The Edge Data Center Market Size is valued at USD 16.6 Bn in 2023 and is predicted to reach USD 61.2 Bn by the year 2031 at an 18.1% CAGR during the forecast period for 2024-2031.

An Edge Data Center is a small-scale data center strategically located near end-users or devices to bring computing power, storage, and network services closer to where data is generated and consumed. Its primary purpose is to reduce latency, improve performance, and enable faster data processing by avoiding the need to send information to distant, centralized data centers. Typically positioned near population centers or within local networks, edge data centers minimize data travel time. These smaller, more distributed centers often work alongside larger, centralized cloud data centers and are designed to scale based on demand, especially in areas with high user density. Unlike traditional data centers, edge data centers support localized workloads without requiring massive infrastructure.

Implementing robust security measures, such as access controls, encryption, and physical security, is essential to protect sensitive data and infrastructure in edge data centers from cyber threats and unauthorized access. With stricter data privacy regulations like the General Data Protection Regulation (GDPR) and the Central Consumer Protection Authority (CCPA), the need for enhanced security at the edge has become more pressing. Key measures, including data encryption, access controls, and regular security audits, are critical for safeguarding data processed at the edge. For example, in May 2023, Vertiv Group introduced modular data centers designed for rapid deployment and scalability, addressing the growing demand for flexible and agile edge solutions.

Micro data centers are also gaining popularity for edge deployments, offering compact and efficient solutions for specific use cases. As businesses prioritize digital transformation projects to support advanced applications and technologies, investments in edge infrastructure are likely to increase. In response to rising concerns over data breaches and regulatory compliance, edge data centers are expected to implement stronger security measures, enhancing consumer trust. Additionally, the need for edge computing solutions to reduce latency and boost performance is expected to drive market growth, as user experience becomes a key differentiator for businesses.

The Edge Data Center market is segmented based on end-use industry, and data center type. Based on the end-use industry, the market is divided into IT and telecom, banking, financial services, insurance (BFSI), government and public sector, healthcare, manufacturing, automotive, retail, and others. Based on the data center type, the market is divided into on-premise edge, network edge, and regional edge.

Based on the end-use industry, the market is divided into IT and telecom, banking, financial services, insurance (BFSI), government and public sector, healthcare, manufacturing, automotive, retail, and others. Among these, the IT and telecom segment is expected to have the highest growth rate during the forecast period. This sector has the highest demand for edge data centers due to the rapid expansion of 5G networks, increased data consumption, and the growing need for faster data processing and reduced latency to support cloud services, video streaming, IoT applications, and other digital services.

The telecom industry, in particular, leverages edge data centers to enhance network efficiency, provide low-latency communication, and ensure seamless connectivity. The IT and telecom sectors generate massive volumes of data from smartphones, IoT devices, cloud services, and content delivery networks (CDNs). Edge data centers help handle this data by processing it locally, reducing the load on centralized data centers, and minimizing latency. The proliferation of IoT devices, especially in telecom, requires localized data processing. Edge data centers facilitate faster data analysis and decision-making for connected devices, enhancing real-time monitoring and control.

Based on the data center type, the market is divided into on-premise edge, network edge, and regional edge. Among these, the rising demand for video streaming, online gaming, and other bandwidth-heavy services is best served by the Network Edge. By caching content closer to users, Network Edge data centers improve performance, reduce buffering, and enhance the user experience. Network Edge data centers allow for local data processing and reduce the burden on centralized data centers, ensuring quicker response times and supporting large-scale IoT deployments. The Network Edge is crucial for telecom operators and IT service providers, as it supports the infrastructure needed for low-latency applications and efficient network management. As these sectors grow, the need for network-edge data centers continues to rise.

