The Electric Powertrain Market Size is valued at USD 86.9 Bn in 2023 and is predicted to reach USD 301.6 Bn by the year 2031 at an 17.1% CAGR during the forecast period for 2024-2031.

The E-powertrain refers to the system of components that generate and deliver power in electric vehicles (EVs) and hybrid electric vehicles (HEVs), replacing the traditional internal combustion engine (ICE) used in gasoline or diesel vehicles. It is responsible for converting electrical energy, typically stored in a battery, into mechanical energy to drive the vehicle's wheels. The e-powertrain market is experiencing rapid growth as electric mobility continues to rise. Future developments will focus on enhancing efficiency, reducing costs, and improving energy storage through innovations in battery technology, lightweight materials, and advanced power electronics. Additionally, the integration of e-powertrains with autonomous driving and connected vehicle technologies will further revolutionize the automotive industry.

The deterioration of air quality, caused by rising carbon and particulate matter emissions from cars, has severely impacted both the environment and human health. In response, governments worldwide have implemented stringent pollution regulations for automakers, prompting a surge in research and development for electric vehicles (EVs) and accelerating the development of e-powertrains. For instance, the road transportation sector significantly influences energy consumption in Europe. To achieve its net-zero greenhouse gas emissions target, the European Union continues to tighten CO2 emission limits for passenger cars and light commercial vehicles, driving the search for viable electric vehicle powertrain solutions. As a result, this has contributed to the global growth of the electric vehicle powertrain market.

Advancements in technology are addressing consumer demands for a longer range and improved performance while meeting regulatory requirements. Axial-flux motors and permanent magnet synchronous motors (PMSMs) are becoming increasingly popular due to their energy efficiency, higher torque, and compact size. Further innovations will focus on modular platforms and modular e-powertrains that combine motors, inverters, and transmission systems to optimize space and reduce costs. New battery technologies, such as solid-state and lithium-air, offer improved energy density and safety. These innovations will play a crucial role in advancing the electric powertrain market and helping the automotive industry achieve its goals of performance, sustainability, and widespread EV adoption.

The Future of the E-Powertrain market is segmented based on integration type, component, and propulsion, vehicle type. Based on the integration type, the market is divided into integrated & non-integrated. Based on the components, the market is divided into motor, battery, BMS, controller, PDM, inverter/converter, and onboard charger. Based on the propulsion, the market is divided into BEV and PHEV. Based on the vehicle type, the market is divided into PC & LCV.

Based on the integration type, the market is divided into integrated & non-integrated. Among these, the integrated segment is expected to have the highest growth rate during the forecast period. The integrated e-powertrain segment is expected to grow rapidly, supported by advancements in technology, the push for cost-efficient EV production, and the need for improved vehicle performance. The integration of key components enhances energy efficiency, as the systems are optimized to work together, reducing energy losses. Integrated systems free up space in EVs, which is essential for design flexibility, allowing for larger batteries or other innovative vehicle features. Integrated systems reduce the number of parts and complexity, leading to lower production costs. As the EV market matures, cost reductions are critical to achieving mass adoption.

Based on the components, the market is divided into motor, battery, BMS, controller, PDM, inverter/converter, and onboard charger. Among these, the battery-based segment dominates the market. the battery is the most critical component of an electric vehicle (EV) e-powertrain, as it directly determines the vehicle’s range, performance, and energy efficiency. It stores the electrical energy that powers the electric motor and other systems within the EV. Batteries account for the largest portion of the total cost of an EV, typically around 30-40%. As such, the battery segment has the largest financial impact on the e-powertrain market. Significant investments are being made in improving battery technology, driving both market share and growth. Increasing consumer demand for longer-range EVs, faster charging times, and lower costs are propelling advances in battery technology. Additionally, governmental regulations on emissions and fuel efficiency are accelerating the shift toward electrification, further expanding the battery market.

