Global Digital Health for Obesity Market Size Was valued at USD 63.4 Bn in 2024 and is predicted to reach USD 490.2 Bn by 2034 at a 23.1% CAGR during the forecast period for 2025-2034.

The goal of digital health for obesity is to prevent, manage, and treat obesity and related medical disorders by utilizing digital technologies such as wearable technology, telemedicine platforms, smartphone apps, and internet resources. It includes a range of digital tools and treatments designed to promote healthy habits, assess body weight and activity levels, track eating patterns, provide educational materials, and facilitate online consultations with medical professionals. With the help of digital health for obesity solutions, people can set realistic goals, adopt healthier lifestyles, and get individualized support and assistance to reach and stay at a healthy weight.

The global obesity epidemic and the health problems that come with it, such as diabetes, heart disease, and some types of cancer, are fueling the demand for digital health for obesity. As wearable technology, smartphone apps, and connected health technologies become more widely used, real-time monitoring and feedback are made possible, which improves accountability and participation in obesity management initiatives. Additionally, the digital health for obesity market is growing and being adopted due to government initiatives and healthcare policies that focus on controlling and preventing chronic diseases, including obesity. These policies also encourage investment in digital health solutions and payment for virtual care services.

However, obstacles, including interoperability problems, data privacy difficulties, and the requirement for large infrastructure and training investments, stand in the way of the broad use of operational analytics solutions. The digital health for obesity market is anticipated to increase in the next few years, despite these obstacles, due to ongoing technological advancements and the growing importance of data-driven decision-making.

Some of the Major Key Players in the Digital Health for Obesity Market are:

The digital health for obesity market is segmented based on components and end-users. Based on components, the market is segmented into hardware, software, and services. By end-user, the market is segmented into patients, payers, providers, and others.

The services category is expected to hold a major global market share in 2024. The rising demand for installation, upkeep, training, and other services is accountable for this expansion. Additionally, the service sector is expanding due to the rising demand for sophisticated software platforms and solutions like Electronic Medical Records (EMRs) and Electronic Health Records (EHRs), as well as the growing requirement for training and upgrades to operate these software programs. Key players offer a broad range of services before and after installation, including resource allocation and optimization, project planning, training, and execution.

The patients segment generated the most market share in 2024 due to the growing need for individualized and easily accessible healthcare solutions, which is the primary driver of this dominance. As the primary consumers of digital health, patients actively utilise wearables, smartphone applications, and other devices to track and manage diseases such as obesity. Further propelling the use of digital health technologies is the convenience of self-management coupled with growing self-awareness of wellness and health. The segment dominance during the forecast period is a result of these factors taken together.

The North American digital health for obesity market is expected to register the highest market share in revenue in the near future because of its high rates of obesity, sophisticated healthcare system, and robust digital technology use. The area is home to many tech-savvy people who frequently utilize health apps, fitness trackers, and cell phones. The need is also fueled by high healthcare costs and government backing for digital health projects. Additionally, the region has grown due to the presence of top health tech businesses and research institutions, which have stimulated innovation in tailored obesity care.

In addition, Asia Pacific is projected to grow rapidly in the global digital health for obesity market. The region's obesity rates are rapidly increasing as a result of dietary modifications, urbanization, and shifting lifestyles. As obesity becomes a more significant health issue, there is a great demand for numerous useful solutions, including digital health technologies. Governments and healthcare organizations in the area are increasingly realizing the potential of digital health to address public health concerns like obesity. Investments in healthcare infrastructure and laws that encourage the use of digital health are driving the market's growth.

|

Report Attribute |

Specifications |

|

Market Size Value In 2024 |

USD 63.4 Bn |

|

Revenue Forecast In 2034 |

USD 490.2 Bn |

|

Growth Rate CAGR |

CAGR of 23.1% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Components, By End-User |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South East Asia; South Korea |

|

Competitive Landscape |

Noom, PlateJoy HEALTH, WW International, WellDoc, Teladoc Health, Inc., MyFitnessPal, Healthify (My Diet Coach), Fitbit, Inc., Tempus, Fitnesskeeper Inc., Sidekick Health, BioAge Labs, and others. |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Digital Health For Obesity Market Snapshot

Chapter 4. Global Digital Health For Obesity Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2025-2034

4.8. Global Digital Health For Obesity Market Penetration & Growth Prospect Mapping (US$ Mn), 2024-2034

4.9. Competitive Landscape & Market Share Analysis, By Key Player (2024)

4.10. Use/impact of AI on Digital Health For Obesity Market Industry Trends

Chapter 5. Digital Health For Obesity Market Segmentation 1: By Component, Estimates & Trend Analysis

5.1. Market Share by Component, 2024 & 2034

5.2. Market Size (Value (US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following Component:

5.2.1. Software

5.2.2. Hardware

5.2.3. Services

Chapter 6. Digital Health For Obesity Market Segmentation 2: By End Use, Estimates & Trend Analysis

6.1. Market Share by End Use, 2024 & 2034

6.2. Market Size (Value (US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following End Use:

6.2.1. Patients

6.2.2. Providers

6.2.3. Payers

6.2.4. Others

Chapter 7. Digital Health For Obesity Market Segmentation 3: Regional Estimates & Trend Analysis

