Global Direct-to-Consumer Genetic Testing Market Size is valued at USD 2.4 Billion in 2024 and is predicted to reach USD 16.2 Billion by the year 2034 at a 21.2% CAGR during the forecast period for 2025-2034.

Direct access testing, also known as direct-to-consumer (DTC) testing, enables clients to order laboratory tests directly from a laboratory without necessarily involving their healthcare provider. Direct-to-consumer genetic testing provides a person's genetic information without needing a doctor or health insurance company. Customers can send the business a DNA sample and get immediate results. Direct-to-consumer genetic testing, among other things, raises awareness of numerous genetic illnesses that aid in predicting one's health and offer information on standard features and ancestry. DTC genetic testing is quick to deliver findings confidently, inexpensively, and easy to use. Such scenarios will help the market expand beneficially.

One of the main factors projected to fuel the growth of the direct-to-consumer (DTC) genetic testing market over the anticipated period is the rise in public awareness. The direct-to-consumer (DTC) genetic testing industry is also expected to grow due to the increase in income levels in developing nations. Additionally, the growing need for service personalization will likely create additional chances for the direct-to-consumer (DTC) genetic testing industry to expand over the next few years.

However, direct-to-consumer (DTC) genetic testing market expansion may be hindered in the near future by flaws in the DTC testing kits. Direct-to-consumer (DTC) genetic testing market expansion is anticipated to be hampered over the timeframe due to the rising cost of DTC genetic testing. Furthermore, insufficient data links a particular genetic mutation to a given illness or functionality. Genetic privacy may also be jeopardized if testing businesses utilize their clients' genetic data improperly or if the information is stolen.

The Direct-to-Consumer Genetic Testing Market is segmented based on type, type of technology, and distribution channel. Based on type, the market is segmented into nutrigenomics testing, predictive testing, carrier testing, and others. Based on the type of technology, the market is divided into whole genome sequencing, single-nucleotide polymorphism chips, targeted analysis, and others. Based on the distribution channel, the market is divided into online platforms, OTC.

Based on type, the market is segmented into nutrigenomics testing, predictive testing, carrier testing, and others Among these, the predictive testing segment is expected to have the highest growth rate during the forecast period. his segment is also expected to experience the fastest growth over the forecast period. The popularity of predictive testing is driven by consumers' increasing interest in understanding their genetic predispositions to various health conditions, enabling proactive health management. Predictive genetic tests offer valuable information on potential health risks, giving consumers a sense of control over their health and the ability to make informed decisions. Tests that assess genetic risks for common diseases like breast cancer (or cardiovascular disease are particularly popular.

Based on the type of technology, the market is divided into whole genome sequencing, single-nucleotide polymorphism chips, targeted analysis, and others. The whole genome sequencing (WGS) segment dominates the market. Advancements in sequencing technologies and a reduction in the cost of genome sequencing have made WGS more affordable and accessible to consumers. The initial high cost of whole genome sequencing has decreased significantly, making it a viable option for direct-to-consumer testing. WGS offers high accuracy and reliability in identifying genetic variations across the entire genome. This comprehensive data allows for a more precise understanding of an individual's genetic predispositions and potential health risks.

In the forecast period, North America to hold a major global market share. The high prevalence of rare illnesses, the presence of numerous disease registries, a sizable number of R&D centres for ultra-rare diseases, and significant investments in disease detection are all factors that contribute to the region's considerable market share. Customers with a lot of disposable money can spend more on direct-to-consumer genetic testing, like genetic and nutrigenomics testing, which encourages regional growth. In addition, the arrival of significant industry players in the area and accelerated technology advancements will foster market expansion locally.

During the forecasted years, Asia Pacific is anticipated to experience significant growth. This is primarily due to improvements in awareness and diagnostic skills. Furthermore, this region will benefit financially from implementing frameworks and policies that support illness management. In China, only a relatively smaller percentage of the population uses genetic screening services, although demand is augmenting. With this, many foreign businesses are anticipated to enter the China direct-to-consumer genetic testing industry to offer affordable services.

|

Report Attribute |

Specifications |

|

Market Size Value In 2024 |

USD 2.4 Billion |

|

Revenue Forecast In 2034 |

USD 16.2 Billion |

|

Growth Rate CAGR |

CAGR of 21.2% from 2025 to 2034 |

|

Quantitative Units |

Representation of revenue in US$ Bn,and CAGR from 2025 to 2034 |

|

Historic Year |

2021 to 2024 |

|

Forecast Year |

2025-2034 |

|

Report Coverage |

The forecast of revenue, the position of the company, the competitive market structure, growth prospects, and trends |

|

Segments Covered |

Type, Type of Technology, Distribution Channel |

|

Regional Scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; China; India; Japan; Brazil; Mexico ; France; Italy; Spain; South Korea; South East Asia; |

|

Competitive Landscape |

23andme Inc., 24Genetics, Ancestry.com LLC, Atlas Biomed, Color Genomics, DNAfit, Gene by Gene, Chengdu Twenty-Three Rubik’s Cube Biotechnology Co., Ltd., EasyDNA, Mapmygenome, MyHeritage Ltd., Laboratory Corporation of America Holdings, Myriad Genetics, Inc., Konica Minolta, Inc., XCODE Life. |

|

Customization Scope |

Free customization report with the procurement of the report, Modifications to the regional and segment scope. Particular Geographic competitive landscape. |

|

Pricing And Available Payment Methods |

Explore pricing alternatives that are customized to your particular study requirements. |