North America, particularly the United States, is a leader in the early adoption of advanced technologies like 5G, IoT, and cloud computing, which are key drivers for edge data center deployment. The rapid deployment of 5G networks across the U.S. and Canada is increasing the demand for edge data centers to support low-latency, high-bandwidth applications, such as autonomous vehicles, smart cities, and AR/VR. a high adoption rate of IoT devices across various industries, including healthcare, automotive, and manufacturing. This creates a need for localized processing power, driving the demand for edge data centers.

|

Report Attribute |

Specifications |

|

Market Size Value In 2023 |

USD 16.6 Bn |

|

Revenue Forecast In 2031 |

USD 61.2 Bn |

|

Growth Rate CAGR |

CAGR of 18.1% from 2024 to 2031 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2024 to 2031 |

|

Historic Year |

2019 to 2023 |

|

Forecast Year |

2024-2031 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By End-Use Industry, and Data Center Type |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South Korea; South East Asia |

|

Competitive Landscape |

ATLASEDGE DATA CENTRES, ATC TRS V LLC, Cologix, Vapor IO, DartPoints, Digital Realty, Edge Centres, EdgeConneX, Ubiquity Management, LLC, Leading Edge Data Centres, Proximity Data Centres, Switch, Vertiv Group Corp, Evoque Data Center Solutions, Flexential, DELL, EATON, IBM, NVIDIA, Schneider Electric, Fujitsu, Cisco, Huawei, 365 Data Centers, Rittal, Panduit, Equinix, Sunbird, Vertiv Group, Huber+Suhner, Siemon |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing and Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Edge Data Center Market Snapshot

Chapter 4. Global Edge Data Center Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2024-2031

4.8. Global Edge Data Center Market Penetration & Growth Prospect Mapping (US$ Mn), 2023-2031

4.9. Competitive Landscape & Market Share Analysis, By Key Player (2023)

4.10. Use/impact of AI on Edge Data Center Industry Trends

Chapter 5. Edge Data Center Market Segmentation 1: By End-Use Industry, Estimates & Trend Analysis

5.1. Market Share by End-Use Industry, 2023 & 2031

5.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following End-Use Industry:

5.2.1. IT and Telecom

5.2.2. Banking, Financial Services, and Insurance (BFSI)

5.2.3. Government and Public Sector

5.2.4. Healthcare

5.2.5. Manufacturing

5.2.6. Automotive

5.2.7. Retail

5.2.8. Others

Chapter 6. Edge Data Center Market Segmentation 2: By Data Center Type, Estimates & Trend Analysis

6.1. Market Share by Data Center Type, 2023 & 2031

6.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Data Center Types:

6.2.1. On-Premise Edge

6.2.2. Network Edge

6.2.3. Regional Edge

Chapter 7. Edge Data Center Market Segmentation 6: Regional Estimates & Trend Analysis

7.1. Global Edge Data Center Market, Regional Snapshot 2023 & 2031

7.2. North America

7.2.1. North America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

7.2.1.1. US

7.2.1.2. Canada

7.2.2. North America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by End-Use Industry, 2024-2031

7.2.3. North America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Data Center Type, 2024-2031

7.3. Europe

7.3.1. Europe Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

7.3.1.1. Germany

7.3.1.2. U.K.

7.3.1.3. France

7.3.1.4. Italy

7.3.1.5. Spain

7.3.1.6. Rest of Europe

7.3.2. Europe Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by End-Use Industry, 2024-2031

7.3.3. Europe Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Data Center Type, 2024-2031

7.4. Asia Pacific

7.4.1. Asia Pacific Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

7.4.1.1. India

7.4.1.2. China

7.4.1.3. Japan

7.4.1.4. Australia

7.4.1.5. South Korea

7.4.1.6. Hong Kong

7.4.1.7. Southeast Asia

7.4.1.8. Rest of Asia Pacific

7.4.2. Asia Pacific Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by End-Use Industry, 2024-2031

7.4.3. Asia Pacific Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts By Data Center Type, 2024-2031

7.5. Latin America

7.5.1. Latin America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

7.5.1.1. Brazil

7.5.1.2. Mexico

7.5.1.3. Rest of Latin America

7.5.2. Latin America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by End-Use Industry, 2024-2031

7.5.3. Latin America Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Data Center Type, 2024-2031

7.6. Middle East & Africa

7.6.1. Middle East & Africa Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by country, 2024-2031

7.6.1.1. GCC Countries

7.6.1.2. Israel

7.6.1.3. South Africa

7.6.1.4. Rest of Middle East and Africa

7.6.2. Middle East & Africa Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by End-Use Industry, 2024-2031

7.6.3. Middle East & Africa Edge Data Center Market Revenue (US$ Million) Estimates and Forecasts by Data Center Type, 2024-2031