The Asia-Pacific region is expected to have the largest share and experience the most significant growth in the future of the e-powertrain market. Several factors contribute to this, making Asia-Pacific a dominant player in the global market. Governments in the Asia-Pacific region are implementing favorable policies, including subsidies, tax incentives, and emissions regulations, to encourage EV adoption. For example, China has strict New Energy Vehicle (NEV) mandates, which require automakers to produce a certain percentage of electric vehicles. China is the world’s largest electric vehicle (EV) market, both in terms of production and sales. The Chinese government has made substantial investments in EV infrastructure, battery production, and electric vehicle development, driving the rapid expansion of the e-powertrain market.

|

Report Attribute |

Specifications |

|

Market Size Value In 2023 |

USD 86.9 Bn |

|

Revenue Forecast In 2031 |

USD 301.6 Bn |

|

Growth Rate CAGR |

CAGR of 17.1% from 2024 to 2031 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2024 to 2031 |

|

Historic Year |

2019 to 2023 |

|

Forecast Year |

2024-2031 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Integration Type, Component, and Propulsion, Vehicle Type. |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South Korea; South East Asia |

|

Competitive Landscape |

Robert Bosch Gmbh, Mitsubishi Electric Corporation, Magna International Inc., Marelli Holdings Co., Ltd., Nissan Motor Co., Ltd., Sigma Powertrain, Inc., Continental Ag, Dana, BORGWARNER INC., Continental AG, ZF, Denso, Hitachi Astemo Americas, Inc., Valeo, CATL, BYD, LG, Panasonic, Samsung, Cummins Inc., Delta, Electronics, Inc., Hyundai Motor Company, Volkswagen |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing and Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Electric Powertrain Market Snapshot

Chapter 4. Global Electric Powertrain Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2024-2031

4.8. Global Electric Powertrain Market Penetration & Growth Prospect Mapping (US$ Mn), 2023-2031

4.9. Competitive Landscape & Market Share Analysis, By Key Player (2023)

4.10. Use/impact of AI on Electric Powertrain Industry Trends

Chapter 5. Electric Powertrain Market Segmentation 1: By Integration Type, Estimates & Trend Analysis

5.1. Market Share by Integration Type, 2023 & 2031

5.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Integration Type:

5.2.1. Integrated

5.2.2. Non-integrated

Chapter 6. Electric Powertrain Market Segmentation 2: By Component, Estimates & Trend Analysis

6.1. Market Share by Component, 2023 & 2031

6.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Components:

6.2.1. Motor

6.2.2. Battery

6.2.3. BMS

6.2.4. Controller

6.2.5. PDM

6.2.6. Inverter/Converter

6.2.7. On-Board Charger

Chapter 7. Electric Powertrain Market Segmentation 3: By Propulsion, Estimates & Trend Analysis

7.1. Market Share by Propulsion, 2023 & 2031

7.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Propulsions:

7.2.1. BEV

7.2.2. PHEV

Chapter 8. Electric Powertrain Market Segmentation 4: By Vehicle Type, Estimates & Trend Analysis

8.1. Market Share by Vehicle Type, 2023 & 2031

8.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Vehicle Types:

8.2.1. Passenger Cars

8.2.2. Light Commercial Vehicles

Chapter 9. Electric Powertrain Market Segmentation 5: Regional Estimates & Trend Analysis