Chapter 1. Methodology and Scope

1.1. Research Methodology

1.2. Research Scope & Assumptions

Chapter 2. Executive Summary

Chapter 3. Global Direct-to-Consumer Genetic Testing Market Snapshot

Chapter 4. Global Direct-to-Consumer Genetic Testing Market Variables, Trends & Scope

4.1. Market Segmentation & Scope

4.2. Drivers

4.3. Challenges

4.4. Trends

4.5. Investment and Funding Analysis

4.6. Porter's Five Forces Analysis

4.7. Incremental Opportunity Analysis (US$ MN), 2024-2034

4.8. Competitive Landscape & Market Share Analysis, By Key Player (2023)

4.9. Use/impact of AI on Direct-to-Consumer Genetic Testing Market Industry Trends

4.10. Global Direct-to-Consumer Genetic Testing Market Penetration & Growth Prospect Mapping (US$ Mn), 2021-2034

Chapter 5. Direct-to-Consumer Genetic Testing Market Segmentation 1: By Type, Estimates & Trend Analysis

5.1. Market Share by Type, 2024 & 2034

5.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following Type:

5.2.1. Nutrigenomics Testing

5.2.2. Predictive testing

5.2.3. Carrier Testing

5.2.4. Others

Chapter 6. Direct-to-Consumer Genetic Testing Market Segmentation 2: By Type of Technology, Estimates & Trend Analysis

6.1. Market Share by Type of Technology, 2024 & 2034

6.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following Type of Technology:

6.2.1. Whole Genome Sequencing

6.2.2. Single Nucleotide Polymorphism Chips

6.2.3. Targeted Analysis

6.2.4. Others

Chapter 7. Direct-to-Consumer Genetic Testing Market Segmentation 3: By Distribution Channel, Estimates & Trend Analysis

7.1. Market Share by Distribution Channel, 2024 & 2034

7.2. Market Size Revenue (US$ Million) & Forecasts and Trend Analyses, 2021 to 2034 for the following Distribution Channel:

7.2.1. Online Platform

7.2.2. OTC

Chapter 8. Direct-to-Consumer Genetic Testing Market Segmentation 5: Regional Estimates & Trend Analysis

8.1. Global Direct-to-Consumer Genetic Testing Market, Regional Snapshot 2024 & 2034

8.2. North America

8.2.1. North America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.2.1.1. US

8.2.1.2. Canada

8.2.2. North America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.2.3. North America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type of Technology, 2021-2034

8.2.4. North America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Distribution Channel, 2021-2034

8.3. Europe

8.3.1. Europe Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.3.1.1. Germany

8.3.1.2. U.K.

8.3.1.3. France

8.3.1.4. Italy

8.3.1.5. Spain

8.3.1.6. Rest of Europe

8.3.2. Europe Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.3.3. Europe Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type of Technology, 2021-2034

8.3.4. Europe Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Distribution Channel, 2021-2034

8.4. Asia Pacific

8.4.1. Asia Pacific Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.4.1.1. India

8.4.1.2. China

8.4.1.3. Japan

8.4.1.4. Australia

8.4.1.5. South Korea

8.4.1.6. Hong Kong

8.4.1.7. Southeast Asia

8.4.1.8. Rest of Asia Pacific

8.4.2. Asia Pacific Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.4.3. Asia Pacific Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type of Technology, 2021-2034

8.4.4. Asia Pacific Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Distribution Channel, 2021-2034

8.5. Latin America

8.5.1. Latin America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Country, 2021-2034

8.5.1.1. Brazil

8.5.1.2. Mexico

8.5.1.3. Rest of Latin America

8.5.2. Latin America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.5.3. Latin America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type of Technology, 2021-2034

8.5.4. Latin America Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Distribution Channel, 2021-2034

8.6. Middle East & Africa

8.6.1. Middle East & Africa Wind Turbine Rotor Blade Market Revenue (US$ Million) Estimates and Forecasts by country, 2021-2034

8.6.1.1. GCC Countries

8.6.1.2. Israel

8.6.1.3. South Africa

8.6.1.4. Rest of Middle East and Africa

8.6.2. Middle East & Africa Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type, 2021-2034

8.6.3. Middle East & Africa Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Type of Technology, 2021-2034

8.6.4. Middle East & Africa Direct-to-Consumer Genetic Testing Market Revenue (US$ Million) Estimates and Forecasts by Distribution Channel, 2021-2034

