The Automotive Thermoplastic Polymer Composite Market Size is valued at USD 8.53 Bn in 2023 and is predicted to reach USD 12.65 Bn by the year 2031 at an 5.2% CAGR during the forecast period for 2024-2031.

The automotive thermoplastic polymer composite market is dynamically transforming with the advancement of better-quality materials that can contribute toward better performance and solve environment-related issues. Thermoplastic polymer composites made for the automotive sector comprise a mixture of reinforcing glass or carbon fibers along with thermoplastic polymers, resulting in lightweight materials that can be shaped in complex geometries with much strength. The various applications in the automotive field make these composites highly suitable, which are predominantly the outer parts such as bumpers and body panels, inner parts such as dashboards and door panels, structural components supporting the body structure of the vehicle, and under-the-hood components which endure high temperatures due to stress.

Light vehicles form one of the growth drivers for the market. Methods to reduce the overall weight of a vehicle are employed by manufacturers to combat stringent emission regulations and lessen fuel consumption. Cutting just 10 kilograms from the weight of a vehicle could cut carbon dioxide emissions by approximately 1 gram per kilometer. This focus on sustainability is supporting the need for regulation compliance and consumer desire for green automobiles, so appealing to the use of thermoplastic polymer composites in automotive design.

The automotive thermoplastic polymer composite market is segmented by application, type, end user, and manufacturing process. By application, the market is segmented into exterior body parts, interior components, structural components, automated parts, and under-the-hood applications. By type market is categorized into polyamide, polypropylene, polycarbonate, acrylonitrile butadiene styrene, thermoplastic polyurethane. By end user market is categorized into passenger vehicles, commercial vehicles, electric vehicles, hybrid vehicles, luxury vehicles. By manufacturing process, the market is categorized into injection molding, compression molding, blow molding, thermoforming, 3d printing.

Polyamide (PA) is a strong growth driver in the automotive thermoplastic polymer composite market as it is lightweight, highly temperature resistant, durable, and resistant to chemicals, which make it indispensable for fuel efficiency improvement and to meet the required level of emissions. Its resistance to high temperatures and wear makes it suitable for challenging applications such as under-the-hood components. Throughout the entire automotive sector, this thermoplastic is often used in air intake manifolds that normally comprise replacement parts with metal, such as reinforced-glass PA; fuel systems because of their chemical resistant attribute, safety attributes like bags' storage containers-against-impact properties, or electronic systems used in most forms of EVs-superb insulation characteristic for harness cable and wiring.

The most rapidly growing process in the automotive thermoplastic polymer composite market is injection molding, primarily because of efficiency and the potential for producing large volumes and suitability for producing complex shapes demanded by modern vehicle components. The material utilization can also be supported with this process since material waste can be avoided since the leftover material can sometimes be recycled. This includes the potential to enable lightweight thermoplastic composites, such as polyamide and polypropylene, where the trend in the automotive industry to reduce vehicle weight continues to be driven by requirements for improved fuel efficiency and lower emissions. In addition, improvements in injection molding technology, such as enhanced processing control and material formulations, are decreasing production costs and cycle times, making this technology increasingly appealing for use in the automotive industry.

Europe is the current market leader in automotive thermoplastic polymer composites, with a strong automotive industry and major manufacturers in countries such as Germany, France, and Italy, which are renowned for innovation and quality. European automobile manufacturers invest billions of euros in R&D; in 2022 alone, €363 billion was spent toward the creation of lightweight, fuel-efficient vehicles, which speeds up the adoption of thermoplastic composites for weight loss and efficiency improvement. Another high-impact driver is the strict emission standards of the EU, forcing automotive companies to adopt lightweight material. Sustainability initiatives for natural fiber-based eco-friendly composites are also on the rise. The rapid expansion of EVs in Europe consequently requires higher demand, as the usage of composites helps maximize battery efficiency, which in turn enhances vehicle performance.

