Facility Management Market Size is valued at USD 52.96 Bn in 2024 and is predicted to reach USD 170.04 Bn by the year 2034 at a 12.5% CAGR during the forecast period for 2025-2034.

Facility management refers to the resources and expertise that keep structures, outdoor areas, utilities, and other real estate operating smoothly, safely, and sustainably. Facility management software and services that increase their efficiency and effectiveness are the initial focus of this research. These services include emergency planning and business continuity, environmental sustainability, human resources, communication, project management, quality assurance, real estate and property management, and strategic planning and leadership.

The need for these services and solutions has been on the rise, and it will continue to rise rapidly in the years to come. Government spending in sectors including transportation, energy, construction, and others has contributed to the rise in demand. Furthermore, In order to provide their services, its service providers enter into agreements with the building management. Management of contracts includes securing resources, including labour, tools, and services.

However, the market growth is hampered by the need for more technology expertise at the executive and managerial levels of facility management and skill sets necessary for managing large-scale facility operations. Several large facilities management service providers with a heavy initial investment in facility services hardly face challenges regarding limited utilization of technology due to the long contracts.

The facility management market is segmented based on offering and vertical. As per the offering, the market is segmented into solutions and services. The solutions segment comprises Integrated Workplace Management System (IWMS), Building Information Modeling (BIM), Facility Environment Management (Sustainability Management and Waste Management), Facility Property Management (Lease Accounting & Real Estate Management, Asset Maintenance Management, Workspace & relocation Management, Reservation Management), Facility Operations & Security Management (Lighting Control, HVAC Control, Video Surveillance & Access Control, Emergency & Incident Management. Also, Services include Professional Services (Deployment and integration, Consulting and training, Auditing and quality Assessment, Support and maintenance, and Service-Level Agreement Management) and Managed Services. The vertical segment consists of BFSI (Banking, Financial Services, And Insurance), IT & IETS, Government and Public Sector, Healthcare and Life Sciences, Education, Retail, Manufacturing, Telecom, Construction & Real Estate, Travel & Hospitality, and Other Verticals.

The services facility management market is expected to hold a significant global market share in 2024. The fastest growth is expected to occur in the services sector as a result of the trend toward treating IT as a service within businesses. Due to its ability to meet the strategic and operational requirements of businesses, this model of IT service delivery is likely to grow at significantly higher rates than the industry average over the coming years.

The prominent segment, healthcare and life sciences, is projected to grow rapidly in the global facility management market because of the rising demand for preventative facility management services in many countries. The healthcare and life sciences industry is expected to expand rapidly throughout the projection period, especially in countries like the US, Germany, the UK, China, and India.

The North American facility management market is expected to record the maximum market share in revenue in the near future. It can be attributed to because of the widespread adoption of cutting-edge technology like the Internet of Things, AI, robotics, and others. Throughout the projection period, the market is projected to expand significantly due to the popularity of government-backed initiatives. That's because people are starting to realize how crucial it is to prevent the spread of coronavirus by maintaining a clean environment. In addition, Asia Pacific is estimated to grow rapidly in the global facility management market because formal and informal businesses are operating in the market. Facility management solutions are in high demand, and cloud computing is becoming increasingly popular to deliver these services.

|

Report Attribute |

Specifications |

|

Market Size Value In 2024 |

USD 52.96 Bn |

|

Revenue Forecast In 2034 |

USD 170.04 Bn |

|

Growth Rate CAGR |

CAGR of 12.5% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

By Offering, and Vertical |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; Japan; Brazil; Mexico; The UK; France; Italy; Spain; China; Japan; India; South Korea; Southeast Asia |

|

Competitive Landscape |

IBM Corporation (US), Oracle Corporation (US), SAP SE (Germany), CBRE Group, Inc. (US), Jones Lang LaSalle Inc (US), Trimble Inc. (US), Nemetschek SE (Germany), Fortive (US), Infor Inc. (US), MRI Software LLC (US), Eptura (US), Planon (Netherlands), Johnson Controls International (Ireland), Apleona GmbH (Germany), Cushman & Wakefield plc (US), Causeway Technologies Limited (UK), Service Works Global Limited (UK), Facilities Management eXpress LLC. (US), Archidata International Inc (Canada), UpKeep Technologies, Inc. (US), FacilityOne Technologies (US), OfficeSpace Software, Inc. (US), Facilio.Inc (US), efacility (Switzerland), InnoMaint (India), Nuvolo (US), QuickFMS (India), and zLink (US). |

|

Customization Scope |

Free customization report with the procurement of the report and modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Facility Management Market Snapshot

