Next-Generation Solar Cell Market Size is valued at USD 3.53 Bn in 2024 and is predicted to reach USD 21.50 Bn by the year 2034 at a 20.0% CAGR during the forecast period for 2025-2034.

Next-generation solar cells are advanced technologies that improve classic silicon-based solar cells' efficiency, cost-effectiveness, and adaptability. These technologies provide novel techniques for capturing and converting sunlight into electricity, frequently overcoming the limitations of traditional solar cells. Improving manufacturing techniques and utilizing novel materials can potentially lower the manufacturing costs of next-generation solar cells. This lowers the cost of solar energy and makes it more competitive with other energy generation sources.

Rapid advances in materials science, nanotechnology, and manufacturing techniques drive the development of next-generation solar cell technologies. Efficiency, stability, and scalability innovations are critical for achieving a competitive advantage in the market. Materials science, nanotechnology, and manufacturing process advancements have enabled the creation of novel solar cell technologies with increased efficiency and stability.

However, manufacturing firms encountered difficulties in keeping operations running while complying with safety procedures. Reduced workforce, slower output, and changes in work arrangements may have hampered the production of next-generation solar cells.

The Next-Generation Solar Cell Market is segmented on the basis of material type, installation and end-use industry. Based on material type, the market is segmented as transceivers, Cadmium Telluride (CdTe), Copper Indian Gallium Selenide (CIGS), Amorphous Silicone (a-Si), Gallium-Arsenide (GaAs), and others. The others are segmented into organic solar cells, dye-sensitized solar cells, and perovskite solar cells. By installation, the market is segmented into on-grid and off-grid. The end-users segment consists of residential, commercial & industrial, utilities, and others.

The perovskites solar cells category is expected to hold a major share of the global Next-Generation Solar Cell Market in 2022. Other material includes perovskite solar cells, organic solar cell, and dye-sensitized solar cells. Perovskite-structured materials utilized in solar cells are typically hybrid organic-inorganic lead or tin-halide compounds, such as methylammonium lead halide. Because these materials are solution-processed, their production is straightforward and economical. Hybrid metal halide perovskite solar cells (PSCs) have received a lot of attention due to their inexpensive cost, smaller design, low-temperature production, and outstanding light absorption qualities (high performance in low and diffuse light).

The commercial & industrial segment is projected to grow at a rapid rate in the global Next-Generation Solar Cell Market. Technological improvements, market trends, and environmental considerations contribute to the growing adoption of next-generation solar cells in the commercial and industrial sectors. Next-generation solar cells now have better efficiency, stability, and cost. Business processes are increasingly likely to include these technologies as they develop and become more dependable.

Asia Pacific's Next-Generation Solar Cell Market is anticipated to register the maximum market share in terms of revenue in the near future. The regional market is expanding as a result of the rising use of PV modules in countries like China, Japan, and India. Next-generation solar cells are more efficient than silicon-based cells and work well in both natural and artificial light. A next-generation solar cell is less than one micron thick and can be produced at low temperatures utilizing inexpensive methods like printing. Additionally, North America is anticipated to experience rapid growth during the projection period. The potential for next-generation solar cells to improve energy efficiency and advance sustainability goals has boosted attention in the region.

|

Report Attribute |

Specifications |

|

Market size value in 2024 |

USD 3.53 Bn |

|

Revenue forecast in 2034 |

USD 21.50 Bn |

|

Growth rate CAGR |

CAGR of 20.0% from 2025 to 2034 |

|

Quantitative units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments covered |

By Material Type, Installation, End-User Industry |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; The UK; France; Italy; Spain; South Korea; South East Asia |

|

Competitive Landscape |

Hanwha Q CELLS (South Korea), Oxford PV (UK), Kaneka Solar Energy (Japan), Flisom (Switzerland), Mitsubishi Chemical Group (Japan), and Hanergy thin film power group (China), Heliatek (Germany), 3D-Micromac(Germany), Suntech Power Holdings (China), Sharp Corporation(Japan), Trina Solar (China), Panasonic Corporation(Japan), Sol Voltaics(Sweden), Geo Green Power(England), Jinko Solar (China), Canadian Solar(Canada), Yingli Solar(China), REC Group(Norway), First Solar (US), Ascent Solar Technologies (US), Solactron (US), MiaSole (US), Polysolar Technology (US), NanoPV technologies(US), Sunpower Corporation(US) |

|

Customization scope |

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing and available payment methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Next-Generation Solar Cell Market By Material Type-

Next-Generation Solar Cell Market By Installation-

Next-Generation Solar Cell Market By End-User Industry-

Next-Generation Solar Cell Market By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

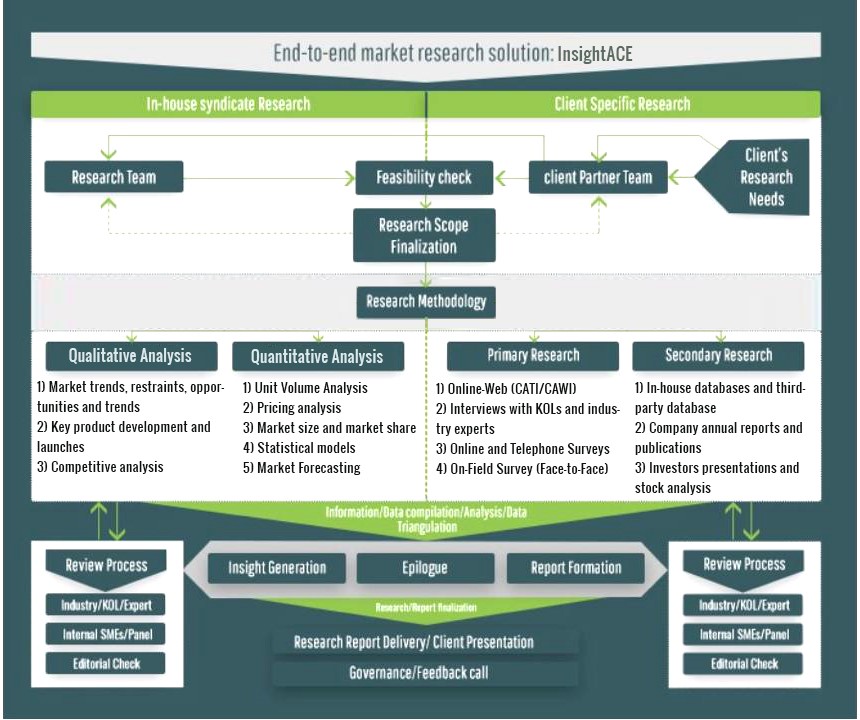

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.4456