9.1. Global Electric Powertrain Market, Regional Snapshot 2023 & 2031

9.2. North America

9.2.1. North America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.2.1.1. US

9.2.1.2. Canada

9.2.2. North America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Integration Type, 2024-2031

9.2.3. North America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Component, 2024-2031

9.2.4. North America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Propulsion, 2024-2031

9.2.5. North America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Vehicle Type, 2024-2031

9.3. Europe

9.3.1. Europe Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.3.1.1. Germany

9.3.1.2. U.K.

9.3.1.3. France

9.3.1.4. Italy

9.3.1.5. Spain

9.3.1.6. Rest of Europe

9.3.2. Europe Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Integration Type, 2024-2031

9.3.3. Europe Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Component, 2024-2031

9.3.4. Europe Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Propulsion, 2024-2031

9.3.5. Europe Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Vehicle Type, 2024-2031

9.4. Asia Pacific

9.4.1. Asia Pacific Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.4.1.1. India

9.4.1.2. China

9.4.1.3. Japan

9.4.1.4. Australia

9.4.1.5. South Korea

9.4.1.6. Hong Kong

9.4.1.7. Southeast Asia

9.4.1.8. Rest of Asia Pacific

9.4.2. Asia Pacific Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Integration Type, 2024-2031

9.4.3. Asia Pacific Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Component, 2024-2031

9.4.4. Asia Pacific Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts By Propulsion, 2024-2031

9.4.5. Asia Pacific Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Vehicle Type, 2024-2031

9.5. Latin America

9.5.1. Latin America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.5.1.1. Brazil

9.5.1.2. Mexico

9.5.1.3. Rest of Latin America

9.5.2. Latin America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Integration Type, 2024-2031

9.5.3. Latin America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Component, 2024-2031

9.5.4. Latin America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Propulsion, 2024-2031

9.5.5. Latin America Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Vehicle Type, 2024-2031

9.6. Middle East & Africa

9.6.1. Middle East & Africa Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by country, 2024-2031

9.6.1.1. GCC Countries

9.6.1.2. Israel

9.6.1.3. South Africa

9.6.1.4. Rest of Middle East and Africa

9.6.2. Middle East & Africa Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Integration Type, 2024-2031

9.6.3. Middle East & Africa Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Component, 2024-2031

9.6.4. Middle East & Africa Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Propulsion, 2024-2031

9.6.5. Middle East & Africa Electric Powertrain Market Revenue (US$ Million) Estimates and Forecasts by Vehicle Type, 2024-2031

Chapter 10. Competitive Landscape

10.1. Major Mergers and Acquisitions/Strategic Alliances

10.2. Company Profiles

10.2.1. Robert Bosch Gmbh

10.2.1.1. Business Overview

10.2.1.2. Key Product/Service Offerings

10.2.1.3. Financial PerIntegration Typeance

10.2.1.4. Geographical Presence

10.2.1.5. Recent Developments with Business Strategy

10.2.2. Mitsubishi Electric Corporation

10.2.3. Magna International Inc.

10.2.4. Marelli Holdings Co., Ltd.

10.2.5. Nissan Motor Co., Ltd.

10.2.6. Sigma Powertrain, Inc.

10.2.7. Continental Ag

10.2.8. Dana

10.2.9. BORGWARNER INC.

10.2.10. Continental AG

10.2.11. ZF

10.2.12. Denso

10.2.13. Hitachi Astemo Americas, Inc.

10.2.14. Valeo

10.2.15. CATL

10.2.16. BYD

10.2.17. LG

10.2.18. Panasonic

10.2.19. Samsung

10.2.20. Cummins Inc.

10.2.21. Delta Electronics, Inc.

10.2.22. Hyundai Motor Company

10.2.23. Volkswagen

10.2.24. Other Market Players

Global Electric Powertrain Market- By Integration Type

Global Electric Powertrain Market – By Component

Global Electric Powertrain Market – By Propulsion

Global Electric Powertrain Market – By Vehicle Type

Global Electric Powertrain Market – By Region

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

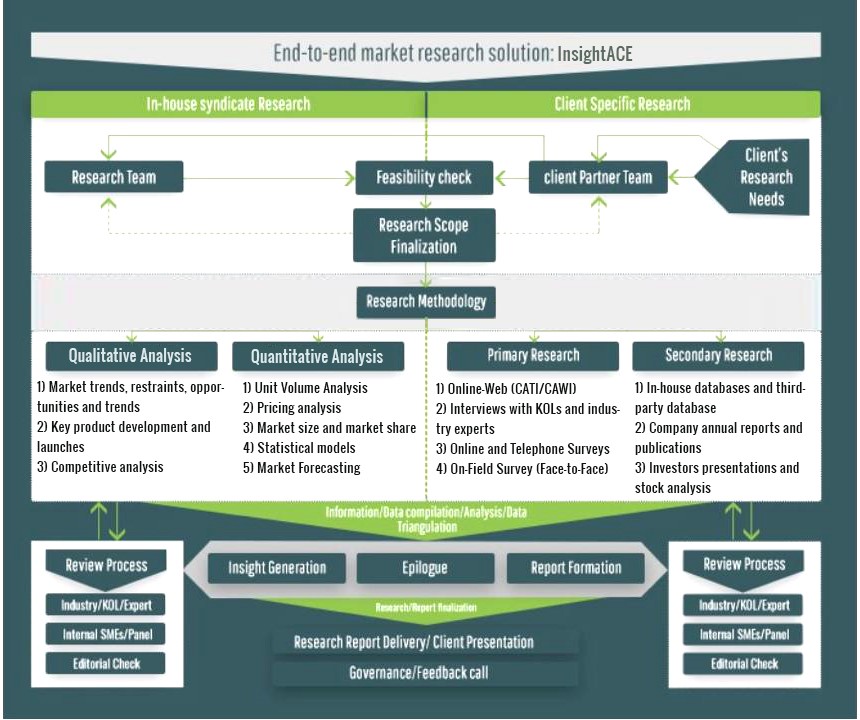

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.