Chapter 4. Global Facility Management Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Industry Analysis – Porter’s Five Forces Analysis

4.7. Competitive Landscape & Market Share Analysis

4.8. Impact of Covid-19 Analysis

Chapter 5. Market Segmentation 1: By Offering Estimates & Trend Analysis

5.1. By Offering, & Market Share, 2024 & 2034

5.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following By Offering:

5.2.1. Solutions

5.2.1.1. Integrated Workplace Management System

5.2.1.2. Building Information Modeling

5.2.1.3. Facility Operations & Security Management

5.2.1.3.1. Lighting Control

5.2.1.3.2. HVAC Control

5.2.1.3.3. Video Surveillance and Access Control

5.2.1.3.4. Emergency And Incident Management

5.2.1.4. Facility Environment Management

5.2.1.4.1. Sustainability Management

5.2.1.4.2. Waste Management

5.2.1.5. Facility Property Management

5.2.1.5.1. Lease Accounting and Real Estate Management

5.2.1.5.2. Asset Management

5.2.1.5.3. Workplace and Relocation Management

5.2.1.5.4. Reservation Management

5.2.2. Services

5.2.2.1. Professional Services

5.2.2.1.1. Deployment And Integration

5.2.2.1.2. Consulting

5.2.2.1.3. Auditing And Quality Assessment

5.2.2.1.4. Support And Maintenance

5.2.2.1.5. Service Level Agreement Management

5.2.2.2. Managed Services

Chapter 6. Market Segmentation 2: By Vertical Estimates & Trend Analysis

6.1. By Vertical & Market Share, 2024 & 2034

6.2. Market Size (Value US$ Mn) & Forecasts and Trend Analyses, 2021 to 2034 for the following By Vertical:

6.2.1. IT & ITeS

6.2.2. Telecom

6.2.3. Banking, Financial Services, & Insurance (BFSI)

6.2.4. Healthcare & Life Sciences

6.2.5. Education

6.2.6. Retail

6.2.7. Travel & Hospitality

6.2.8. Manufacturing

6.2.9. Construction & Real Estate

6.2.10. Government & Public Sector

6.2.11. Other Verticals

Chapter 7. Facility Management Market Segmentation 3: Regional Estimates & Trend Analysis