Chapter 9. Competitive Landscape

9.1. Major Mergers and Acquisitions/Strategic Alliances

9.2. Company Profiles

9.2.1. 23andMe

9.2.1.1. Business Overview

9.2.1.2. Key Type/Service Overview

9.2.1.3. Financial Performance

9.2.1.4. Geographical Presence

9.2.1.5. Recent Developments with Business Strategy

9.2.2. Illumina, Inc.

9.2.3. Family Tree DNA

9.2.4. Ancestry

9.2.5. Myriad Genetics, Inc.

9.2.6. Genesis HealthCare

9.2.7. EasyDNA

9.2.8. Veritas

9.2.9. Full Genomes Corporation, Inc

9.2.10. Living DNA Ltd.

9.2.11. Color Health, Inc.

Direct-to-Consumer Genetic Testing Market - By Type

Direct-to-Consumer Genetic Testing Market By Technology

Direct-to-Consumer Genetic Testing Market By Distribution Channel-

By Region-

North America-

Europe-

Asia-Pacific-

Latin America-

Middle East & Africa-

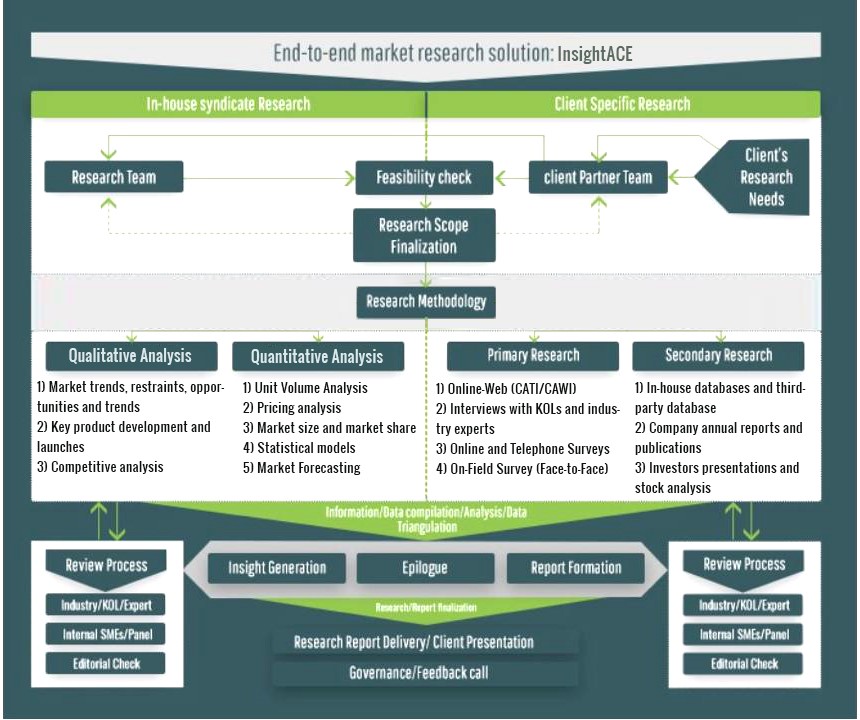

InsightAce Analytic follows a standard and comprehensive market research methodology focused on offering the most accurate and precise market insights. The methods followed for all our market research studies include three significant steps – primary research, secondary research, and data modeling and analysis - to derive the current market size and forecast it over the forecast period. In this study, these three steps were used iteratively to generate valid data points (minimum deviation), which were cross-validated through multiple approaches mentioned below in the data modeling section.

Through secondary research methods, information on the market under study, its peer, and the parent market was collected. This information was then entered into data models. The resulted data points and insights were then validated by primary participants.

Based on additional insights from these primary participants, more directional efforts were put into doing secondary research and optimize data models. This process was repeated till all data models used in the study produced similar results (with minimum deviation). This way, this iterative process was able to generate the most accurate market numbers and qualitative insights.

Secondary research

The secondary research sources that are typically mentioned to include, but are not limited to:

The paid sources for secondary research like Factiva, OneSource, Hoovers, and Statista

Primary Research:

Primary research involves telephonic interviews, e-mail interactions, as well as face-to-face interviews for each market, category, segment, and subsegment across geographies

The contributors who typically take part in such a course include, but are not limited to:

Data Modeling and Analysis:

In the iterative process (mentioned above), data models received inputs from primary as well as secondary sources. But analysts working on these models were the key. They used their extensive knowledge and experience about industry and topic to make changes and fine-tuning these models as per the product/service under study.

The standard data models used while studying this market were the top-down and bottom-up approaches and the company shares analysis model. However, other methods were also used along with these – which were specific to the industry and product/service under study.

To know more about the research methodology used for this study, kindly contact us/click here.