Smart Agriculture Edge Computing Devices Market Size is valued at US$ 2.9 Bn in 2024 and is predicted to reach US$ 16.7 Bn by the year 2034 at an 19.5% CAGR during the forecast period for 2025-2034.

In agricultural settings, including farms, greenhouses, and animal facilities, computation hardware and systems that process data locally—at or close to the source of data generation are referred to as smart agriculture edge computing devices. IoT-enabled tools, sensors, and cameras are integrated into these devices to monitor a variety of metrics, including crop health, livestock behavior, temperature, humidity, and soil moisture. Therefore, in modern agricultural practices, smart agriculture edge devices are essential for precision farming, resource optimization, productivity growth, and the advancement of sustainability. The market for intelligent agriculture is expanding due to the increasing strain on the food supply chain and the rising need for sustainable practices.

Additionally, because loT and Al-based systems provide accurate, data-driven insights, the growing demand for these cutting-edge systems is a significant driver of the widespread adoption of smart agriculture technology. Real-time data collection from loT devices enables farmers to make well-informed decisions based on particular circumstances. The market does, however, confront certain obstacles, such as high startup costs and some farmers' lack of technological know-how. These obstacles may prevent broad adoption, especially in underdeveloped areas. Nevertheless, if governments and organizations invest in agricultural technology programs, there are many opportunities.

The smart agriculture edge computing devices market is segmented by component, type, deployment mode, application, connectivity, and end-use. By component, the market is segmented into software [data analytics platforms, edge al software, edge device management platforms], hardware [processors, networking devices, power management units, storage devices], and services [consulting services, deployment & integration, support & maintenance]. By type, the market is segmented into edge sensors, edge gateways, edge-integrated drones, edge nodes, edge servers, and edge-enabled cameras. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By application, the market is segmented into crop monitoring, precision farming, livestock monitoring, smart farm equipment management, greenhouse automation, irrigation management, and soil health monitoring. By connectivity, the market is segmented into Wi-Fi, bluetooth, zigbee, cellular (3G, 4G, 5G), and LPWAN (LoRa, NB-loT). By end-use, the market is segmented into agri-tech companies, agricultural cooperatives, large farms, small & medium farms, and research institutions.

The edge gateways category led the smart agriculture edge computing devices market in 2024 because they effectively control the data flow between centralized systems and field devices. Real-time analytics and protocol translation are made possible by these devices, which act as the main hubs for communication. Its capacity to preprocess and aggregate data at the edge greatly lowers bandwidth consumption and latency, which is essential for farms with poor connectivity. Both established and new markets are increasingly adopting edge gateways due to the growing need for quicker decision-making in precision agriculture.

The majority of edge computing usage in the smart agriculture edge computing devices industry is driven by the large farm sector, which requires scalable, automated, and data-driven solutions. To manage large acreages, maximize input use, and monitor workers and equipment in several locations, these farms make investments in edge infrastructure. They can implement cutting-edge AI applications for yield forecasting, illness detection, and autonomous equipment control because of their abundant resource availability. On the other hand, small and medium-sized farms are increasingly using edge devices to increase output while using fewer resources. These farms may gradually incorporate smart technologies owing to flexible and reasonably priced edge solutions.

The significant presence of technologically improved agricultural methods and the broad adoption of precision farming are driving the growth of the smart agriculture edge computing devices market in the North America region. The area gains from widespread internet use, cutting-edge cloud and edge technology, and government programs that support smart farming practices. Furthermore, the presence of important technology companies and agri-tech startups is accelerating the development and commercialization of edge computing systems in the agriculture industry.

In addition, the market for smart agriculture edge computing devices is growing quickly in the Asia Pacific area as a result of growing population-driven food demand and heightened attention to updating agricultural infrastructure. Agri-tech technologies are being invested in by nations like China, India, Japan, and Australia to increase production and resource efficiency. Drones, edge devices, and IoT-enabled sensors are becoming increasingly popular in the area. These tools facilitate localized data processing for pest detection, irrigation management, and crop health monitoring.

|

Report Attribute |

Specifications |

|

Market Size Value In 2024 |

USD 2.9 Bn |

|

Revenue Forecast In 2034 |

USD 16.7 Bn |

|

Growth Rate CAGR |

CAGR of 19.5% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Component, By Type, By Deployment Mode, By Application, By Connectivity, By End-use |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; Germany; The UK; France; Italy; Spain; Rest of Europe; China; Japan; India; South Korea; Southeast Asia; Rest of Asia Pacific; Brazil; Argentina; Mexico; Rest of Latin America; GCC Countries; South Africa; Rest of the Middle East and Africa |

|

Competitive Landscape |

John Deere, IBM, Microsoft, Siemens, AGCO, Alphabet (Google), FarmLogix, Arable Labs, Carbon Robotics, Huawei, Intel, Bosch, NVIDIA, Cisco, Amazon Web Services (AWS), Trimble, Qualcomm, Dell Technologies, Blue River Technology, and CropX |

|

Customization Scope |

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Geographic competitive landscape. |

|

Pricing and Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Smart Agriculture Edge Computing Devices Market by Component-

Smart Agriculture Edge Computing Devices Market by Type -

Smart Agriculture Edge Computing Devices Market by Deployment Mode-

Smart Agriculture Edge Computing Devices Market by Application-

Smart Agriculture Edge Computing Devices Market by Connectivity-

Smart Agriculture Edge Computing Devices Market by End-use-

Smart Agriculture Edge Computing Devices Market by Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

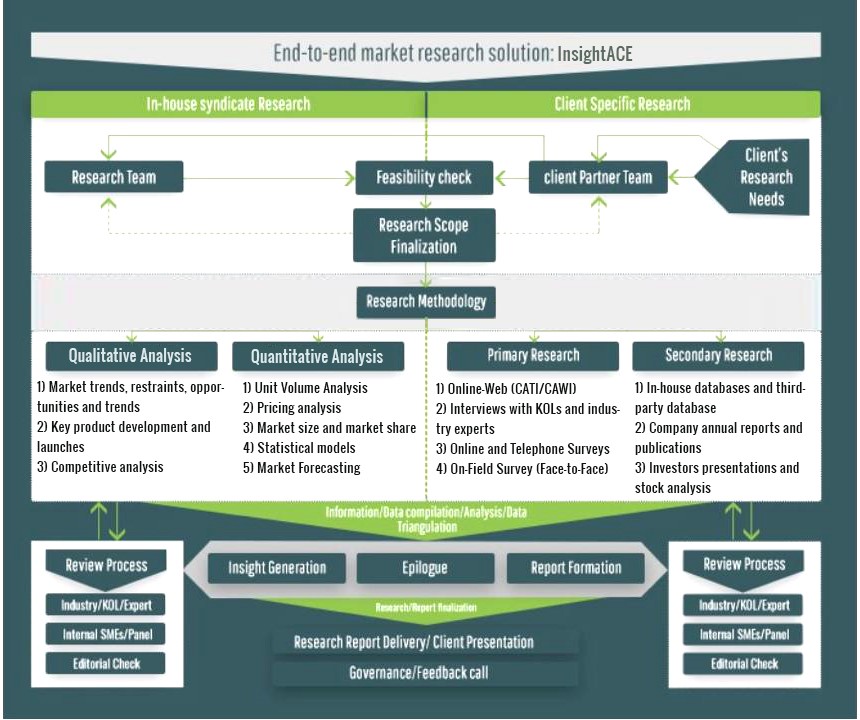

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.