7.1. Global Digital Health For Obesity Market, Regional Snapshot 2024 & 2034

7.2. North America

7.2.1. North America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Country, 2021-2034

7.2.1.1. US

7.2.1.2. Canada

7.2.2. North America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Component, 2021-2034

7.2.3. North America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by End Use, 2021-2034

7.3. Europe

7.3.1. Europe Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Country, 2021-2034

7.3.1.1. Germany

7.3.1.2. U.K.

7.3.1.3. France

7.3.1.4. Italy

7.3.1.5. Spain

7.3.1.6. Rest of Europe

7.3.2. Europe Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Component, 2021-2034

7.3.3. Europe Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by End Use, 2021-2034

7.4. Asia Pacific

7.4.1. Asia Pacific Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Country, 2021-2034

7.4.1.1. India

7.4.1.2. China

7.4.1.3. Japan

7.4.1.4. Australia

7.4.1.5. South Korea

7.4.1.6. Hong Kong

7.4.1.7. Southeast Asia

7.4.1.8. Rest of Asia Pacific

7.4.2. Asia Pacific Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Component, 2021-2034

7.4.3. Asia Pacific Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by End Use, 2021-2034

7.5. Latin America

7.5.1. Latin America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Country, 2021-2034

7.5.1.1. Brazil

7.5.1.2. Mexico

7.5.1.3. Rest of Latin America

7.5.2. Latin America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Component, 2021-2034

7.5.3. Latin America Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by End Use, 2021-2034

7.6. Middle East & Africa

7.6.1. Middle East & Africa Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by country, 2021-2034

7.6.1.1. GCC Countries

7.6.1.2. Israel

7.6.1.3. South Africa

7.6.1.4. Rest of Middle East and Africa

7.6.2. Middle East & Africa Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by Component, 2021-2034

7.6.3. Middle East & Africa Digital Health For Obesity Market Revenue (US$ Mn) Estimates and Forecasts by End Use, 2021-2034

Chapter 8. Competitive Landscape

8.1. Major Mergers and Acquisitions/Strategic Alliances

8.2. Company Profiles

8.2.1. WW International

8.2.1.1. Business Overview

8.2.1.2. Key Product/Service

8.2.1.3. Financial Performance

8.2.1.4. Geographical Presence

8.2.1.5. Recent Developments with Business Strategy

8.2.2. MyFitnessPal

8.2.3. Teladoc Health, Inc.

8.2.4. Fitnesskeeper Inc.

8.2.5. Healthify (My Diet Coach)

8.2.6. Fitbit, Inc.

8.2.7. Noom

8.2.8. PlateJoy HEALTH

8.2.9. Tempus

8.2.10. WellDoc

8.2.11. Sidekick Health

8.2.12. BioAge Labs

Segmentation of Digital Health for Obesity Market-

Digital Health for Obesity Market-By Component

Digital Health for Obesity Market-By End-User

Digital Health for Obesity Market-By Region

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

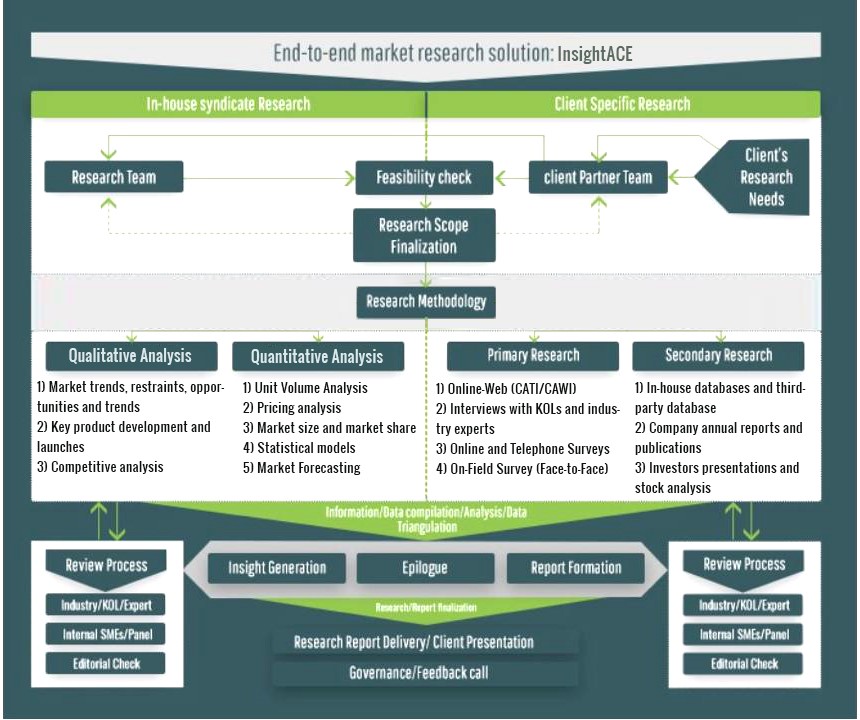

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.