Chapter 8. Competitive Landscape

8.1. Major Mergers and Acquisitions/Strategic Alliances

8.2. Company Profiles

8.2.1. ATLASEDGE DATA CENTRES

8.2.1.1. Business Overview

8.2.1.2. Key Product/Service Offerings

8.2.1.3. Financial Performance

8.2.1.4. Geographical Presence

8.2.1.5. Recent Developments with Business Strategy

8.2.2. ATC TRS V LLC

8.2.3. Cologix

8.2.4. Vapor IO

8.2.5. DartPoints

8.2.6. Digital Realty

8.2.7. Edge Centres

8.2.8. EdgeConneX

8.2.9. Ubiquity Management, LLC

8.2.10. Leading Edge Data Centres

8.2.11. Proximity Data Centres

8.2.12. Switch

8.2.13. Vertiv Group Corp

8.2.14. Evoque Data Center Solutions

8.2.15. Flexential

8.2.16. DELL

8.2.17. EATON

8.2.18. IBM

8.2.19. NVIDIA

8.2.20. Schneider Electric

8.2.21. Fujitsu

8.2.22. Cisco

8.2.23. Huawei

8.2.24. 365 Data Centers

8.2.25. Rittal

8.2.26. Panduit

8.2.27. Equinix

8.2.28. Sunbird

8.2.29. Vertiv Group

8.2.30. Huber+Suhner

8.2.31. Siemon

Global Edge Data Center Market- By End-Use Industry

Global Edge Data Center Market – By Data Center Type

Global Edge Data Center Market – By Region

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

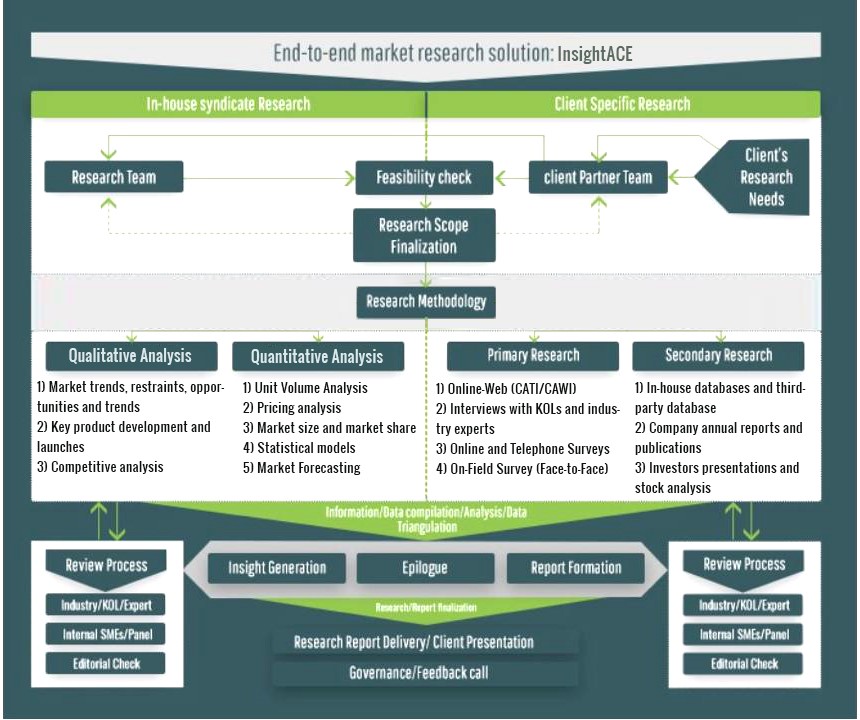

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.