexer, Demultiplexer, User Interface, Wiring Solution, Power Unit, and Casing.

The segment is growing as a result of rising investments in the space industry and an increase in the number of launches of communication satellites. As more defense forces use next-generation gadgets for real-time information, the military apps and navigation industry will experience tremendous growth.

Satellite communications depend on transponders and antennas. By necessity, antennas mounted on satellites are utilized for both signal reception and signal transmission. The satellite's antennas pick up signals uplinked (broadcast) from numerous Earthly sources.

The majority of worldwide revenue came from North America, which controlled the market. This is explained by the military's and defense industry's rising need for constant contact, which led to the U.S. defense department's widespread deployment of satellite communication technology. Additionally, numerous satellite communication service providers, including Telesat, Viasat, Inc., and EchoStar Corporation, support market expansion. Additionally, over the next few years, it is anticipated that the regional market will grow significantly as a result of the upgrading of military communication infrastructure.

|

Report Attribute |

Specifications |

|

Market size value in 2024 |

USD 9.3 Billion |

|

Revenue forecast in 2034 |

USD 11.0 Billion |

|

Growth rate CAGR |

CAGR of 1.7% from 2025 to 2034 |

|

Quantitative units |

Representation of revenue in US$ Mn,, and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report coverage |

The forecast of revenue, the position of the company, the competitive market statistics, growth prospects, and trends |

|

Segments covered |

Application, Drone Type, Frequency Band, And Component |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia; South Korea; Southeast Asia |

|

Competitive Landscape |

Honeywell International Inc., Cobham Aerospace Communications, Thales Group, Get SAT Ltd., Viasat Inc, Harvest Technology Group Pty Limited., SKYTRAC Systems Ltd., Gilat Satellite Networks, Inmarsat Global Limited, CTECH, Indra, Cowave Communication Technology Co., Ltd, Orbit Communication Systems Ltd and Hughes Network Systems, LLC. |

|

Customization scope |

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing and available payment methods |

Explore pricing alternatives that are customized to your particular study requirements. |

UAV Satellite Communication (SATCOM) Market By Application-

UAV Satellite Communication (SATCOM) Market By Drone Type-

UAV Satellite Communication (SATCOM) Market By Frequency Band-

UAV Satellite Communication (SATCOM) Market By Component-

UAV Satellite Communication (SATCOM) Market By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

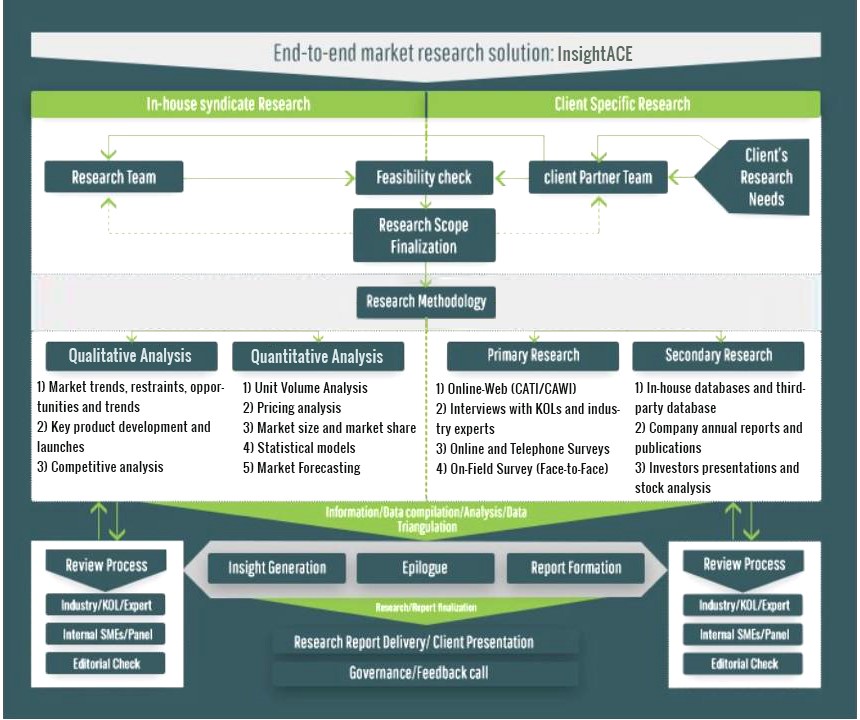

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.