7.1. North America

7.1.1. North America Facility Management Market revenue (US$ Million) estimates and forecasts By Offering, 2021-2034

7.1.2. North America Facility Management Market revenue (US$ Million) estimates and forecasts By Vertical, 2021-2034

7.1.3. North America Facility Management Market revenue (US$ Million) estimates and forecasts by country, 2021-2034

7.2. Europe

7.2.1. Europe Facility Management Market revenue (US$ Million) By Offering, 2021-2034

7.2.2. Europe Facility Management Market revenue (US$ Million) By Vertical, 2021-2034

7.2.3. Europe Facility Management Market revenue (US$ Million) by country, 2021-2034

7.3. Asia Pacific

7.3.1. Asia Pacific Facility Management Market revenue (US$ Million) By Offering, 2021-2034

7.3.2. Asia Pacific Facility Management Market revenue (US$ Million) By Vertical, 2021-2034

7.3.3. Asia Pacific Facility Management Market revenue (US$ Million) by country, 2021-2034

7.4. Latin America

7.4.1. Latin America Facility Management Market revenue (US$ Million) By Offering, (US$ Million) 2021-2034

7.4.2. Latin America Facility Management Market revenue (US$ Million) By Vertical, (US$ Million) 2021-2034

7.4.3. Latin America Facility Management Market revenue (US$ Million) by country, 2021-2034

7.5. Middle East & Africa

7.5.1. Middle East & Africa Facility Management Market revenue (US$ Million) By Offering, (US$ Million) 2021-2034

7.5.2. Middle East & Africa Facility Management Market revenue (US$ Million) By Vertical, (US$ Million) 2021-2034

7.5.3. Middle East & Africa Facility Management Market revenue (US$ Million) by country, 2021-2034

Chapter 8. Competitive Landscape

8.1. Major Mergers and Acquisitions/Strategic Alliances

8.2. Company Profiles

8.2.1. IBM Corporation (US)

8.2.2. Oracle Corporation (US)

8.2.3. SAP SE (Germany)

8.2.4. CBRE Group, Inc. (US)

8.2.5. Jones Lang LaSalle Inc (US)

8.2.6. Trimble Inc. (US)

8.2.7. Nemetschek SE (Germany)

8.2.8. Fortive (US)

8.2.9. Infor Inc. (US)

8.2.10. MRI Software LLC (US)

8.2.11. Eptura (US)

8.2.12. Planon (Netherlands)

8.2.13. Johnson Controls International (Ireland)

8.2.14. Apleona GmbH (Germany)

8.2.15. Cushman & Wakefield plc (US)

8.2.16. Causeway Technologies Limited (UK)

8.2.17. Service Works Global Limited (UK)

8.2.18. Facilities Management eXpress LLC. (US)

8.2.19. Archidata International Inc (Canada)

8.2.20. UpKeep Technologies, Inc. (US)

8.2.21. FacilityOne Technologies (US)

8.2.22. OfficeSpace Software, Inc. (US)

8.2.23. Facilio.Inc (US)

8.2.24. efacility (Switzerland)

8.2.25. InnoMaint (India)

8.2.26. Nuvolo (US)

8.2.27. QuickFMS (India)

8.2.28. zLink (US)

Facility Management Market By Offering-

Facility Management Market By Vertical-

Facility Management Market By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

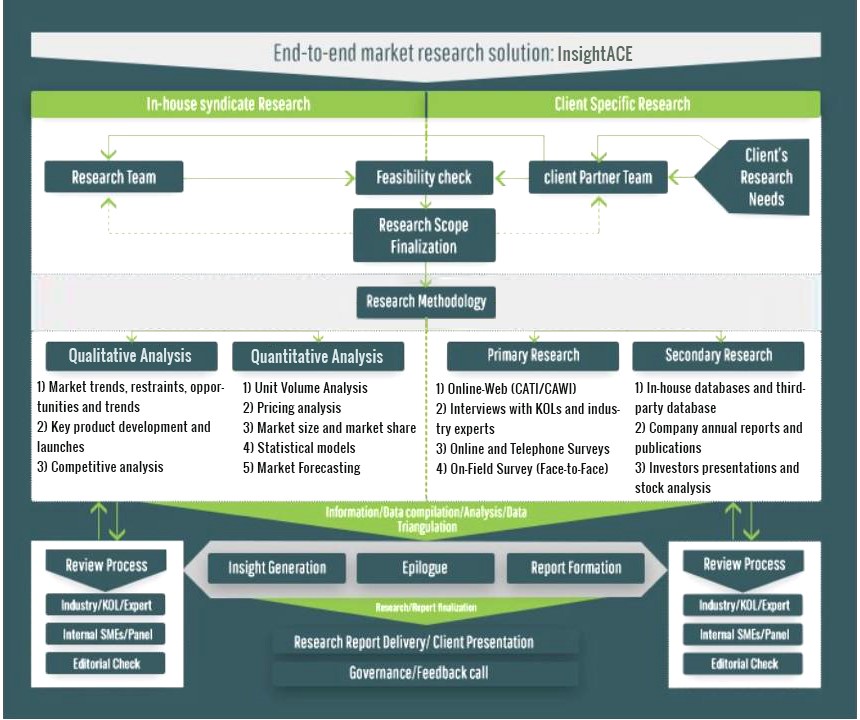

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.