|

Report Attribute |

Specifications |

|

Market Size Value In 2023 |

USD 8.53 Bn |

|

Revenue Forecast In 2031 |

USD 12.65 Bn |

|

Growth Rate CAGR |

CAGR of 5.2% from 2024 to 2031 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2024 to 2031 |

|

Historic Year |

2019 to 2023 |

|

Forecast Year |

2024-2031 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Application, Type, End User, Manufacturing Process |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico; France; Italy; Spain; South Korea; Southeast Asia |

|

Competitive Landscape |

Covestro, DuPont, Teijin, Kraton Corporation, BASF, Lanxess, SABIC, Solvay, TenCate, Eastman Chemical Company, Continental, LG Chem, PolyOne, Forgeway, Mitsubishi Chemical, Reliance Industries Limited, Advanced Composites Pvt Ltd, SGL Carbon India Pvt Ltd, Tata AutoComp Systems Ltd, SABIC Innovative Plastics India Pvt Ltd |

|

Customization Scope |

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Geographic competitive landscape. |

|

Pricing and Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Automotive Thermoplastic Polymer Composite Market Snapshot

Chapter 4. Global Automotive Thermoplastic Polymer Composite Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2024-2031

4.8. Global Automotive Thermoplastic Polymer Composite Market Penetration & Growth Prospect Mapping (US$ Mn), 2023-2031

4.9. Competitive Landscape & Market Share Analysis, By Key Player (2023)

4.10. Use/impact of AI on Automotive Thermoplastic Polymer Composite Industry Trends

Chapter 5. Automotive Thermoplastic Polymer Composite Market Segmentation 1: By Application , Estimates & Trend Analysis

5.1. Market Share by Application , 2023 & 2031

5.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Application :

5.2.1. Exterior Body Parts

5.2.2. Interior Components

5.2.3. Structural Components

5.2.4. Automated Parts

5.2.5. Under-the-Hood Applications

Chapter 6. Automotive Thermoplastic Polymer Composite Market Segmentation 2: By Type, Estimates & Trend Analysis

6.1. Market Share by Type, 2023 & 2031

6.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Type:

6.2.1. Polyamide

6.2.2. Polypropylene

6.2.3. Polycarbonate

6.2.4. Acrylonitrile Butadiene Styrene

6.2.5. Thermoplastic Polyurethane

Chapter 7. Automotive Thermoplastic Polymer Composite Market Segmentation 3: By End User, Estimates & Trend Analysis

7.1. Market Share by End User, 2023 & 2031

7.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following End User:

7.2.1. Passenger Vehicles

7.2.2. Commercial Vehicles

7.2.3. Electric Vehicles

7.2.4. Hybrid Vehicles

7.2.5. Luxury Vehicles

Chapter 8. Automotive Thermoplastic Polymer Composite Market Segmentation 4: By Manufacturing Process, Estimates & Trend Analysis

8.1. Market Share by Manufacturing Process, 2023 & 2031

8.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2019 to 2031 for the following Manufacturing Process:

8.2.1. Injection Molding

8.2.2. Compression Molding

8.2.3. Blow Molding

8.2.4. Thermoforming

8.2.5. 3D Printing

Chapter 9. Automotive Thermoplastic Polymer Composite Market Segmentation 5: Regional Estimates & Trend Analysis

9.1. Global Automotive Thermoplastic Polymer Composite Market, Regional Snapshot 2023 & 2031

9.2. North America

9.2.1. North America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.2.1.1. US

9.2.1.2. Canada

9.2.2. North America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Application , 2024-2031

9.2.3. North America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Type, 2024-2031

9.2.4. North America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by End User, 2024-2031

9.2.5. North America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Manufacturing Process, 2024-2031

9.3. Europe

9.3.1. Europe Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.3.1.1. Germany

9.3.1.2. U.K.

9.3.1.3. France

9.3.1.4. Italy

9.3.1.5. Spain

9.3.1.6. Rest of Europe

9.3.2. Europe Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Application , 2024-2031

9.3.3. Europe Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Type, 2024-2031

9.3.4. Europe Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by End User, 2024-2031

9.3.5. Europe Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Manufacturing Process, 2024-2031

9.4. Asia Pacific

9.4.1. Asia Pacific Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.4.1.1. India

9.4.1.2. China

9.4.1.3. Japan

9.4.1.4. Australia

9.4.1.5. South Korea

9.4.1.6. Hong Kong

9.4.1.7. Southeast Asia

9.4.1.8. Rest of Asia Pacific

9.4.2. Asia Pacific Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Application , 2024-2031

9.4.3. Asia Pacific Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Type, 2024-2031

9.4.4. Asia Pacific Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts By End User, 2024-2031

9.4.5. Asia Pacific Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Manufacturing Process, 2024-2031

9.5. Latin America

9.5.1. Latin America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Country, 2024-2031

9.5.1.1. Brazil

9.5.1.2. Mexico

9.5.1.3. Rest of Latin America

9.5.2. Latin America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Application , 2024-2031

9.5.3. Latin America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Type, 2024-2031

9.5.4. Latin America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by End User, 2024-2031

9.5.5. Latin America Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Manufacturing Process, 2024-2031

9.6. Middle East & Africa

9.6.1. Middle East & Africa Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by country, 2024-2031

9.6.1.1. GCC Countries

9.6.1.2. Israel

9.6.1.3. South Africa

9.6.1.4. Rest of Middle East and Africa

9.6.2. Middle East & Africa Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Application , 2024-2031

9.6.3. Middle East & Africa Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Type, 2024-2031

9.6.4. Middle East & Africa Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by End User, 2024-2031

9.6.5. Middle East & Africa Automotive Thermoplastic Polymer Composite Market Revenue (US$ Million) Estimates and Forecasts by Manufacturing Process, 2024-2031

Chapter 10. Competitive Landscape

10.1. Major Mergers and Acquisitions/Strategic Alliances

10.2. Company Profiles

10.2.1. Covestro

10.2.1.1. Business Overview

10.2.1.2. Key End User/Service Offerings

10.2.1.3. Financial Performance

10.2.1.4. Geographical Presence

10.2.1.5. Recent Developments with Business Strategy

10.2.2. DuPont

10.2.3. Teijin

10.2.4. Kraton Corporation

10.2.5. BASF

10.2.6. Lanxess

10.2.7. SABIC

10.2.8. Solvay

10.2.9. TenCate

10.2.10. Eastman Chemical Company

10.2.11. Continental

10.2.12. LG Chem

10.2.13. PolyOne

10.2.14. Forgeway

10.2.15. Mitsubishi Chemical

10.2.16. Reliance Industries Limited

10.2.17. Advanced Composites Pvt Ltd

10.2.18. SGL Carbon India Pvt Ltd

10.2.19. Tata AutoComp Systems Ltd

10.2.20. SABIC Innovative Plastics India Pvt Ltd

10.2.21. Other Prominent Players

Automotive Thermoplastic Polymer Composite Market by Application -

Automotive Thermoplastic Polymer Composite Market by Type -

Automotive Thermoplastic Polymer Composite Market by End User -

Automotive Thermoplastic Polymer Composite Market by Manufacturing Process -

Automotive Thermoplastic Polymer Composite Market by Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

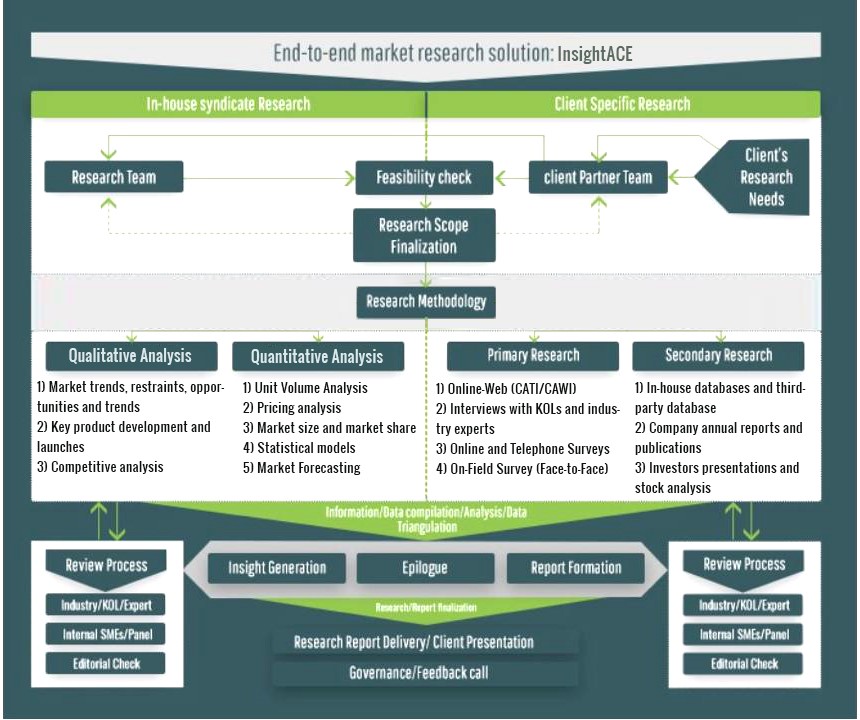

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.